The good news: Turkey places no nationality restrictions on company ownership, and 100% foreign ownership is permitted across most sectors. The challenge is that registration, tax, and documentation requirements involve multiple government bodies, strict apostille rules, and deadlines that trip up even experienced investors.

This guide covers everything you need — business structures, step-by-step registration, costs, and ongoing compliance — to make informed decisions before you begin.

Key Takeaways

- 100% foreign ownership is permitted; foreigners hold the same legal rights as Turkish investors

- LLC (Ltd. Şti.) is the fastest route for most first-time foreign investors; minimum capital is TRY 50,000

- Full registration takes 5–10 business days; end-to-end setup runs 2–3 weeks with correct documents

- Corporate income tax is 25% for 2026; VAT tiers are 20%, 10%, and 1%

- Turkey has 93 active Double Taxation Agreements covering most major economies, including the US, UK, Germany, and India

Why Set Up a Business in Turkey?

A Market Worth the Attention

Turkey's economy is growing, and foreign capital is following. GDP grew 3.2% in 2024 per World Bank data, with the IMF forecasting 4.1% growth for 2025. Full-year 2024 FDI reached USD 11.3 billion, and H1 2025 already reported USD 6.3 billion — suggesting the trend is holding.

The domestic consumer base stands at over 86 million people as of end-2025, making Turkey the largest market between the EU's eastern border and Central Asia.

The EU Customs Union — in force since 1 July 1996 and covering industrial goods and processed agricultural products — gives Turkish-based manufacturers meaningful access to European supply chains without the red tape of full EU membership.

The Regulatory Environment for Foreign Investors

That market access only matters if the legal framework lets you operate freely. Turkey's Foreign Direct Investment Law puts international investors on equal footing with domestic ones. Key features:

- 100% foreign shareholding permitted in most sectors

- No minimum local partner requirement

- One-stop-shop registration through the MERSIS digital system

- Automatic notification to tax authorities and Social Security Institution (SGK) after registration

High-Opportunity Sectors

Foreign capital has concentrated in specific areas where Turkey's geography, workforce, and infrastructure create natural advantages:

- Real estate and construction — driven by urbanisation and tourism demand

- Tourism and hospitality — Turkey ranks among the world's top five tourist destinations by arrivals

- Technology and startups — Istanbul has emerged as a regional tech hub with growing VC activity

- Manufacturing and exports — competitive labour costs and EU Customs Union access

- Renewable energy — government incentives for solar and wind projects

- Logistics — strategic position connecting Europe, the Middle East, and Central Asia

Types of Business Structures in Turkey

Most foreign investors choose between four structures. Two create a new Turkish legal entity; two operate as extensions of an existing foreign company.

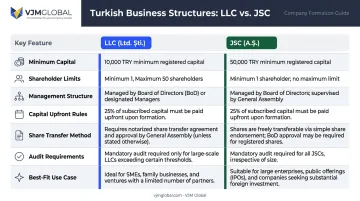

Comparing LLC vs. JSC: Which Is Right for You?

| Feature | LLC (Ltd. Şti.) | JSC (A.Ş.) |

|---|---|---|

| Minimum capital | TRY 50,000 | TRY 250,000 |

| Shareholders | 1–50 | Minimum 1 |

| Management | One or more managers | Board of directors |

| Capital upfront | Payable within 24 months | 25% required before registration |

| Share transfers | Requires notarial deed | By endorsement and delivery |

| Independent audit | Not automatic | Required above KGK thresholds |

| Best for | SMEs, first-time foreign investors | Larger operations, future IPO candidates |

Both structures permit 100% foreign ownership and provide limited liability to shareholders.

Branch Offices and Liaison Offices

Foreign companies that want a presence in Turkey without creating a separate Turkish entity have two options.

A Branch Office (Şube) is not a separate legal entity — it extends the foreign parent company directly. It can conduct commercial activities consistent with the parent's purpose and is registered through the standard trade registry process. The parent company bears full legal liability for the branch's obligations.

A Liaison Office (İrtibat Bürosu) is licensed by the Ministry of Industry and Technology, initially for up to three years. Liaison offices cannot engage in commercial activity — they exist for market research, promotion, and information gathering only. They carry no capital requirement and are tax-exempt, making them a practical entry point before committing to full incorporation.

Free Trade Zones

Turkey operates 19 free zones spread across major industrial and port cities including Istanbul, Izmir, Mersin, Antalya, Bursa, Gaziantep, and Trabzon. Businesses operating in free zones benefit from:

- Exemption from customs duties on goods entering the zone

- VAT exemption on goods and services supplied within the zone

- Corporate income tax exemption on income from goods produced in the zone (subject to statutory conditions)

The corporate income tax exemption applies specifically to production income — companies that only trade or distribute within a free zone do not qualify for this benefit.

