Introduction

VAT on services in the UK is not a single flat rate. It shifts depending on the type of service, whether the transaction is B2B or B2C, and whether either party is based overseas. Misclassifying a service can mean HMRC penalties, lost input VAT reclaims, or an unexpected VAT bill landing on a client who wasn't expecting one.

Many service businesses struggle with three specific problems: identifying which VAT rate applies to their service category, knowing when registration becomes mandatory, and navigating cross-border supply rules after Brexit.

This guide covers UK VAT rates by service type, the current £90,000 registration threshold, place of supply rules, the exempt vs. zero-rated distinction, and the accounting schemes available to service businesses. Foreign businesses — particularly those from India, the US, or Australia supplying professional services into the UK — will find the registration and place of supply sections especially relevant.

Key Takeaways

- The UK has three VAT rates (20%, 5%, 0%) plus an exempt category ; which rate applies depends on the type of service

- The mandatory VAT registration threshold is £90,000 in taxable turnover over any rolling 12-month period (from April 2024)

- B2B services supplied to overseas business clients are typically outside the scope of UK VAT under place of supply rules

- Exempt services cannot recover input VAT, which is a real cash flow cost that must be built into your pricing

- Non-UK established businesses face no registration threshold: UK VAT registration is required from the very first taxable supply

What VAT on Services Actually Means in the UK

VAT is an indirect consumption tax, collected by VAT-registered businesses on behalf of HMRC and ultimately borne by the end consumer. The Value Added Tax Act 1994 is the primary legislation governing both goods and services. VAT has applied in the UK since 1 April 1973, when it replaced the earlier Purchase Tax regime under the Finance Act 1972.

Output VAT vs. Input VAT

The structural distinction that matters most for service businesses:

- Output VAT: VAT you charge on the services you sell and account for to HMRC

- Input VAT: VAT you pay on your own business purchases and expenses, reclaimable if those purchases relate to taxable supplies

For service businesses, this distinction is significant. Unlike product-based businesses with substantial goods purchases, many service firms have limited input VAT to reclaim — meaning the choice between taxable, exempt, and zero-rated status directly affects net profitability. A business supplying only exempt services cannot register for VAT and absorbs its input VAT costs entirely.

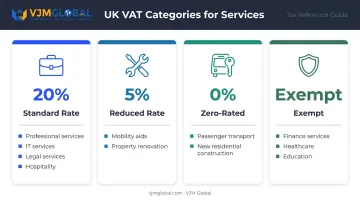

UK VAT Rates Applied to Services: A Category Breakdown

According to GOV.UK's VAT rates guidance, the UK operates three positive rates alongside an exempt category. The rate that applies depends entirely on the nature of the service — not simply on whether you're supplying a product or a service.

Standard Rate (20%)

The 20% rate has applied since 4 January 2011 and covers the majority of services. Common examples include:

- Professional consulting and accountancy

- Legal services to consumers

- Hairdressing and beauty treatments

- Hotel accommodation and restaurant meals

- Telecommunications and pay TV subscriptions

- Software development and IT services

If a service doesn't fall within a reduced, zero-rated, or exempt category, standard rate applies by default.

Reduced Rate (5%)

The 5% reduced rate applies to a narrow set of services. Applicable categories include:

- Installation of mobility aids for people aged 60 or over

- Certain residential property renovation work (including premises empty for at least two years)

- Some relevant residential and charitable building conversions

Important correction on energy-saving materials: Installations of energy-saving materials in residential properties are currently zero-rated until 31 March 2027, reverting to 5% from 1 April 2027 under VAT Notice 708/6.

Zero-Rated Services (0%)

Zero-rated services are still taxable supplies: the rate is 0%, but businesses remain VAT-registered and can reclaim input VAT on related costs. Key service categories include:

- International passenger transport (vehicles carrying 10+ passengers)

- Construction and first sale of new qualifying residential dwellings

- Certain services for disabled people (installation, repair, or adaptation of qualifying goods where conditions are met)

Exempt Services

Exempt services sit outside the VAT system entirely. The primary categories under Schedule 9 of the Value Added Tax Act 1994 include:

- Financial services (loans, deposits, share transactions)

- Insurance and related services

- Education and vocational training (by eligible bodies)

- Healthcare (registered doctors, dentists, opticians)

- Burial and cremation

- Membership subscriptions to trade unions and professional bodies

- Sports and physical education activities

- Gambling, betting, and lotteries

Unlike zero-rated supplies, businesses supplying only exempt services cannot register for VAT and cannot recover input VAT on their business purchases.

Outside the Scope of UK VAT

A fifth category often confused with exempt covers supplies that fall entirely outside UK VAT legislation. Common examples include:

- Services supplied outside the UK (where the place of supply rules take the transaction out of UK VAT)

- Statutory fees charged at the prescribed maximum (such as MOT testing fees)

- Supplies made by businesses below the VAT registration threshold

"Outside the scope" is meaningfully different from exempt. Businesses making only outside-the-scope supplies are not affected by the partial exemption rules and face no restriction on VAT registration eligibility — two consequences that do apply to exempt suppliers.

