Introduction

For Singapore-based NRIs and OCI (Overseas Citizen of India) cardholders looking to enter the Indian market without the overhead of a full company setup, the sole proprietorship is often the first structure they consider. It's India's simplest business form: a single-owner entity with no legal identity separate from the owner, and relatively low setup costs compared to a private limited company or LLP.

The process looks simple on paper, but Singapore-based applicants hit friction points that most generic guides skip entirely. Aadhaar biometric requirements, FEMA (Foreign Exchange Management Act) compliance, and document authentication protocols create real barriers for non-residents.

This guide covers what Singapore-based individuals actually need to know: eligibility rules, required documentation, the registration process step by step, and the compliance obligations that follow.

Key Takeaways

- No mandatory corporate registration required, but specific licences (Shop and Establishment, GST) and a business bank account are essential for legal operations

- Foreign nationals face strict restrictions; this structure is only viable for Singapore-based NRIs or OCIs who are physically present in India

- Registration typically completes in 10–15 days with low upfront costs compared to other India entry structures

- Ongoing compliance includes annual income tax filing, quarterly GST returns (if applicable), and licence renewals

- Singapore Pte. Ltd. companies cannot register a sole proprietorship; a Private Limited Company or LLP is required instead

What Is a Sole Proprietorship in India and Who Can Register One?

Defining the Structure

A sole proprietorship in India is a business owned and operated by a single individual where there is no legal distinction between the owner and the business. As confirmed by Supreme Court rulings, a proprietorship is not a separate legal entity. All profits, debts, and liabilities belong entirely to the owner.

Unlike a Private Limited Company or LLP, there is no mandatory incorporation, no shareholders, and no MCA (Ministry of Corporate Affairs) registration. India has no single statute governing sole proprietorship formation, though various registrations (GST, Shop and Establishment Act) formalize business operations.

Key Features Making It Popular

Why businesses choose this structure:

- No mandatory incorporation process

- Minimal compliance burden compared to corporate structures

- Fast setup timeline (10–15 days)

- Full decision-making authority retained by the owner

- No minimum capital requirement

- Business income taxed as personal income under applicable tax slabs

The Eligibility Question for Singapore-Based Individuals

These straightforward features make the structure appealing — but eligibility depends heavily on your specific situation as a Singapore-based individual.

India has no formal law explicitly barring foreign nationals from sole proprietorships. The practical barrier is documentation: the structure requires an Indian PAN card, Aadhaar card, and a registered Indian address. These are accessible to NRIs and OCIs, but largely unavailable to non-resident foreign nationals with no prior India ties.

Three categories of Singapore-based individuals considering this route:

- Indian-origin Singapore citizens/OCIs — Eligible, provided they hold a valid OCI card, Indian PAN, and can establish a registered Indian address

- NRIs temporarily relocating to India — Eligible once physically present and able to complete Aadhaar and PAN requirements in person

- Singapore-incorporated companies (Pte. Ltd.) — Cannot use a sole proprietorship; must consider Private Limited Company, Wholly Owned Subsidiary, or LLP

Under the FEMA Non-debt Instruments Rules 2019, NRIs and OCIs are explicitly permitted to invest in proprietary concerns on a non-repatriation basis (meaning profits cannot be repatriated to Singapore). The barrier to ownership is procedural, not statutory.

Critical Distinction from Other Structures

| Feature | Sole Proprietorship | Private Limited Company | LLP |

|---|---|---|---|

| Legal entity | Not separate from owner | Separate legal entity | Separate legal entity |

| Liability | Unlimited personal liability | Limited to shareholding | Limited to agreed contribution |

| Registration | Indirect (GST, licences) | Mandatory with MCA | Mandatory with MCA |

| Compliance burden | Minimal | High (annual filings, audits) | Moderate (annual filings) |

| Capital raising | Not possible | Can raise equity | Limited options |

Why Singapore Businesses Consider the Sole Proprietorship Route Into India

Practical Appeal for Eligible Individuals

For Singapore-based NRIs or OCIs, the sole proprietorship offers a practical entry point:

