%20(3).jpg)

Many Singapore businesses assume their existing audited accounts satisfy Dubai's requirements. They don't. An annual financial audit in Dubai is an independent, IFRS-compliant review conducted by a UAE-licensed auditor — and Dubai's regulatory framework, governed by the UAE Commercial Companies Law, Corporate Tax Law, and free zone mandates, creates obligations that differ fundamentally from Singapore's ACRA-based system.

Singapore companies filing under SFRS or SFRS(I) cannot transfer those reports to satisfy UAE authorities. Dubai requires statements audited by UAE-registered professionals — regardless of whether your Singapore audit is current or fully compliant at home.

This guide covers who must conduct a Dubai audit, what the process entails, how to prepare your books for UAE review, and the misconceptions that most commonly cause compliance failures.

A financial audit in Dubai is an independent examination of a company's income statements, balance sheets, cash flow statements, and accounting records. Its purpose is to confirm that these documents present a "true and fair view" of financial health under IFRS and UAE-specific regulations.

Who must conduct one:

Singapore businesses operating in Dubai frequently encounter multiple audit obligations at once — and confuse them. Here's how they differ:

Audit types clarified:

Audit TypeInitiated ByPurposeStatutory/Annual Financial AuditCompany (mandatory)Independent verification of financial statements for regulatory compliance under ISAFTA VAT AuditFederal Tax AuthorityVerify VAT compliance, invoices, input claimsFTA Corporate Tax AuditFederal Tax AuthorityVerify CT calculations, returns, transfer pricingInternal AuditCompany (voluntary)Assess internal controls, risk management

The statutory audit and FTA tax audits are entirely separate obligations. Preparing for one does not satisfy the other, and both can apply to your business at the same time.

Non-compliance carries concrete, escalating consequences under Cabinet Decision No. 75 of 2023:

Free zone non-compliance leads to license suspension, blacklisting, and inability to renew. DMCC, JAFZA, and DAFZA enforce audit submission deadlines strictly. Missing the deadline blocks your license renewal regardless of profitability.

The frameworks are not interchangeable:

You cannot substitute a Singapore audit for a UAE audit. The regulatory authority (Ministry of Economy for mainland, individual free zone bodies for DMCC/JAFZA/DIFC) will reject Singapore-prepared reports.

Since the UAE introduced a 9% corporate tax in June 2023, businesses must maintain verifiable, audited financial records for tax computation and FTA filing.

Key thresholds:

UAE banks require audited financial statements for credit facilities:

Free zone authorities like DMCC and JAFZA make audited financials a prerequisite for license renewal. Investors and joint venture partners demand audited accounts before committing capital. Without audit-ready books, you forfeit access to partnerships, government contracts, and external funding.

The type of audit opinion matters as much as having one. A clean (unqualified) opinion confirms your financials are free from material misstatement — the baseline UAE partners and government procurement offices expect. A qualified or adverse opinion, by contrast, signals unresolved accounting issues and will prompt investors and lenders to require explanations before proceeding.

For Singapore businesses entering the UAE, audit quality also affects your standing with the FTA. Audited statements that contradict your tax filings — even inadvertently — can trigger a compliance review. Getting the audit right the first time is the cleaner, lower-risk path.

The process moves from engagement and planning through risk assessment, evidence gathering, testing and verification, to the issuance of an audit report—typically lasting 2–6 weeks depending on company size and records readiness.

The auditor begins by understanding your business model, industry, and financial structure. They identify areas of elevated audit risk:

The auditor designs the audit approach based on risk areas, materiality thresholds, and regulatory requirements specific to your jurisdiction (mainland vs. free zone).

With the risk profile established, the auditor moves into document collection and testing. Core financial records reviewed include:

Supporting compliance documents typically requested:

Having these documents organized in advance significantly shortens audit duration and reduces costs. Businesses with year-round cloud-based bookkeeping (Zoho, QuickBooks) complete audits faster and cheaper than those scrambling to compile records post-year-end.

The auditor issues an audit report expressing an opinion on whether the financial statements present a true and fair view:

Opinion TypeMeaningUnqualified (Clean)Statements present a true and fair view in all material respectsQualifiedFairly presented except for specific identified mattersAdverseStatements do NOT present a true and fair viewDisclaimerAuditor unable to form an opinion due to scope limitations

Management receives a management letter with findings and internal control improvement recommendations. The company submits the final report to the relevant free zone authority or regulatory body within the specified deadline—typically 3–6 months from financial year-end depending on jurisdiction.

Singapore businesses using SFRS at home must ensure their Dubai entity's books are maintained under IFRS from day one. Three standards commonly cause reconciliation issues for Singapore businesses:

Revenue recognition (IFRS 15) focuses on transfer of control rather than risks and rewards. Dubai auditors scrutinize contract terms to determine performance obligations — Singapore private companies under SFRS may recognize revenue at a different point in time.

Lease accounting (IFRS 16) requires lessees to capitalize almost all leases as right-of-use assets with corresponding liabilities. Operating leases that stay off-balance-sheet under SFRS must appear on the books for Dubai entities.

