Introduction

Over 12,000 Australian companies export to the United States, yet many founders arrive at the US market with a critical blind spot: assuming the setup process mirrors what they know from home. It doesn't.

The US operates on state-by-state registration, has no equivalent to ASIC for federal company formation, and imposes separate federal and state tax obligations from day one. Get this wrong and the consequences stack up fast:

- Restructuring a poorly chosen entity is expensive and time-consuming

- Missing a state nexus trigger exposes you to back taxes and penalties

- Choosing the wrong entity type complicates your Australian tax position unnecessarily

This checklist covers every major step Australian business owners need to complete before and after launching in the USA — from entity selection and EIN registration to banking, trademarks, and ongoing compliance obligations.

Key Takeaways

- Non-residents can legally register a US LLC or C-Corp without citizenship or residency

- State selection affects tax rates, ongoing fees, and where you must also register if operating locally

- EIN applications for non-residents require IRS Form SS-4 submitted by fax or phone, EIN applications for non-residents require IRS Form SS-4 submitted by fax or phone; the online portal is not available to foreign applicants

- Opening a US bank account is often the hardest practical step — fintech platforms tend to have fewer barriers than traditional banks for non-residents

- The US-Australia Double Tax Agreement reduces but does not eliminate cross-border tax complexity

What Setting Up a US Business Actually Means for Australians

Setting up a US business from Australia means incorporating a legal entity under US law, obtaining federal and state tax registrations, and building the operational infrastructure — banking, address, registered agent — needed to legally conduct business in the US.

This is different from simply selling into the US. An Australian business that exports products or delivers digital services from Australia — without a US entity, employees, or physical presence — doesn't automatically trigger US corporate law or full US tax obligations.

That changes once you form a US entity, hire staff, or establish a physical presence. From that point, you're subject to compliance requirements at both the federal and state level.

The key structural difference is that unlike Australia, where companies register federally through ASIC, the US operates on a state-by-state model. Your choice of registration state affects:

- Corporate income tax rates

- Annual filing fees and franchise taxes

- Ongoing compliance requirements

- Where you may also need to register if you operate in another state

Why Australian Businesses Expand to the USA

DFAT reports A$98.6 billion in Australia-US goods and services trade in 2025, with Australian investment in the US reaching A$1.64 trillion. Beyond market scale, businesses are drawn by USD revenue, access to the US$637 billion federal procurement market, and proximity to US venture capital.

How AUSFTA Helps

Two key agreements reduce friction for Australian businesses entering the US market:

- AUSFTA (in force since 1 January 2005) eliminates tariffs on over 99% of qualifying manufactured goods, opens services markets, and strengthens IP protection

- US-Australia Double Tax Agreement (DTA) prevents double taxation on profits earned in the US and repatriated to Australia

- Together, they create a more predictable operating environment than most other cross-border expansions

What Australians Consistently Underestimate

The shared language creates a false sense of familiarity. In practice:

- US corporate law is state-governed and far more fragmented than Australia's

- Employment obligations differ significantly — no superannuation, no NES equivalent, at-will employment in most states

- Upfront compliance costs are higher than expected

- Consumer protection laws and IP registration systems are entirely separate from Australia's

The Complete USA Business Setup Checklist for Australian Businesses

Step 1 – Choose Your Business Structure

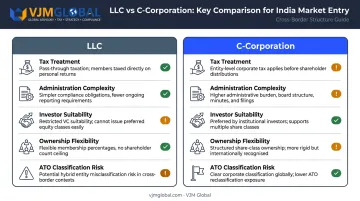

Two entity types are available to non-resident Australians:

| Feature | LLC | C-Corporation |

|---|---|---|

| Tax treatment | Pass-through (default) | 21% federal corporate tax |

| Administration | Simpler | More complex |

| Investor suitability | Harder to structure equity | Preferred by VCs |

| Ownership restrictions | Flexible | Flexible for non-residents |

| ATO classification risk | Foreign hybrid issue | Cleaner treatment |

LLCs suit service-based businesses and solo founders who want lighter compliance. One complication to plan for: the ATO may classify a US LLC as a "foreign hybrid company" under Australian tax law, treating Australian members as partners rather than shareholders. This creates tax complexity that catches many founders off guard.

C-Corporations are preferred if you're raising venture capital, issuing equity to multiple investors, or want a cleaner separation between the Australian parent and the US entity. IRS Publication 542 confirms C-Corps pay a flat 21% federal corporate income tax.

One clear rule: S-Corporations are not available to non-US residents. The IRS prohibits non-resident alien shareholders. Don't let a US-based adviser recommend this structure without flagging this exclusion.

Foreign-owned single-member LLCs also face an important reporting obligation: IRS Form 5472 must be filed annually, with a $25,000 penalty for incomplete or missing filings.

Choose your structure before registering. Restructuring after the fact is costly and triggers additional legal and tax work on both sides of the Pacific.

