That single fact creates real confusion for two distinct groups. First, US businesses expanding internationally who suddenly encounter VAT registration requirements in the UK, EU, or Australia. Second, foreign companies from VAT-operating countries entering the US market, expecting a familiar national tax framework and finding a patchwork of state and local rules instead.

This article explains what VAT is, why the US chose a different path, how US sales tax compares, and the five key differences that matter most for cross-border compliance.

Key Takeaways

- The US has no federal VAT; sales tax is administered by individual states and local jurisdictions

- VAT is collected at every stage of the supply chain; US sales tax applies only at the final sale

- More than 170 countries operate a VAT or GST system (OECD)

- The US has more than 12,000 state and local taxing jurisdictions, each with its own rates and rules

- Post-Wayfair economic nexus rules allow foreign sellers to trigger US sales tax obligations with no physical presence required

What Is VAT and How Does It Work?

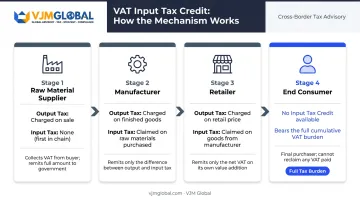

VAT is a consumption tax applied to the value added at each stage of production and distribution — manufacturer, wholesaler, retailer, and finally the end consumer. Businesses act as collection intermediaries on behalf of the government, not the ultimate bearers of the tax.

The Input Tax Credit Mechanism

This is the defining feature of VAT. Here's how it works in practice:

- A manufacturer buys raw materials and pays VAT on that purchase (input tax)

- The manufacturer sells finished goods, charges VAT on the sale (output tax), and remits only the difference to the tax authority

- This process repeats at each stage of the chain

- The full tax burden lands on the end consumer, not any intermediate business

The invoice-based structure creates a built-in audit trail. Every transaction generates a record — which is why the Tax Policy Center notes that VAT is administratively stronger than a retail sales tax. Cross-reporting between buyers and sellers makes evasion harder to sustain.

Global Context

VAT is not a niche system. According to the OECD, over 170 countries operate a VAT or GST, and the IMF reported in 2022 that VAT raises, on average, over 30% of total tax revenue in countries that impose it.

Rates vary by region:

| Region | Standard VAT Rate Range |

|---|---|

| EU member states (2024) | 17% (Luxembourg) to 27% (Hungary) |

| OECD average (2024) | 19.3% |

| EU legal minimum | 15% |

For any US business selling into these markets, VAT registration, invoicing requirements, and periodic filings are mandatory compliance obligations.

Why the US Does Not Have a National VAT

The absence of a federal VAT is not an oversight. It reflects the structural and political reality of how the US government is organized.

The Federalist Structure

The US Constitution grants substantial taxation authority to individual states. There is no single federal body imposing a broad consumption tax, which makes the centralization required for a VAT system politically difficult and administratively demanding. A federal VAT would not replace state sales taxes — it would layer on top of them, creating a stacked system that states would resist.

The 12,000-Jurisdiction Problem

The existing US sales tax landscape makes harmonization exceptionally difficult. According to Avalara, there are more than 12,000 US sales and use tax jurisdictions — states, counties, cities, and special districts — each with its own rates, definitions, and exemptions. Achieving nationwide uniformity would require unprecedented coordination across all levels of government.

Political Resistance

VAT has faced bipartisan resistance for decades. The two camps oppose it for opposite reasons:

- Conservative critics view it as a "hidden tax" that expands government revenue without visible accountability to voters

- Progressive critics worry it would raise consumer prices, disproportionately affecting lower-income households

Neither side has found sufficient political traction to advance a federal VAT bill.

The Puerto Rico Exception

Puerto Rico enacted Act 72-2015, creating the Impuesto al Valor Añadido (IVA), a VAT system prepared for rollout on April 1, 2016. It was repealed later that year after a short window.

Despite the repeal, Puerto Rico remains a notable case study — the only US jurisdiction to formally introduce and attempt a VAT system, demonstrating both the feasibility and the complications of such a transition within US territory.

US Sales Tax: The American Equivalent of VAT

US sales tax is a single-stage consumption tax applied only at the final point of sale between a retailer and the end consumer. It is not collected throughout the supply chain.

The core mechanics:

- Businesses purchasing goods for resale avoid the tax entirely by providing resale exemption certificates to their suppliers

- Tax is collected once, at checkout, and remitted to the relevant state or local authority

- The buyer sees the tax added to the price at the point of purchase

State-by-State Fragmentation

According to the Tax Foundation's 2024 data, 45 states plus Washington D.C. collect statewide sales taxes. The five exceptions are Alaska, Delaware, Montana, New Hampshire, and Oregon — but this doesn't mean those states are entirely tax-free. Alaska, for example, allows localities to impose their own local sales taxes, so sellers cannot assume zero obligation there.

Local sales taxes exist in 38 states, adding another layer of complexity for businesses selling across jurisdictions.

Use Tax: A Compliance Trap

Use tax has no equivalent in VAT systems and catches many businesses off-guard. When a buyer does not pay sales tax at the point of purchase — for example, buying from an out-of-state seller who doesn't collect it — they may be personally liable for self-reporting and remitting "use tax" to their home state. This obligation applies to businesses, not just consumers, and is frequently missed during compliance reviews.