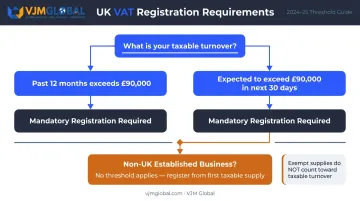

VAT Registration Requirements for UK Service Businesses

Mandatory Registration Threshold

As confirmed by HMRC, the mandatory registration threshold increased from £85,000 to £90,000 on 1 April 2024. Registration is required when:

- Taxable turnover for the past 12 months exceeds £90,000, or

- Taxable turnover is expected to exceed £90,000 in the next 30 days

Taxable turnover includes: standard-rated, reduced-rate, and zero-rated supplies Taxable turnover excludes: exempt supplies

This exclusion matters for mixed-supply businesses. A business earning £80,000 from exempt financial services and £20,000 from standard-rated consulting has taxable turnover of only £20,000 — well below the threshold.

Voluntary Registration

A service business below £90,000 may choose to register voluntarily. This makes sense when:

- Significant input VAT is incurred on business purchases (and can be reclaimed)

- Clients are mainly VAT-registered businesses who can recover the VAT you charge

- Future turnover is likely to exceed the threshold soon

The trade-off: administrative burden increases, and you must charge VAT to any end consumers who cannot recover it, which can make your pricing less competitive.

Non-UK Established Businesses

This is where the rules change substantially. Foreign businesses supplying services into the UK face no registration threshold — they must register for UK VAT from their very first taxable supply, as confirmed by VAT Notice 700/1.

This catches many Indian, US, and Australian businesses off guard when they begin supplying consulting, professional, or digital services to UK clients. If that applies to you, VJM Global can help you work through the registration process and ongoing compliance requirements — reach out at info@vjmglobal.com.

Making Tax Digital (MTD)

All VAT-registered businesses must file VAT returns through HMRC-compatible MTD software. Returns are typically submitted quarterly, with payment due one calendar month and seven days after the end of each accounting period. Non-compliance with MTD carries financial penalties.

Place of Supply Rules: Who Pays VAT and Where

"Place of supply" determines which country's VAT rules apply to a service transaction. Because services don't transfer a physical object, the rules rely on the nature of the transaction and where each party is established — not where the work physically occurs.

General B2B Rule

When a UK business supplies services to a business customer in another country, the place of supply is where the customer is located. UK VAT does not apply; the overseas customer accounts for VAT in their own jurisdiction — typically via a reverse charge mechanism.

Example: A UK marketing agency supplying campaign strategy services to a German manufacturer does not charge UK VAT. The German business accounts for German VAT under the reverse charge.

General B2C Rule

When a UK business supplies services to a non-business consumer, the place of supply is where the supplier is located — meaning UK VAT applies at the standard rate (unless the service is exempt or zero-rated).

Example: A UK tax consultant advising a private individual living in Australia must still charge UK VAT at 20% on those services.

Key Exceptions to the General Rules

Several service categories have their own place-of-supply rules under VAT Notice 741A:

| Service Type | Place of Supply |

|---|---|

| Land-related services | Where the land is situated |

| Restaurant and catering | Where physically performed |

| Passenger transport | Where the journey takes place |

| Digital services to EU consumers (B2C) | Where the consumer is located |

Post-Brexit Cross-Border Implications

The exceptions above become especially relevant in cross-border contexts. Since leaving the EU VAT area, the UK now operates its own separate framework — creating distinct obligations on both sides of UK–EU transactions:

- UK businesses supplying EU clients: Must assess whether VAT registration is required in specific EU member states — particularly for digital services supplied to EU consumers

- EU businesses supplying into the UK: May need UK VAT registration depending on the nature and volume of supplies

HMRC's guidance on VAT on services from abroad is the primary reference for foreign businesses assessing their UK obligations.

VAT Exemptions and Zero-Rated Services: Why the Distinction Matters

The difference between zero-rated and exempt is one of the most commercially significant distinctions in UK VAT — and one that service businesses frequently misunderstand.

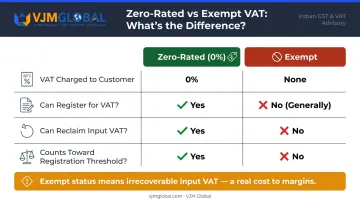

Zero-Rated vs. Exempt: A Direct Comparison

| Zero-Rated | Exempt | |

|---|---|---|

| VAT charged to customer | 0% | None |

| Can register for VAT? | Yes | Generally no |

| Can reclaim input VAT? | Yes | No |

| Counts toward registration threshold? | Yes | No |

Zero-rated keeps you inside the VAT system at a nil rate. Exempt removes you from it entirely — and that removal has a cost.