Step 2 – Choose the Right State and Register

Delaware and Wyoming are the most popular choices for non-resident Australians:

- Delaware: Strong, well-tested corporate law; no state income tax on out-of-state activities; LLC formation fee from $110; annual LLC tax $300

- Wyoming: No corporate or personal state income tax; LLC Articles of Organization filing fee $100; minimal annual compliance obligations

However, if your business will physically operate, employ staff, or generate revenue in another state (California or Texas, for example) you'll need to foreign qualify in that state as well. That means two sets of registrations, two sets of fees, and two sets of compliance obligations.

California imposes an $800 minimum franchise tax on corporations incorporated, registered, or doing business there. Texas charges $750 for most foreign entity registrations.

Core registration steps:

- Check name availability in your chosen state

- Appoint a registered agent (required to receive legal documents; costs typically $50–$125/year)

- File Articles of Incorporation (C-Corp) or Articles of Organization (LLC)

- Pay the applicable state filing fee

- Obtain your Certificate of Formation or Incorporation

Step 3 – Obtain an EIN and Register for Taxes

The Employer Identification Number (EIN) is the US equivalent of an ABN. You need it to open a business bank account, hire employees, file taxes, and apply for licences.

Non-residents cannot use the IRS online EIN portal — it requires a US principal address and valid US taxpayer ID. Instead, apply through one of these channels:

- Phone (international applicants only): Immediate issuance during the call if eligible

- Fax (Form SS-4): Generally processed within 4 business days with a return fax number

- Mail: Approximately 4 weeks

On line 7b of Form SS-4, where it asks for the responsible party's SSN or ITIN, non-residents without one should enter "foreign" or "N/A."

Beyond the EIN, you'll need:

- Federal corporate income tax registration (C-Corps: 21% flat rate)

- State-specific sales tax registration where applicable

- Industry-specific permits or licences

US sales tax is state-governed, unlike Australia's GST. Rates vary by state, and not every state collects it. Since the Wayfair ruling, economic nexus thresholds commonly apply once you exceed $100,000 in sales or 200 transactions in a state — physical presence is no longer required to trigger an obligation.

Step 4 – Open a US Business Bank Account

This is consistently the most practically difficult step. Most major US banks (Chase, Bank of America, Wells Fargo) require in-person identity verification, a US address, and supporting corporate documents, which creates real friction for Australian non-residents.

Options for non-residents:

- Visit the US to open an account in person at a traditional bank

- Mercury and Relay both support US entities owned by non-US residents, though each applies country restrictions and operating presence requirements — you'll need your EIN and entity documents regardless

- Some cross-border business setup firms maintain facilitation relationships with banking providers

Don't assume a fintech account is guaranteed. Both Mercury and Relay apply country screening and activity-based eligibility checks. Confirm your eligibility before committing to a banking strategy.

Step 5 – Assess Visa and Immigration Requirements

Owning a US business does not grant the right to live or work in the USA. This is a common source of confusion. You can incorporate an LLC or C-Corp in Delaware from your desk in Melbourne and remain legally compliant, but moving to the US to run that business requires the appropriate visa.

The most relevant visa options for Australians:

- E-2 Treaty Investor Visa: Available to Australians under AUSFTA. Requires a substantial investment in a bona fide enterprise and entry solely to develop or direct it. No fixed dollar minimum, but investment must be proportional to total enterprise cost.

- O-1A Visa: For individuals with extraordinary ability in business, sciences, or education

- L-1A Visa: For intracompany transferees — executives or managers who have worked at the Australian entity for at least one continuous year in the prior three years

Visa applications are entirely separate from entity formation. Build both timelines in parallel, not sequentially.

Step 6 – Register Trademarks, Protect IP, and Manage Ongoing Compliance

An Australian trademark does not automatically protect your brand name or logo in the US. US trademark rights are territorial. File with the USPTO before or immediately after entering the US market.

Key points for Australian applicants:

- Foreign-domiciled applicants must use a US-licensed attorney (USPTO rule effective 3 August 2019)

- Current base application fee: $350 per class (effective January 2025 — the old TEAS Plus/Standard structure no longer applies)

Ongoing compliance obligations after setup:

- Annual state reports and franchise tax filings

- Federal corporate tax returns (Form 1120 for C-Corps; Form 5472 for foreign-owned LLCs)

- Payroll tax filings if hiring US employees (Forms 941, 940, W-2)

- Maintaining a registered agent in your formation state

- Sales tax filings in any state where you've triggered economic nexus

Managing compliance across two jurisdictions adds up quickly. VJM Global works with Australian businesses on cross-border tax planning and ongoing US compliance — covering both Australian and US obligations so founders don't have to coordinate between separate advisers.

