Key Takeaways

- Sole proprietors must prepare a Profit & Loss Account and Balance Sheet annually, even if revenue is below S$500,000

- Business income is taxed at personal income tax rates (0%–24%), not corporate rates, so accurate profit tracking directly affects your tax bill

- Revenue of S$500,000+ requires certified accounts submitted to IRAS; below that threshold, a simplified 4-Line Statement suffices — but full records must still be kept

- GST registration is mandatory once taxable turnover exceeds S$1 million, requiring quarterly filing and GST-compliant invoices

- All financial records must be retained for at least 5 years and can be requested by IRAS at any time

What Is Accounting for a Sole Proprietorship in Singapore?

Sole proprietorship accounting covers four core responsibilities: recording business revenues and expenses, maintaining organized financial records, preparing required financial statements, and fulfilling tax obligations with IRAS.

Unlike a company, a sole proprietorship is not a separate legal entity from the owner. Personal and business finances are legally intertwined, and the owner bears full liability for all business debts.

Purpose of the accounting process:

- Provide an accurate picture of business profitability

- Calculate your tax liability precisely

- Demonstrate compliance with IRAS requirements

- Support decision-making and financial planning

Understanding these fundamentals helps clarify where sole proprietorship accounting diverges from company accounting.

How It Differs from Company Accounting

Key distinctions:

- Business income is reported on Form B or Form B1 through your personal income tax filing — no separate corporate return is required

- No external audit is required unless specific conditions or revenue thresholds apply

- Business profit is taxed at Singapore's progressive personal income tax rates (0%–24%), not the flat 17% corporate tax rate

- Depending on your revenue level, you may qualify for a simplified 2-Line or 4-Line Statement instead of full certified accounts

Key Accounting and Compliance Obligations for Sole Proprietors in Singapore

Legal Requirement to Prepare Statement of Accounts

Every sole proprietor must prepare a statement of accounts comprising two documents:

- Profit & Loss Account: Records all income earned and expenses incurred during the financial year

- Balance Sheet: Shows business assets, liabilities, and owner's equity at year-end

These documents must be prepared annually, regardless of revenue level. IRAS provides a downloadable template to help structure these statements correctly.

IRAS Revenue Threshold Rules

Your submission requirements depend on annual revenue:

| Revenue Level | Filing Requirement |

|---|---|

| S$200,000 or less | 2-Line Statement (Revenue + Adjusted Profit/Loss) |

| More than S$200,000 | 4-Line Statement (Revenue, Gross Profit, Allowable Expenses, Adjusted Profit/Loss) |

| S$500,000 or more | 4-Line Statement + Certified Statement of Accounts |

Critical point: Even if you qualify for a simplified statement, you must still prepare and retain full accounts that can be produced if IRAS requests them.

Record-Keeping Requirements

Sole proprietors must retain source documents for a minimum of 5 years, including:

- Sales invoices and receipts

- Purchase orders and supplier invoices

- Bank statements

- Contracts and agreements

- Vouchers and supporting documents

- General ledgers

- Tax computations

These records must be organized and accessible for potential IRAS review or audit. Failure to maintain proper records can result in disallowed expenses, estimated income assessments, and financial penalties.

CPF Medisave Obligations

Self-employed persons earning more than S$6,000 in net trade income (NTI) annually must contribute to their Medisave account. Factor these contributions into your cash-flow planning when calculating take-home profit.

Consequences of non-compliance:

- ACRA will not process business registration renewals

- Licensing authorities will refuse new licence applications

- CPF Board may enforce collection through legal channels

Allowable vs. Non-Allowable Business Expenses

Understanding which expenses can be deducted is critical for accurate tax computation. IRAS provides detailed guidance on allowable deductions. To qualify, an expense must be incurred wholly and exclusively to earn business income and supported by documentation such as receipts, invoices, or contracts.

Non-allowable expenses include:

- Owner's salary, bonus, or drawings

- Personal or domestic expenses

- Capital expenditure (computers, furniture, equipment qualify for capital allowances instead)

- Income tax payments

- Amounts exceeding statutory rates, such as excess CPF contributions or Foreign Worker Levy

- Club subscriptions, personal entertainment, and travel between home and workplace

How Sole Proprietorship Accounting Works: Step-by-Step

Sole proprietorship accounting runs year-round — every transaction recorded now saves hours of scrambling at tax time. Here's how the process breaks down:

Step 1: Set Up a Separate Business Account and Chart of Accounts

Separating personal and business finances isn't legally required, but it's essential for accurate accounting. It simplifies transaction tracking, reduces errors, and makes reconciliation straightforward.

