Introduction

Singapore investors setting up Dubai holding structures run into a consistent problem: most setup guides are written for generic "foreign investors." They don't address Singapore-specific documentation requirements, the UAE-Singapore tax treaty relationship, or how cross-border ownership works when the shareholder is a Singapore-incorporated entity. Dubai's zero-tax environment and its position as a gateway between Asia and the Gulf make it genuinely attractive — but only if you understand how its rules apply to you specifically.

The questions that matter are practical ones: How do Dubai holding company regulations apply to a Singapore corporate shareholder? What does the apostilling process look like for Singapore incorporation documents? Which jurisdiction — Mainland, DIFC, or ADGM — offers the best trade-off between cost and credibility for managing regional subsidiaries or IP portfolios?

This article answers those questions directly. We cover what a holding company license in Dubai is, why it matters for Singapore investors, the structures available, the step-by-step registration process, and a full cost breakdown.

Key Takeaways

- A Dubai holding company license lets Singapore investors legally own subsidiaries, shares, IP, and assets under one entity without direct trade operations

- Dubai offers 0% corporate tax on qualifying income, 100% foreign ownership in free zones, and a Singapore-inclusive Double Tax Treaty network covering 137+ countries

- Three main structures to choose from: mainland (broader market access), free zone (DIFC, DMCC, RAKEZ), or offshore via RAK ICC for the lowest setup cost

- Registration takes 3–15 business days for free zone entities; Singapore corporate shareholders need apostilled documents

- Total costs vary by jurisdiction — free zone licenses start from AED 12,500 and offshore from AED 7,200

What Is a Holding Company License in Dubai?

A holding company license in Dubai authorizes an entity to own shares in other companies, hold assets such as real estate, intellectual property, and investments, and manage subsidiaries. Income flows through dividends, royalties, rental income, and capital gains — not through operational trade. Direct commercial activities are handled exclusively through subsidiaries.

The UAE Commercial Companies Law (Federal Decree-Law No. 32 of 2021, Articles 268-275) formally defines this structure. Under Article 269, holding companies are restricted to five permitted activities:

- Holding shares in other companies

- Providing loans or guarantees to subsidiaries

- Acquiring real estate and movable assets

- Managing subsidiary operations

- Acquiring intellectual property

Direct commercial operations are prohibited. All trading must happen through subsidiaries, not the holding entity itself.

This distinguishes the holding license from other UAE license types:

| License Type | Permitted Activities |

|---|---|

| Holding | Own assets, manage subsidiaries, collect dividends/royalties |

| Trading | Buy, sell, and import goods |

| Professional | Consultancy, advisory, and service delivery |

Compliance Obligations

UBO Registration: Cabinet Decision No. 58 of 2020 requires all UAE entities to register Ultimate Beneficial Owners with their licensing authority. Singapore investors must disclose name, nationality, passport details, residential address, and the basis of ownership.

Audited Financial Statements: From tax periods starting 1 January 2025, Ministerial Decision No. 84 of 2025 requires Qualifying Free Zone Persons to maintain IFRS-audited accounts prepared by a UAE-licensed auditor. Most free zones also require audited financials for annual license renewal.

Annual License Renewal: UAE holding licenses must be renewed each year. Late or missed renewals attract penalties and risk license suspension.

Why Singapore Investors Are Setting Up Holding Companies in Dubai

The 17% vs. 0% Tax Differential

Singapore imposes a flat 17% corporate income tax on chargeable income. The UAE, by contrast, offers 0% corporate tax on qualifying income for Qualifying Free Zone Persons under Federal Decree-Law No. 47 of 2022. Article 18 provides this 0% rate if the entity:

- Maintains adequate substance in the UAE

- Derives qualifying income as specified

- Has not elected standard tax rates

- Complies with transfer pricing and documentation requirements

- Meets additional ministerial conditions

For Singapore investors, the 17-percentage-point gap creates a clear structuring advantage. A Dubai holding company structured as a QFZP receives dividends from subsidiaries at 0% UAE corporate tax, versus the 17% rate applied when routed through a Singapore parent.

That said, failing any of the five conditions above results in losing QFZP status retroactively from the beginning of that tax period — making compliance non-negotiable.

The Singapore-UAE Double Tax Agreement

Singapore and the UAE signed the Agreement for the Avoidance of Double Taxation on 1 December 1995. It entered into force on 30 August 1996 and applies from 1 January 1992.