Key Tax and Compliance Considerations

Federal and State Tax Rates

| Jurisdiction | Tax | Rate |

|---|---|---|

| Federal (C-Corp) | Corporate income tax | 21% |

| Delaware | Corporate income tax (in-state activity only) | 8.7% |

| California | Corporate income tax | 8.84% |

| Florida | Corporate income tax | 5.5% |

| Wyoming | Corporate income tax | None |

| Texas | Franchise tax | 0.375%–0.75% |

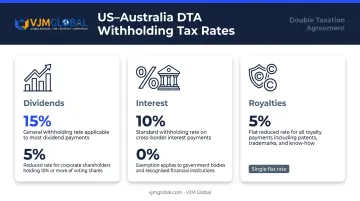

The US-Australia Double Tax Agreement

The DTA prevents Australian businesses from being taxed on the same income twice. IRS Treaty Table 1 sets the following withholding tax rates for payments from the US to Australian recipients:

- Dividends: 15% general; 5% for corporate beneficial owners holding at least 10% voting stock

- Interest: 10% general (0% for certain government and financial institution cases)

- Royalties: 5%

These rates matter when repatriating profits from a US C-Corp to an Australian parent. For LLCs, the hybrid entity classification under the DTA requires separate analysis : the ATO treats US LLCs as foreign hybrid companies (partnerships), which changes how Australian-resident members report income from the entity.

Tax structure is only part of the compliance picture. Once you hire in the US, a separate set of employment obligations applies — and most Australian defaults don't carry over.

Employment Law: What Changes When You Hire in the US

Australian employment assumptions don't transfer:

- No equivalent to superannuation — US retirement plans (401k) are voluntary and employer contributions are discretionary

- At-will employment applies in all states except Montana, meaning either party can end employment at any time (with limited exceptions for contracts and public policy)

- Federal minimum wage: $7.25/hour, with many states setting higher rates

- Overtime: Mandatory at 1.5x regular rate after 40 hours in a workweek under the Fair Labor Standards Act

- State-specific minimum wages and leave laws vary significantly

Common Mistakes Australians Make When Setting Up in the USA

These four mistakes trip up Australian founders more than any others — and most are entirely avoidable with early planning.

Assuming Australian rules apply. Shared language doesn't mean shared regulation. US corporate law, employment obligations, consumer protection, and IP systems each operate independently from Australia's frameworks.

Registering only in Delaware when operating elsewhere. Delaware is popular for incorporation, but if your business operates physically in California or Texas, you must also foreign qualify in those states — incurring additional fees and compliance obligations.

Overlooking the Australian tax consequences. A US entity structure creates obligations back home too: offshore income reporting, potential transfer pricing rules for subsidiary arrangements, and the need to correctly classify your US entity under the Double Tax Agreement (DTA) to access treaty benefits.

Underestimating how long setup actually takes. Getting a US company fully operational takes longer than most Australians expect. A realistic timeline:

| Step | Typical timeframe |

|---|---|

| State registration | 2 business days to several weeks (varies by state) |

| EIN (fax) | ~4 business days |

| EIN (mail) | ~4 weeks |

| Bank account opening | Days to weeks (fintech); longer for traditional banks |

| Full operational readiness | Several weeks to several months |

Plan your US market entry at least 2–3 months before your intended launch date — and engage a cross-border tax adviser early to avoid compliance gaps on both sides of the Pacific.

Frequently Asked Questions

Can I start a business in the US if I'm from Australia?

Yes. Non-residents, including Australians, can register an LLC or C-Corp in the USA without US citizenship or residency. No visa is required to own a US business — but one is required if you want to physically live and work there.

Do Australian businesses need a US visa to set up a company?

No visa is needed to register a US company. If you plan to physically manage operations from within the US, however, you'll need an appropriate visa. The E-2 Treaty Investor Visa is the most relevant option for Australians wanting to work on-site.

What is the best US state for Australian businesses to register?

Delaware and Wyoming are the most popular for non-residents — both offer tax advantages and well-established corporate law. If your business operates physically in another state, you'll likely need to register there as well, triggering additional fees and obligations.

What are the tax obligations for Australian companies in the USA?

C-Corps pay a 21% federal corporate income tax. State income taxes vary (Wyoming has none; California charges 8.84%). The US-Australia DTA reduces withholding taxes on dividends, interest, and royalties repatriated to Australia, but cross-border tax planning is essential.

What business can I start with $10,000 USD in the USA?

$10,000 is sufficient to cover LLC or C-Corp formation fees, registered agent costs, and an EIN for service-based businesses such as consulting, digital services, or e-commerce. Capital-intensive industries like retail, manufacturing, or hospitality typically require $50,000 or more to get started.

Can an Australian citizen live permanently in the USA?

Permanent US residency requires a Green Card through employment sponsorship, family relationships, or investment (EB-5 visa). Owning a US business alone does not grant permanent residency. The E-2 visa is renewable indefinitely but does not lead directly to a Green Card.