Basic chart of accounts for sole proprietors:

- Income: Sales revenue, service fees, other business income

- Cost of Goods Sold: Direct costs of producing goods or services

- Operating Expenses: Rent, utilities, marketing, professional fees, office supplies

- Assets: Cash, accounts receivable, equipment, inventory

- Liabilities: Accounts payable, loans, accrued expenses

Step 2: Record Transactions Consistently

Choose a recording method that fits your volume:

- Manual ledgers

- Spreadsheet-based bookkeeping

- Accounting software (Xero, QuickBooks, cloud-based solutions)

Most sole proprietors in Singapore use cash-basis accounting — recording income when received and expenses when paid. As your business grows, switching to accrual-basis accounting gives you a clearer view of outstanding income and unpaid expenses.

Record every financial event, including:

- Every sale and invoice issued

- All purchases and payments made

- Bank deposits and withdrawals

- Petty cash transactions

- Loan repayments and interest

Step 3: Reconcile Accounts and Prepare Financial Statements

Monthly/quarterly reconciliation:

- Match bank statements to recorded transactions

- Identify discrepancies and resolve errors

- Update accounts receivable and payable balances

Annual preparation:

- Prepare the Profit & Loss Account and Balance Sheet

- Use IRAS's sample statement of accounts template to ensure compliance

- Review for accuracy before filing

Step 4: Calculate Taxable Income and File with IRAS

Follow these four steps to calculate your taxable income:

- Start with net profit from the P&L Account

- Add back disallowable expenses (personal costs, capital expenditure)

- Deduct capital allowances (depreciation on business assets)

- Result = Adjusted Profit (your taxable business income)

Report the adjusted profit through Form B or B1 on the myTax Portal. The filing deadline is 18 April (e-Filing) or 1 March (paper filing).

Income Tax and GST Obligations for Sole Proprietors in Singapore

Personal Income Tax Rates

Sole proprietors are taxed on business profits at Singapore's progressive personal income tax rates:

| Chargeable Income (Marginal Band) | Tax Rate | Tax Payable on Band |

|---|---|---|

| First S$20,000 | 0% | S$0 |

| Next S$10,000 (S$20,001–S$30,000) | 2% | S$200 |

| Next S$10,000 (S$30,001–S$40,000) | 3.5% | S$350 |

| Next S$40,000 (S$40,001–S$80,000) | 7% | S$2,800 |

| Next S$40,000 (S$80,001–S$120,000) | 11.5% | S$4,600 |

| Next S$40,000 (S$120,001–S$160,000) | 15% | S$6,000 |

| Next S$40,000 (S$160,001–S$200,000) | 18% | S$7,200 |

| Next S$40,000 (S$200,001–S$240,000) | 19% | S$7,600 |

| Next S$40,000 (S$240,001–S$280,000) | 19.5% | S$7,800 |

| Next S$40,000 (S$280,001–S$320,000) | 20% | S$8,000 |

| Next S$180,000 (S$320,001–S$500,000) | 22% | S$39,600 |

| Next S$500,000 (S$500,001–S$1,000,000) | 23% | S$115,000 |

| Above S$1,000,000 | 24% | 24% on amount above S$1,000,000 |

Corporate tax comparison:

Companies in Singapore are taxed at a flat 17% rate and benefit from Start-Up Tax Exemption (SUTE) schemes that can exempt up to S$125,000 of chargeable income. Sole proprietorships do not qualify for SUTE — only incorporated companies are eligible.

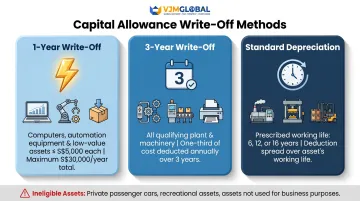

Capital Allowances

Sole proprietors can claim capital allowances on fixed assets used in the business:

Three write-off methods apply:

- 1-year write-off: Computers, automation equipment, low-value assets (≤S$5,000 each, max S$30,000 total per year)

- 3-year write-off: All qualifying plant and machinery (one-third deducted annually)

- Standard depreciation: Over prescribed working life of 6, 12, or 16 years

Eligible assets include computers, laptops, printers, software, office furniture, machinery, and commercial vehicles. Private passenger cars (S-plated vehicles) do not qualify.

Keep a fixed asset schedule recording cost, purchase date, and depreciation method for each asset — IRAS may request this during audits.