- Minimal capital investment — No mandatory minimum capital requirement

- No incorporation fees — Only licence fees apply; no company formation costs

- Near-zero ongoing regulatory overhead — No annual board meetings, audits, or MCA filings

- Ideal for market testing — Perfect for freelancers, consultants, or small traders exploring Indian market potential

Tax Simplicity

The low setup burden is only part of the appeal. On the tax side, business income is treated as the individual's personal income and taxed under the applicable Indian income tax slab, avoiding the complexity of corporate tax structures. The India-Singapore DTAA (Double Taxation Avoidance Agreement) — in force since May 27, 1994, with an amended protocol effective October 1, 2019 — can reduce double taxation exposure for eligible individuals.

Under the DTAA:

- Business profits are taxable only in Singapore unless a Permanent Establishment (PE) exists in India

- Independent personal services income is taxable in India only if a fixed base exists or the individual stays 183+ days in the fiscal year

- NRI sole proprietors can claim DTAA benefits by obtaining a Tax Residency Certificate from IRAS and filing Form 10F in India

Scale of Proprietorship in India

Over 7.30 crore enterprises (73 million) have registered on the Udyam portal as of December 2025, with the vast majority being micro or proprietary enterprises. This scale reflects the structure's accessibility and minimal compliance burden — it is widely familiar to Indian banks, vendors, and government agencies, which matters when opening accounts or applying for licences.

The Singapore-India investment corridor is robust: cumulative FDI equity inflow from Singapore to India stands at USD 171.92 billion (23.87% of India's total cumulative FDI) as of December 2024, ranking Singapore 2nd among all FDI source countries.

How to Register a Sole Proprietorship in India: Step-by-Step

The registration process does not follow a single government portal but instead involves obtaining a series of documents and licences that collectively establish the business. Total timeline: approximately 10–15 days assuming all documentation is in order.

Step 1: Obtain a PAN Card

The PAN card is the most critical prerequisite for any Indian business activity.

Which form applies:

- Form 49A — For Indian citizens, including NRIs holding Indian passports

- Form 49AA — For foreign nationals and OCI cardholders

Fee structure:

- Indian address dispatch: ₹91 excluding GST (approximately ₹107 including GST)

- Foreign address dispatch: ₹862 excluding GST (approximately ₹1,017 including GST)

Documents required:

- Passport (mandatory for foreign nationals)

- Overseas address proof

- Photographs

- OCI card (for OCI applicants)

Processing timeline:

- e-PAN: 2–3 working days

- Physical PAN card: 15–20 working days

Under Section 139AA of the Income Tax Act, PAN-Aadhaar linking is mandatory for resident taxpayers — PANs not linked by June 30, 2023 became inoperative. NRIs and non-citizens are exempt from this requirement. If re-activation is needed, a late linking fee of ₹1,000 applies.

Step 2: Secure a Registered Office Address in India

The sole proprietorship must have a registered Indian address.

Document requirements:

| Property Type | Documents Required |

|---|---|

| Owned property | Electricity bill, property tax receipt, sale deed, or municipal khata |

| Rented property | Rent/lease agreement + NOC from landlord + landlord's ownership proof |

| Virtual office | Service agreement + NOC from provider + ownership proof of premises |

Virtual office addresses are legally accepted for GST registration. GST Circular 161/17/2021 and subsequent CBIC instructions confirm this, provided the rental agreement and NOC are submitted with the application.

Singapore-based registrants without physical presence in India may explore:

- Family member's address with proper consent

- Compliant virtual office address in key business centres

- Temporary residential address during an India visit

Step 3: Obtain a Shop and Establishment Act Licence

With an address in place, the next step is securing the foundational operating licence for that location. Also called a "gumasta" or trade licence, this is issued by the local municipal authority and must be obtained within 30 days of commencing business operations.

State-specific variations:

| State | Fee Range | Online Portal |

|---|---|---|

| Maharashtra (Mumbai) | ₹2,500 – ₹10,000 | portal.mcgm.gov.in |

| Delhi | Up to ₹5,000 | labourcis.nic.in |

| Karnataka | Varies by municipality | labouronline.kar.nic.in |

The form and requirements vary significantly by state. Each state has its own version of the Act, implemented by the respective Labour Department.