Treaty Rates:

- Dividends: 5% maximum withholding tax (Article 10)

- Interest: 7% maximum (Article 11)

- Royalties: 5% maximum (Article 12)

Since the UAE currently levies no withholding tax on dividends, interest, or royalties domestically, the treaty's practical value lies in:

- Legal certainty against future WHT imposition

- Singapore-side foreign tax credit claims

- Mutual agreement procedure for dispute resolution

UAE Treaty Network and Market Access

That treaty protection becomes even more useful when layered with the UAE's broader network. The UAE has concluded 137 Double Taxation Agreements with key trade partners — a substantially wider reach than Singapore's network alone. For investors, a Dubai holding company becomes a regional hub for the Middle East, Africa, and Central/South Asia, with treaty-protected income flows into each jurisdiction.

Bilateral trade between Singapore and the UAE reached S$27.94 billion in goods, with the UAE positioned as a strategic re-export hub connecting Singapore to broader Middle Eastern and African markets.

Asset Protection and Structuring Benefits

A Dubai holding company allows Singapore investors to ringfence operational risk. If a subsidiary faces legal or financial issues, creditors cannot pierce the holding company structure to reach assets held at the parent level. Key protections this structure provides:

- Isolates subsidiary liabilities from the holding company's asset base

- Preserves capital in the parent entity during subsidiary insolvency proceedings

- Enables clean portfolio separation across different industries or geographies

100% Foreign Ownership

Federal Decree-Law No. 26 of 2020, effective 1 June 2021, abolished the requirement that UAE nationals hold at least 51% of onshore company shares. Singapore citizens and companies can now own 100% of Dubai holding structures in both mainland and free zone jurisdictions, with no UAE national sponsor required.

Types of Dubai Holding Company Structures: What Singapore Investors Should Know

Free Zone, Offshore, and Mainland Comparison

| Jurisdiction | Entity Types | Key Advantages | Limitations | Best For |

|---|---|---|---|---|

| Mainland (DED) | LLC | Full UAE market access; 100% foreign ownership since 2021 | Requires physical office lease (Ejari); higher costs | Groups needing to trade across emirates |

| Free Zone (DIFC, DMCC, RAKEZ) | FZ LLC, FZE | 100% ownership; 0% QFZP tax rate; streamlined registration | Cannot trade directly in UAE mainland without distributor | Tax-efficient holding and investment structures |

| Offshore (RAK ICC) | IBC, Foundation | Lowest cost; minimal overhead | No UAE market trading rights | Pure asset/share holding; succession planning |

Of these three jurisdictions, free zone and offshore structures attract most Singapore investors. Here are the five zones most commonly used for holding company setups.

Most Relevant Free Zones for Singapore Investors

DIFC (Dubai International Financial Centre):

- Operates under independent English common law framework

- Prescribed Company vehicle: USD 100 incorporation + USD 1,000/year renewal

- DFSA regulates financial services activities

- Ideal for investment holding, fund structures, and legal certainty

- Widely used in cross-border investment and fund structures

DMCC (Dubai Multi Commodities Centre):

- Over 1,000 activity codes; minimum share capital typically AED 50,000

- From AED 20,285/year license fee

- Strong ecosystem for commodity-linked groups

- Processing time: ~2 weeks

RAKEZ (Ras Al Khaimah Economic Zone):

- Cost-conscious option starting from ~AED 5,499/year with flexi-desk

- Customized packages for different business needs

- Free zone and non-free zone options available

- Fastest approval timelines

RAK ICC (RAK International Corporate Centre):

- Offshore IBC: AED 3,250 incorporation; AED 3,950 annual renewal

- Cannot trade directly in UAE market

- Processing: 3-5 working days

- Lowest-cost entry point for pure holding structures

JAFZA (Jebel Ali Free Zone):

- Dedicated Holding License: AED 30,000

- Minimum capital requirement: AED 10 million

- Must hold 3+ companies

- Processing: ~21 working days

- Suited to institutional-scale groups with significant capital requirements

Legal Entity Types

- FZ LLC (Free Zone Limited Liability Company) — supports multiple shareholders; commonly used by Singapore corporate shareholders setting up regional subsidiaries

- FZE (Free Zone Establishment) — single-shareholder structure; suited to Singapore entrepreneurs or companies establishing a wholly-owned holding entity

- Foundation (DIFC) — standalone legal entity with no shareholders; used for multigenerational wealth transfer, confidential beneficiary designations, and Shari'ah-compliant structures

- IBC (International Business Company) — RAK ICC offshore vehicle for holding shares globally; no UAE market trading rights

Step-by-Step: How to Register a Holding Company in Dubai

Step 1 — Define Business Objectives and Choose a Jurisdiction

Singapore investors should first clarify the holding company's primary purpose:

- Tax planning and optimization: Free zone QFZP structures (DIFC, DMCC, RAKEZ)

- Asset protection and succession: DIFC Foundation or RAK ICC

- IP holding and licensing: Free zone structures with IP-specific activities

- Managing UAE/GCC subsidiaries: Mainland or free zone depending on market access needs

- Global investment management: Offshore RAK ICC or DIFC Prescribed Company

The answer determines whether mainland, free zone, or offshore is the right fit.