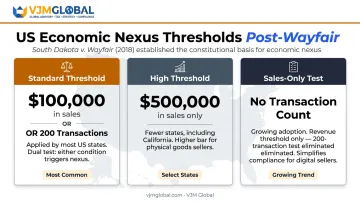

Economic Nexus After Wayfair

Before 2018, a business generally needed a physical presence in a state to owe sales tax there. The Supreme Court's South Dakota v. Wayfair decision changed that. Now, sufficient economic activity in a state can create nexus even without a warehouse, office, or employee.

South Dakota's threshold (the model most states followed) applies to sellers with more than $100,000 in sales or 200 transactions into the state. But thresholds vary considerably across jurisdictions:

- Some states set the bar at $500,000 in sales

- Others use combined sales-and-transaction tests

- A few have eliminated the transaction count entirely

Avalara documents active thresholds showing the full range of current state rules. Assuming every state uses the same trigger is a compliance risk.

VAT vs. US Sales Tax: 5 Key Differences Businesses Must Know

1. Collection Point

VAT is collected at every stage of the supply chain. US sales tax is collected once — at the final consumer sale. For businesses with multi-tier supply chains or import operations, this distinction determines where tax liability sits and whether any recovery mechanism applies.

2. Rate Structure

VAT systems typically maintain a single national standard rate, with limited reduced rates for specific categories. The US has thousands of independently set jurisdictional rates that can vary by street address within the same ZIP code. Rate changes across US jurisdictions occur continuously — Avalara tracked rate changes taking effect across more than a dozen states in April 2024 alone.

3. Tax Recovery

VAT-registered businesses reclaim input tax on qualifying business purchases through their periodic VAT return. No equivalent recovery exists under US sales tax. Instead, businesses use resale exemption certificates to avoid paying sales tax on goods intended for resale — a different mechanism with its own documentation requirements and audit risk.

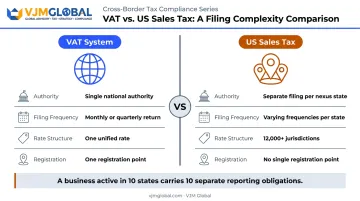

4. Reporting and Filing

VAT returns are filed monthly or quarterly with a single national authority. US sales tax requires separate filings with each state where a business has nexus, sometimes with different filing frequencies assigned by each state. State-specific examples illustrate how fast this adds up:

- California's CDTFA assigns cadences from quarterly prepay to annual, based on sales volume

- Texas monthly filers must submit returns by the 20th of the following month

- A business active in ten states carries ten separate reporting obligations, each with its own deadlines

5. Cross-Border Implications

For UK, EU, or Australian companies entering the US, the shift from a centralized VAT framework to a state-by-state sales tax system requires a completely different compliance strategy. Unlike VAT, there is no single registration point, no universal rate, and no input tax credit to recover costs across the supply chain.

That complexity is where many international businesses get caught out. VJM Global's team of CPAs and US-compliant tax professionals works with companies on this transition — covering nexus analysis across all 50 states, multi-state registration, and ongoing filing obligations as they expand into the US market.

Could the US Ever Adopt a Federal VAT?

The conversation resurfaces periodically. In 2024, the Congressional Budget Office published a policy option titled "Impose a 5 Percent Value-Added Tax" — framed explicitly as a budget option, not active legislation.

The CBO outlined two alternatives:

- Broad-base option: A 5% VAT applied to most goods and services

- Narrow-base option: A 5% VAT excluding categories such as food, education, housing, and medical care

Both alternatives were modeled with a hypothetical effective date of January 1, 2026, purely for revenue estimation purposes.

The theoretical case for a federal VAT includes:

- A broader and more stable revenue base than the current patchwork

- An invoice-based audit trail that improves compliance

- Potential simplification relative to managing 12,000+ jurisdictions

That theoretical case runs into significant practical resistance. State governments are unlikely to surrender tax authority. Implementation costs would be substantial. And layering a federal VAT onto existing state sales taxes — rather than replacing them — would create a more complex system, not a simpler one. Most economists and policy observers consider full US adoption unlikely in the near term.

For businesses with US operations — particularly foreign companies navigating American tax exposure — this matters mostly as a long-term watch item. The current state-led sales tax system remains the operational reality, and compliance today means mastering that 12,000+ jurisdiction patchwork, not preparing for a VAT that may never arrive.

Frequently Asked Questions

Does the USA have a VAT or GST?

No. The US has no federal VAT or GST. Sales taxes administered by individual states and local governments serve a similar revenue function, but they operate on a completely different mechanism and structure.

Is VAT included in prices in the USA?

No. Because the US uses sales tax rather than VAT, tax is typically added at the checkout rather than included in the listed price. Rates vary across thousands of jurisdictions, making pre-inclusion impractical for most retailers.

What tax does the US use instead of VAT?

The US uses a state-administered sales and use tax system, collected only at the final point of sale. Rates and rules vary by state, county, and city. There is no federal equivalent.

What is the main difference between VAT and US sales tax?

VAT is collected incrementally at every stage of the supply chain through an input tax credit mechanism. US sales tax is a one-time charge at the point of final consumer purchase, with no equivalent recovery mechanism for businesses.

Could the US ever adopt a VAT system?

The idea resurfaces periodically in policy discussions, including a 2024 CBO analysis of a hypothetical 5% federal VAT. Political, structural, and administrative barriers make near-term adoption unlikely.

Do international businesses need to understand VAT when operating in or from the US?

Yes, in both directions. US businesses exporting internationally will encounter VAT obligations in over 170 countries. Foreign companies selling into the US must understand sales tax nexus rules, which differ significantly from VAT frameworks and vary state by state.