Step 4: Register for GST (If Applicable)

GST registration is mandatory when:

- Annual turnover exceeds ₹20 lakh for services (₹40 lakh for goods) in regular states

- Conducting inter-state trade (regardless of turnover)

- Selling through e-commerce platforms

Registration is free — no government fee on the official portal (gst.gov.in).

Documents needed:

- PAN card

- Aadhaar (for residents) or passport/OCI card (for non-residents)

- Registered address proof

- Bank account details

- Business details and photographs

OCI cardholders should verify current Aadhaar-equivalent requirements before applying — while the OCI card serves as identity proof in most scenarios, the GST portal's acceptance can vary. Non-resident taxable persons must submit a valid passport along with Form GST REG-09.

Once registered, your filing schedule depends on turnover:

- QRMP scheme (quarterly filing) available for turnover up to ₹5 crore

- GSTR-1 and GSTR-3B due: 22nd or 24th of the month following the quarter

- Turnover above ₹5 crore: monthly filing required

Step 5: Open a Business Bank Account

A current account in the business name is required under RBI KYC guidelines to maintain a clear separation between personal and business transactions.

Documents typically required:

- GST certificate

- Shop and Establishment licence

- PAN card

- Identity proof (Aadhaar, passport, or OCI card)

- Address proof

Under the RBI Master Direction on KYC, banks require two-fold verification: (1) KYC of the individual proprietor, and (2) proof of business existence. Banks require any two of the following business proof documents:

- GST Registration Certificate

- Shop and Establishment Act Licence

- Udyam (MSME) Registration Certificate

- Professional Tax Licence

- FSSAI Licence (food businesses)

If only one document is available, banks may accept it subject to physical verification (site visit) of business premises.

Key Documents and Practical Challenges for Singapore Registrants

Consolidated Document Checklist

For Singapore-based individuals registering a sole proprietorship:

- Indian PAN card (Form 49A or 49AA)

- Aadhaar card or OCI card as substitute where applicable

- Registered Indian office address proof (owned or rented)

- Passport-size photographs

- Business name and description

- Sector-specific licences (if applicable)

The Aadhaar Challenge

The primary obstacle for Singapore registrants:

Aadhaar enrolment requires physical biometric capture in India and cannot be completed remotely or at Indian consulates abroad. Key facts:

- 182-day residency requirement: OCI cardholders must have resided in India for at least 182 days in the 12 months preceding application

- In-person enrolment mandatory: You must have biometric data captured at an authorized enrolment centre in India

- Not mandatory for all processes: NRIs and non-citizens are exempt from PAN-Aadhaar linking, though some registrations assume Aadhaar availability

Singapore-based individuals planning to register should schedule an India visit specifically to complete Aadhaar enrolment before beginning other registration steps.

Beyond identity documentation, Singapore registrants also need to account for how funds move in and out of the Indian business — which is governed by FEMA.

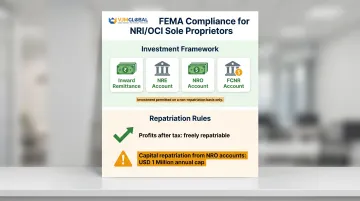

FEMA Compliance Considerations

While a sole proprietorship itself has no FEMA registration requirement, Singapore-based owners who remit funds into the Indian business account or repatriate profits must ensure compliance with RBI guidelines.

Investment framework under FEMA Non-debt Instruments Rules 2019:

- NRIs/OCIs can invest in proprietary concerns on a non-repatriation basis under the automatic route

- No upper limit on capital investment

- Permitted fund sources: inward remittance, NRE, NRO, or FCNR accounts

- Prohibited sectors: agriculture/plantation, real estate trading, print media

Repatriation rules:

- Business profits are freely repatriable after all applicable Indian taxes are paid

- Capital repatriation from NRO accounts is capped at USD 1 million per financial year

FEMA compliance is one of the more technically demanding aspects of running an Indian sole proprietorship from Singapore. VJM Global's India entry advisory team works specifically with NRIs and OCIs to navigate RBI guidelines, structure fund flows correctly, and maintain documentation that holds up under scrutiny.