Step-by-Step Guide to Setting Up a Business in Turkey

End-to-end setup typically takes 2–3 weeks when documents are prepared correctly, with formal registration alone requiring 5–10 business days. Documentation errors are the leading cause of delays, so accuracy at each step directly determines how fast your company gets operational.

Step 1: Choose Your Business Structure and Trade Name

Select your entity type based on business activities, planned capital, and long-term growth strategy. At the same time, choose a trade name that:

- Does not duplicate any existing registered name

- Is not misleading about the company's activities

- Has the main business activity described in Turkish, per the Regulation on Trade Names

Run a name availability check through the MERSIS system before finalising.

Step 2: Obtain a Tax Identification Number (TIN)

Every non-Turkish shareholder and board member must obtain a potential tax identification number from the relevant Turkish tax office before incorporation. This number is required to open a bank account and proceed with registration.

Required documents for the TIN application:

- Petition

- Copy of the Articles of Association

- Copy of the tenancy contract

- Power of attorney (if applying by proxy)

Step 3: Prepare and Notarize Required Documents

Core documents required for registration:

- Articles of Association — drafted and submitted through the MERSIS system

- Notarized passport copies of all shareholders

- Signature declarations for authorized signatories

- Company manager identity documents

- Proof of registered business address (lease agreement or property ownership documents)

Critical: All foreign-issued documents must be apostilled or ratified by the Turkish Consulate, then officially translated by a Turkish-certified notary. Incomplete apostilles alone account for a significant share of first-submission rejections — verify every foreign document before submitting.

Step 4: Register with the Trade Registry Directorate

After submitting the Articles of Association through MERSIS, founders appear in person at the relevant Trade Registry Directorate — located within the relevant Chamber of Commerce — with all notarized documents.

Once approved:

- The company is officially registered

- The Trade Registry Directorate automatically notifies the tax office and SGK

- A Turkish Trade Registry Gazette announcement is published within approximately 10 days

Step 5: Open a Corporate Bank Account and Deposit Capital

A Turkish corporate bank account is required to deposit minimum capital. Banks conduct AML/KYC checks and will request:

- Trade Registry documents

- Tax identification number

- Signature circular

- Notarized and translated passport copies

Capital deposit rules:

- LLC: Full TRY 50,000 may be deposited within 24 months of registration

- JSC: At least 25% of TRY 250,000 (TRY 62,500) must be deposited before registration

Major private Turkish banks offer English-language service and multi-currency accounts — recommended for foreign-owned companies managing cross-border payments.

Step 6: Complete Tax Registration, Social Security Enrollment, and Obtain Licenses

Post-registration steps that must not be overlooked:

- A tax officer visits the company headquarters to prepare a determination report

- Obtain a tax registration certificate from the local tax office

- Register the company with the Social Security Institution (SGK) to get a social security number

- Identify and apply for sector-specific licenses early — finance, healthcare, education, energy, and tourism all require ministry approvals before operations begin

Sector licensing timelines vary significantly by ministry and can add weeks to your launch schedule. Engaging a local legal or compliance advisor at this stage helps avoid operational delays from missed approvals.

Costs of Starting a Business in Turkey

The figures below reflect 2026 tariffs and schedules. Exchange rates shift frequently, so treat TRY amounts as the authoritative reference and convert at the official rate on your registration date.

Registration and Administrative Fees

| Cost Item | Approximate Amount (TRY) | Notes |

|---|---|---|

| Trade Registry fees | Varies by transaction | Ledger certification, establishment certification, gazette announcement |

| Notary fees | TRY 58.82 minimum per transaction; TRY 667.67/page for translations | 2026 tariff; total depends on document volume |

| Chamber of Commerce membership | TRY 3,305–TRY 4,600 annually for new capital companies | 2026 ITO schedule |

| Competition Authority contribution | 0.04% of registered capital | Formula-based, not fixed |

USD equivalents fluctuate with the TRY/USD exchange rate. Use the official rate on your registration date for conversion.

Minimum Capital Requirements

These are not fees. The capital must be deposited into the corporate account and forms part of the company's assets:

- LLC: TRY 50,000 (payable within 24 months of registration)

- JSC: TRY 250,000 (at least 25% before registration; remainder within 24 months)

Professional and Advisory Fees

Most foreign investors engage legal, accounting, and advisory support — language barriers, document complexity, and the risk of registration rejections make local expertise practical from day one. Costs vary by scope; request quotes from advisory firms directly, as fees depend on the services required.

Tax Obligations for Foreign-Owned Businesses in Turkey

Turkey's tax framework covers corporate income, VAT, withholding obligations, and social security contributions. Each has distinct rates and filing schedules that foreign-owned businesses must track from day one.

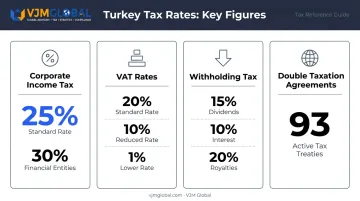

Corporate Income Tax

The standard corporate income tax (CIT) rate is 25% for 2025 and 2026 accounting periods. Banks, financial leasing companies, electronic payment institutions, insurers, reinsurers, and certain other financial entities are taxed at 30%.