The Input VAT Cash Flow Problem

A business supplying only exempt services — say, a small private healthcare provider or independent financial adviser — cannot register for VAT. Every pound of VAT paid on expenses becomes an irrecoverable cost, including:

- Office rent

- Software subscriptions

- Professional indemnity insurance

- Marketing and advertising

For a business spending £50,000 annually on VAT-bearing expenses, that's £10,000 in unrecoverable VAT at 20% — absorbed directly into pricing or margins.

The situation becomes more nuanced for businesses that aren't entirely exempt. Partly exempt businesses — those with a mix of taxable and exempt supplies — must calculate recoverable input tax under partial exemption rules set out in VAT Notice 706. The standard method uses a turnover-based percentage, but HMRC may agree a special method where that produces a fairer result. Either way, getting the calculation wrong can trigger assessments and penalties.

VAT Accounting Schemes for Service-Based Businesses

Three HMRC-approved schemes can simplify VAT accounting for eligible service businesses. Each suits a different business profile.

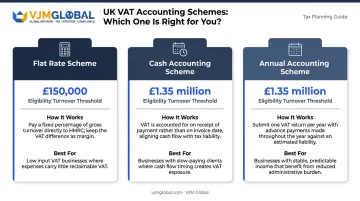

Flat Rate Scheme

- Eligibility: Taxable turnover of £150,000 or less (excluding VAT)

- How it works: Pay a fixed percentage of gross (VAT-inclusive) turnover to HMRC, rather than calculating VAT on each transaction

- Best for: Businesses with low input VAT costs

Common flat-rate percentages for service sectors (from HMRC's flat-rate table):

| Service Category | Flat Rate % |

|---|---|

| Accountancy or bookkeeping | 14.5% |

| Management consultancy | 14% |

| Computer/IT consultancy | 14.5% |

| Legal services | 14.5% |

| Hairdressing/beauty | 13% |

The scheme is simple but not always beneficial. If your input VAT costs are substantial, standard VAT accounting will typically return more.

Cash Accounting Scheme

- Eligibility: Expected taxable supplies of £1.35 million or less in the next year

- How it works: VAT is accounted for when payment is actually received, not when invoices are issued

- Best for: Service businesses on 30-60-90 day payment terms, or those with slow-paying clients

Without this scheme, you must pay VAT to HMRC on issued invoices — even if the client hasn't paid yet. Cash accounting eliminates that cash flow exposure.

Annual Accounting Scheme

- Eligibility: Expected taxable supplies of £1.35 million or less

- How it works: One VAT return per year, with advance payments made either as nine monthly or three quarterly instalments based on estimated liability

- Best for: Service businesses with stable, predictable income who want to reduce administrative workload

The scheme reduces quarterly filing obligations to a single annual return. That said, advance payments are based on estimated liability — so plan those figures carefully to avoid a large year-end correction.

These three schemes aren't mutually exclusive in all cases: for example, you can combine the Cash Accounting Scheme with standard VAT accounting. The right choice depends on your payment terms, input VAT exposure, and appetite for administrative work. If you're unsure which applies, the next section covers how to register and file under each.

Frequently Asked Questions

Is VAT always 20% in the UK?

No. 20% is the standard rate that applies to most services, but the reduced rate (5%) applies to specific categories such as mobility aids installation, and the zero rate (0%) applies to others including international passenger transport. Some services — financial, healthcare, education — are exempt entirely.

Is there VAT or GST in the UK?

The UK uses VAT (Value Added Tax), not GST. While both are consumption taxes, the UK retained its VAT system after Brexit and does not use the GST terminology common in Australia, India, or Canada.

What services are exempt from VAT in the UK?

The main exempt categories include financial services, insurance, education and vocational training, healthcare, burial and cremation, membership subscriptions, sports activities, and gambling. Businesses that supply only exempt services generally cannot register for VAT or recover input VAT on their costs.

Do UK businesses need to charge VAT on services provided to overseas clients?

It depends on whether the client is a business or consumer. B2B services to overseas businesses are typically outside the scope of UK VAT, with the overseas customer accounting for VAT locally. B2C services to individual consumers abroad usually attract UK VAT at the standard rate.

What is the VAT registration threshold for UK service businesses in 2024?

The mandatory threshold is £90,000 in taxable turnover over any rolling 12-month period, effective from 1 April 2024. Non-UK established businesses have no threshold — they must register from their very first taxable supply in the UK.

What is the reverse charge mechanism for services?

The reverse charge shifts responsibility to account for VAT from the supplier to the customer. In cross-border B2B transactions, this means the UK customer accounts for VAT rather than the overseas supplier charging it. It also applies domestically in certain sectors — notably construction services under the domestic reverse charge.