When a Sole Proprietorship May Not Be the Right India Entry Choice

Singapore Pte. Ltd. Companies Cannot Use This Structure

A Singapore-incorporated private limited company (Pte. Ltd.) is treated as a foreign company under the Companies Act 2013. It cannot register a sole proprietorship in India, as a sole proprietorship is by definition an individual person's business.

Available India entry structures for foreign companies:

- Wholly Owned Subsidiary (WOS) — 100% FDI via automatic route; separate Indian company

- Branch Office (BO) — RBI approval required; can conduct commercial activities

- Liaison Office (LO) — RBI approval required; limited to communication/representational activities; cannot earn income

- Project Office — For specific project execution

For most Singapore Pte. Ltd. entities, VJM Global recommends a Wholly Owned Subsidiary — it offers legal independence, full operational flexibility, 100% foreign ownership under FDI policy, and access to India's tax treaty benefits.

Structural Limitations That Restrict Growth

Sole proprietorships are unsuitable when:

- Liability protection is needed (unlimited personal liability exposes all personal assets)

- Business plans to raise equity capital (sole proprietorships cannot issue shares)

- Multiple co-founders need formal profit-sharing arrangements

- Business continuity is important if the owner is incapacitated

- Formal contracts and bidding for government projects are planned

When to escalate to an alternative structure:

- Annual turnover expected to exceed GST thresholds quickly

- Business will employ a significant number of Indian staff

- Business model requires strong legal standing for contracts

- Professional services partnership (LLP is often preferred)

- Need for institutional credibility with suppliers, clients, or investors

Choosing the wrong structure at entry creates costly restructuring down the road. VJM Global's India entry consultations help Singapore businesses lock in the right structure before incorporation — not after.

Frequently Asked Questions

How much does it cost to register a sole proprietorship in India?

There is no single mandatory registration fee. Costs arise from obtaining a Shop and Establishment licence (varies by state and municipality, typically ₹2,500–₹10,000), GST registration (free online), and PAN application (approximately ₹110). Total setup costs are typically low, but professional advisory fees may apply for foreign nationals navigating the process.

How to register a proprietorship firm in India?

Follow five key steps: obtain PAN card, secure a registered Indian address, get a Shop and Establishment licence, register for GST if applicable, and open a business bank account. The full process typically takes 10–15 days with proper documentation.

How is a sole proprietorship different from an LLC?

A sole proprietorship has no separate legal identity and exposes the owner to unlimited personal liability. An LLC (Private Limited Company in India) is a registered corporate entity with limited liability for shareholders, formal governance requirements, and mandatory annual filings.

Can a Singapore national or foreign national register a sole proprietorship in India?

In practice, this structure is accessible only to NRIs and OCI cardholders who can obtain an Indian PAN and complete Aadhaar biometric enrolment in person. Singapore-incorporated entities cannot register a sole proprietorship — they must use a formal corporate structure such as a Private Limited Company or LLP.

What is the difference between a sole proprietorship and a private limited company in India?

The key distinction is tax treatment and capital access. A sole proprietorship's income is taxed under personal income tax slabs, while a Private Limited Company pays corporate tax and can raise external equity. The Private Limited structure also requires mandatory MCA filings and annual audits — obligations that don't apply to a sole proprietorship.

What are the ongoing compliance requirements for a sole proprietorship in India?

Core ongoing obligations include:

- Annual income tax return (business income taxed as personal income)

- Quarterly GST returns if registered (GSTR-1 and GSTR-3B)

- Shop and Establishment licence renewal per state requirements

- Professional tax filing where applicable

- TDS compliance if employing staff

Need expert guidance on India market entry? VJM Global has helped NRIs, OCIs, and international businesses establish and operate in India for 30+ years, with a 95% client retention rate. Our team handles business setup, FEMA compliance, tax planning, and ongoing regulatory filings — so you're not piecing together advice from multiple sources. Contact us at info@vjmglobal.com or call +91-9213397070 to discuss your India entry strategy.