- Resident companies (incorporated in Turkey) are taxed on worldwide income

- Non-resident entities (branches, liaison offices) are taxed only on Turkey-sourced income

VAT (Katma Değer Vergisi / KDV)

All businesses must register for VAT and file regular returns. Current rates:

- Standard rate: 20% (applies to most goods and services)

- Reduced rate: 10% (food, medical products, certain services)

- Lower reduced rate: 1% (basic foodstuffs, agricultural products, certain other goods)

The older 18%/8% framework no longer applies. The current tiers are 20%, 10%, and 1%.

Withholding Tax and Double Taxation Agreements

Payments to foreign shareholders and non-resident entities are subject to withholding tax at these domestic rates:

- Dividends: 15%

- Interest: 10% (general; exceptions apply for qualifying bank loans)

- Royalties: 20%

Turkey has 93 Double Taxation Agreements in force as of April 2025, covering major partners including the United States, United Kingdom, Germany, France, Netherlands, UAE, Saudi Arabia, and Australia. Treaty provisions can reduce applicable withholding rates — always check whether a DTA applies before structuring payments.

Social Security Contributions (SGK)

For each employee, both employer and employee contribute to SGK:

| Contribution | Rate |

|---|---|

| Employee (long-term insurance + health) | 14% of gross salary |

| Employer (long-term insurance + health) | 19.5% of gross salary |

| Unemployment insurance | 2% employer / 1% employee |

Monthly VAT and withholding tax declarations, annual corporate tax returns, and SGK filings are all recurring obligations. Late or missing filings carry real costs: for capital companies, first-degree irregularity penalties reach TRY 35,000 under 2026 GIB schedules. A qualified local accountant or outsourced compliance partner can manage these filing calendars and help avoid penalties before they accumulate.

Common Mistakes to Avoid When Setting Up a Business in Turkey

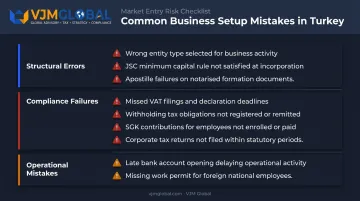

Structural and Documentation Errors

- **Choosing the wrong entity type** — selecting an LLC when future capital raises or a public offering requires a JSC forces costly restructuring later

- Underestimating the JSC upfront capital rule — the 25% pre-registration deposit (TRY 62,500) catches many investors off guard

- Incomplete or improperly apostilled documents — missing apostilles or untranslated foreign documents are the leading cause of registration rejections and delays

Post-Registration Compliance Failures

Many foreign founders treat company registration as the finish line. It is not. Ongoing obligations begin the moment the company is registered:

- Monthly VAT declarations

- Withholding tax filings

- Annual corporate tax returns

- SGK contributions for each employee

Missed filings trigger financial penalties, delay interest, and can result in losing investment incentives that took months to qualify for.

Operational Mistakes

- Open the corporate bank account early — capital deposits and operational payments both require it, and delays here stall the entire final stage of setup

- Obtain a work permit before acting as director — owning a Turkish company does not authorize you to work in Turkey. Any foreign national signing contracts, directing operations, or drawing a salary must hold a work permit issued by the Ministry of Labor and Social Security. Operating without one is unlawful.

Frequently Asked Questions

How much does it cost to start a business in Turkey?

Minimum capital is TRY 50,000 for an LLC and TRY 250,000 for a JSC. Add notary, translation, Chamber of Commerce membership, and Competition Authority contribution fees — exact totals vary by document volume and company type. Professional advisory fees are additional and quoted on a case basis.

Can a foreigner start a business in Turkey?

Yes. Turkey permits 100% foreign ownership in most sectors with no nationality restrictions. Foreign investors have the same legal rights and obligations as Turkish nationals under the Foreign Direct Investment Law.

Is Turkey a good place to do business?

Turkey offers real advantages: 86+ million consumers, EU Customs Union access for industrial goods, government incentives, and competitive costs. The main challenges are bureaucratic complexity and language barriers, both of which are manageable with the right local expertise.

Which business is most profitable in Turkey?

Real estate, tourism and hospitality, manufacturing and exports, technology, and logistics attract foreign capital. Profitability depends on sector expertise, entry timing, and local market execution.

How long does it take to register a company in Turkey?

Formal registration takes 5–10 business days. The full end-to-end process — including bank account opening and social security enrollment — typically takes 2–3 weeks when all documents are correctly prepared and apostilled before submission.

What are the ongoing compliance requirements for a registered company in Turkey?

Registered companies must file monthly VAT and withholding tax declarations, submit annual corporate tax returns, make SGK contributions for all employees, and update the Trade Registry for any changes in ownership, management, or registered address.