Step 2 — Select Legal Structure and Reserve Trade Name

Once the jurisdiction is chosen:

- Select entity type (FZE for single shareholder, FZ LLC for multiple shareholders, Foundation for succession)

- Confirm eligible business activities (e.g., "holding of shares," "management of investments," "IP holding and licensing")

- Apply for trade name approval from the relevant authority

- Ensure the name includes "holding company" designation per UAE Commercial Companies Law

Step 3 — Prepare and Submit Documentation

For Individual Singapore Shareholders:

- Valid passport copy (minimum 6 months validity)

- Proof of residential address (utility bill or bank statement)

- Bank reference letter

- Source of funds declaration

- Completed application form with passport-sized photographs

For Corporate Singapore Shareholders:

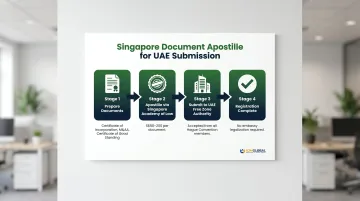

- Certificate of Incorporation (apostilled)

- Memorandum and Articles of Association (apostilled)

- Board Resolution authorizing UAE entity formation

- Certificate of Good Standing (apostilled)

- Shareholder and director passport copies

- Audited financial statements of the parent company

- UBO declaration

Singapore Apostille Convention: Singapore deposited its instrument of accession to the Hague Apostille Convention on 18 January 2021. Singapore-origin corporate documents can now be apostilled directly through the Singapore Academy of Law, eliminating multi-step embassy legalization. UAE free zones accept apostilled documents from all Hague Convention member states.

Professional Advisory Support: Working with a business setup advisor such as VJM Global — which specializes in cross-border accounting, international tax planning, and legal entity setup — helps Singapore investors ensure their documentation meets UAE authority standards and avoid processing delays.

Step 4 — Submit Application, Sign MOA, and Receive License

- Pay initial registration fee

- Sign the Memorandum of Association (MOA)

- Complete UBO registration (mandatory under UAE AML regulations)

- Receive the trade license and share certificate

Typical approval timelines:

- Free zone entities: 3–7 business days

- Mainland: 7–15 business days

- RAK ICC: 3–5 working days

- JAFZA holding license conversion: ~21 working days

Step 5 — Open a Corporate Bank Account

After license issuance, Singapore investors must open a UAE corporate bank account to make the holding company fully operational.

Required documents:

- Trade license

- MOA and share certificate

- Business plan

- Source of funds declaration

- UBO documents

- Passport copies and proof of address

Banking timeline: Due diligence is rigorous; onboarding typically takes 2–6 weeks.

Major UAE banks accepting free zone holding companies:

- Emirates NBD (minimum fixed deposit: AED 10,000)

- Mashreq Bank

- Abu Dhabi Commercial Bank (ADCB)

Minimum balance requirements: Typically AED 25,000 to AED 50,000 to avoid monthly maintenance fees, though this varies significantly by bank and package tier.

Step 6 — Ongoing Compliance After Registration

Singapore investors must maintain the following on an ongoing basis:

Economic Substance Regulations (ESR): Holding Company Business is a Relevant Activity under UAE MOF ESR framework. Holding companies benefit from reduced substance requirements but must still file:

- Annual Notification within 6 months of year-end

- Economic Substance Report within 12 months if income is earned

- Penalties: AED 20,000 (Notification failure), AED 50,000 (Report failure)

Corporate Tax Registration: The UAE Federal Tax Authority confirms that all Free Zone Persons must register for Corporate Tax regardless of QFZP status — including dormant holding companies.

Annual Audit: All QFZPs must maintain IFRS-audited financial statements by a UAE-licensed auditor (Ministerial Decision No. 84 of 2025). Budget AED 15,000–50,000+ annually.

UBO Register: Keep Ultimate Beneficial Owner information current with your licensing authority.

License Renewal: Submit renewal applications and fees before expiry to avoid penalties.

How Much Does a Holding Company License Cost in Dubai?