GST Registration Obligations

GST registration becomes mandatory when taxable turnover exceeds S$1 million under either:

- Retrospective view: Taxable turnover exceeded S$1 million at the end of the calendar year

- Prospective view: Reasonably expected to exceed S$1 million in the next 12 months

Current GST rate: 9% (effective 1 January 2024)

Once registered, you must:

- Charge 9% GST on all standard-rated supplies

- Issue GST-compliant tax invoices (simplified invoices permitted for amounts under S$1,000)

- File quarterly GST returns (Form GST F5) within one month of each accounting period

- Retain GST-specific records for at least 5 years

- Display all prices inclusive of GST

Quarterly filing deadlines: Jan–Mar by 30 Apr, Apr–Jun by 31 Jul, Jul–Sep by 31 Oct, Oct–Dec by 31 Jan.

GST compliance sits alongside your personal income tax obligations — both draw from the same business income records, so accurate bookkeeping serves double duty.

Personal Tax Reliefs

As a self-employed person filing personal income tax, you can claim reliefs that reduce overall tax payable:

- Earned Income Relief: S$1,000 (below age 55), S$6,000 (age 55–59), S$8,000 (age 60+)

- CPF Relief for Self-Employed: Full relief on mandatory Medisave contributions; from YA 2026, relief extends to full CPF contributions

- CPF Cash Top-Up Relief: Up to S$16,000 per year (max S$8,000 for yourself, max S$8,000 for eligible family members)

These reliefs apply directly against your chargeable income, so the lower your net business income (after legitimate deductions), the more effectively each relief reduces your final tax bill.

Common Accounting Mistakes Sole Proprietors Make — and When to Seek Help

Frequent Accounting Errors

1. Mixing personal and business expenses:

Recording personal costs as business expenses inflates deductions and triggers IRAS scrutiny. Keep finances separate, even if you use the same bank account.

2. Failing to retain source documents:

Missing receipts, invoices, or bank statements mean you can't prove expenses if IRAS requests documentation. Result: disallowed deductions and penalties.

3. Using vague expense categories:

Grouping multiple expenses under "General" or "Miscellaneous" violates IRAS requirements. Expenses must be itemized with clear descriptions.

4. Incorrectly claiming private or capital expenditure:

Personal meals, home-to-office travel, and equipment purchases cannot be deducted as operating expenses. Capital assets qualify for capital allowances instead.

5. Missing GST registration deadlines:

If turnover exceeds S$1 million, you must register within 30 days. Late registration results in penalties and backdated GST liabilities.

The Low-Revenue Misconception

Many sole proprietors believe that earning below S$500,000 exempts them from serious accounting obligations. This is false. IRAS can request full records at any time, regardless of revenue. Missing or inaccurate records lead to:

- Disallowed expense claims

- Estimated income assessments (IRAS guesses your income)

- Financial penalties

- Interest charges on unpaid taxes

When to Engage a Professional Accounting Firm

Consider professional support when you encounter:

- Revenue approaching or exceeding S$500,000 — certified accounts become mandatory

- Multiple income streams — each revenue type carries distinct tax treatment and reporting obligations

- GST registration — quarterly filings and compliance require specialized knowledge

- Employees on payroll — payroll processing, CPF contributions, and tax withholding add layers

- International clients or transactions — cross-border tax issues require expertise

If any of these apply, professional support is worth the investment. Firms like VJM Global provide outsourced accounting, bookkeeping, and tax compliance services — including cross-border and international transaction support — so filings stay accurate and deadlines don't get missed.

Frequently Asked Questions

What is the liability of a sole proprietorship in Singapore?

A sole proprietor bears unlimited personal liability, meaning the owner's personal assets (savings, property) can be used to settle business debts or legal claims. Unlike a company, there is no corporate shield separating personal and business obligations.

Do sole proprietors in Singapore need to file audited financial statements?

No. Sole proprietors are not required to have their accounts audited. They must prepare a statement of accounts (P&L and Balance Sheet), and only those with revenue of S$500,000 or more need to submit certified accounts signed by the owner to IRAS.

What is the income tax rate for a sole proprietor in Singapore?

Sole proprietors are taxed at Singapore's personal income tax rates on their business profits, ranging from 0% to 24% on a progressive scale. This contrasts with the flat 17% corporate tax rate available to Pte Ltd companies.

When must a sole proprietor register for GST in Singapore?

GST registration becomes mandatory when taxable turnover exceeds S$1 million annually. Once registered, the sole proprietor must charge 9% GST on taxable supplies, file quarterly GST returns via myTax Portal, and maintain GST-compliant records.

What records does a sole proprietor need to keep in Singapore?

Sole proprietors must retain all source documents for 5 years, including invoices, receipts, bank statements, contracts, and tax computations. Records must be organized and available for IRAS inspection.

Can a sole proprietor deduct business expenses from taxable income in Singapore?

Yes. Allowable business expenses incurred wholly and exclusively to produce business income can be deducted, provided they are supported by proper documentation. Private or domestic expenses and capital expenditure are not deductible; capital assets qualify for capital allowances instead.