Cost Components Overview

Total cost comprises:

- License fee (registration and annual)

- Office or flexi-desk requirement

- Visa allocations (if residency needed)

- Notarization/apostille fees for Singapore documents

- Professional service fees

- Corporate bank account minimum balance

- Annual audit fees (mandatory for QFZPs)

Comparative Fee Schedule by Jurisdiction

| Jurisdiction | Incorporation | Annual License | Min Share Capital | Office/Flexi-Desk | First-Year Total (Approx) |

|---|---|---|---|---|---|

| RAK ICC (Offshore) | AED 3,250 | AED 3,950 | None | N/A (offshore) | ~AED 7,200 |

| RAKEZ (Free Zone) | Included | From ~AED 5,499 | None | From ~AED 4,000/yr | ~AED 9,500+ |

| DMCC | AED 9,000 | From AED 20,285 | ~AED 50,000 | Included in packages (from AED 35,480) | ~AED 35,000–50,000 |

| DIFC Prescribed Co | USD 100 | USD 1,000 | None | Physical required | ~AED 10,000+ |

| DIFC Standard LLC | ~USD 8,000 | ~USD 12,000 | None | Physical required | ~AED 75,000+ |

| JAFZA | AED 30,000 | Included | AED 10,000,000 | Physical required | AED 10,030,000+ |

| DED Mainland | ~AED 10,000–15,000 | ~AED 15,000–50,000 | Varies | Mandatory Ejari lease (AED 50,000–150,000/yr) | ~AED 75,000–200,000+ |

DIFC fees are denominated in USD; AED equivalent at approximately 3.67 per USD.

Key Insight: RAK ICC offers the lowest entry cost at approximately AED 7,200 for the first year (incorporation plus registered agent fees), while JAFZA's AED 10 million minimum capital requirement makes it suitable only for large corporate groups.

Additional Costs Singapore Investors Should Anticipate

Beyond the jurisdiction fees above, budget for these recurring and one-time costs before committing to a structure:

| Cost Item | Amount | Notes |

|---|---|---|

| Singapore document apostille | S$50–200 per document | Via Singapore Academy of Law |

| UAE investor/residence visa | AED 3,500–6,500 per person | Includes processing and government fees |

| Corporate bank account minimum balance | AED 10,000–50,000 | Deposit (locked capital), not a fee |

| Annual audit fees (QFZP) | AED 15,000–50,000+ | Mandatory under Ministerial Decision No. 84 of 2025; non-compliance triggers 9% tax for 5 years |

| ESR filing penalties | AED 20,000 (Notification) / AED 50,000 (Report) | Filing cost typically absorbed by compliance firm |

| Annual license renewal | Varies by jurisdiction | See comparison table above |

Free Zone vs. Mainland Cost Difference

Free zone licenses are more cost-effective for most Singapore investors, starting around AED 9,500 at RAKEZ. The primary cost driver for mainland setups is the mandatory Ejari-registered office lease, which adds AED 50,000–150,000 per year on top of DED registration fees.

RAK ICC offshore structures cost the least at ~AED 7,200 for year one, but that low cost reflects a trade-off: offshore entities cannot trade within the UAE domestic market. For Singapore investors using Dubai purely as a holding layer for regional or global subsidiaries, that restriction rarely matters. For those who need UAE market access, a free zone or mainland structure is the more practical fit.

Frequently Asked Questions

What is a holding company in the UAE?

A UAE holding company is a legal entity that owns shares in subsidiary companies and holds assets such as real estate, IP, and investments — without engaging in direct trade or day-to-day operations. It earns income through dividends, royalties, and capital gains.

How to register a holding company in Dubai?

Registration involves choosing a jurisdiction (free zone, mainland, or offshore), selecting a legal structure, submitting apostilled corporate documents, signing the MOA, and paying registration fees. Free zone setups typically complete in 3–10 business days.

Does a holding company need to be registered?

Yes. A holding company must be formally registered with the relevant UAE authority (DED for mainland, or the respective free zone authority) and must obtain a valid trade license. Post-2023, it must also register with the Federal Tax Authority for corporate tax purposes, regardless of whether it qualifies for 0% QFZP status.

How much does it cost to register a holding company in Dubai?

Costs vary by jurisdiction. Free zone licenses start from around AED 12,500 (RAKEZ), while RAK ICC offshore incorporation starts at AED 7,200. DIFC and mainland structures cost more. Additional expenses — office space, visa allocations, apostille fees, and annual audits — can add significantly to the total.

Can a Singapore company be the shareholder of a Dubai holding company?

Yes. A Singapore-registered company can be a corporate shareholder of a Dubai holding company. The Singapore entity must provide apostilled incorporation documents, a Board Resolution, Certificate of Good Standing, audited financials, and UBO disclosure for UAE registration.

Is there a double tax treaty between Singapore and the UAE?

Yes. The Singapore-UAE Double Taxation Agreement was signed on 1 December 1995 and has been in force since 30 August 1996. The treaty caps withholding tax at 5% on dividends, 7% on interest, and 5% on royalties. Since the UAE currently levies no domestic WHT, the treaty primarily provides legal certainty against future imposition and facilitates Singapore-side foreign tax credit claims.