Financial instruments (IFRS 9) applies a forward-looking expected credit loss model for impairment. SFRS provisioning methods differ, so reconciliation is typically needed for accounts receivable provisions and investment classifications.

Action step: Engage an IFRS-compliant bookkeeping partner from day one of Dubai operations. Retrofitting SFRS books to IFRS post-year-end is expensive and error-prone.

Treat document readiness as a year-round discipline, not a year-end task:

Core financial documents:

Transactional evidence:

Regulatory filings:

Singapore businesses with parent-subsidiary or branch structures must document intercompany transactions clearly. UAE auditors and the FTA scrutinize:

Each of these transaction types must comply with the arm's length principle. The UAE follows OECD Transfer Pricing Guidelines under Articles 34–36 of the Corporate Tax Law, giving auditors and the FTA clear grounds to challenge pricing retrospectively.

Documentation requirements:

Maintain clear agreements and pricing justifications from the first transaction, regardless of whether you meet the formal documentation threshold.

With transfer pricing documentation in order, the next step is appointing a qualified auditor. Auditors must be registered with the UAE Ministry of Economy and/or approved by the relevant free zone authority.

Verification steps:

AuthorityHow to VerifyUAE Ministry of EconomyCheck MoE registered auditors listDMCCVerify against DMCC Approved Auditors ListJAFZAConfirm with JAFZA authority approved auditor listDIFCCheck DIFC Registered Auditors portal

Selection criteria:

VJM Global supports foreign businesses through IFRS reconciliation, pre-audit preparation, and coordination with UAE-licensed audit partners — covering the compliance gap between Singapore accounting practices and UAE requirements.

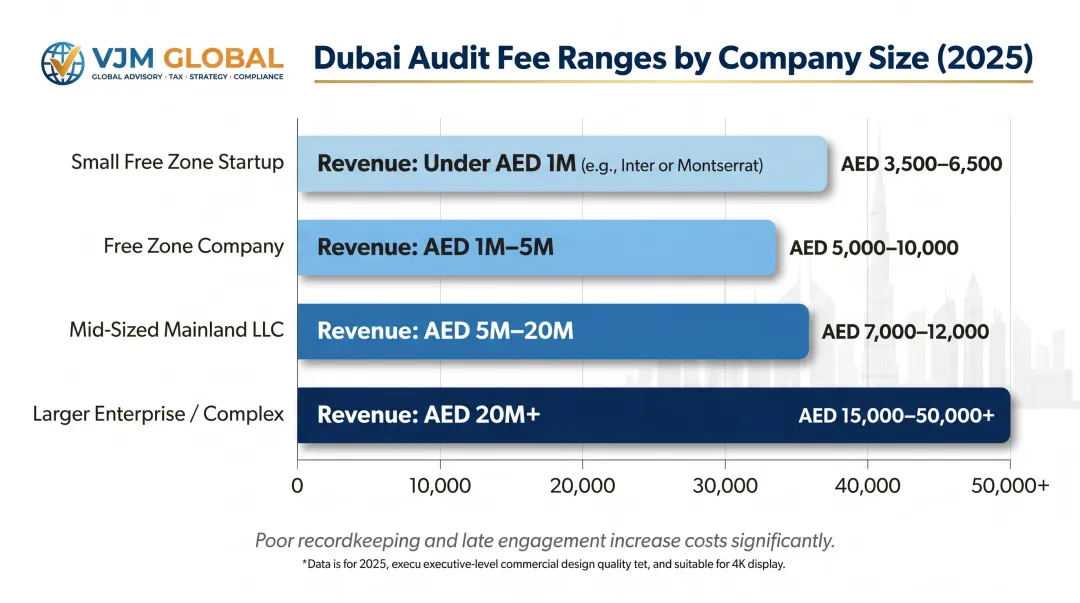

Indicative audit fee ranges by business size (2025 data):

Company ProfileRevenue RangeFee Range (AED)Small free zone startupUnder AED 1M3,500 – 6,500Free zone company (general)AED 1M – 5M5,000 – 10,000Mid-sized mainland LLCAED 5M – 20M7,000 – 12,000Larger enterprise/complexAED 20M+15,000 – 50,000+

Key cost drivers:

FALSE. UAE regulatory authorities—including the Ministry of Economy for mainland entities and individual free zone bodies (DMCC, JAFZA, DIFC, DAFZA)—require financial statements prepared under IFRS and audited by a UAE-registered auditor in accordance with ISA.

Singapore's Accounting Standards Council issues SFRS — not the IASB. Even SFRS(I), which is substantively identical to IFRS, cannot be presented as "IFRS-compliant" to UAE authorities. The regulatory framework demands IFRS as issued by the IASB, audited by a UAE-licensed professional.

Who will reject it: The Ministry of Economy (for mainland), DMCC, JAFZA, DAFZA, or DIFC (for free zones) will reject Singapore-prepared audit reports when you attempt to submit them for license renewal or regulatory filing.

FALSE. All major Dubai free zones mandate annual audited financial statements:

Additionally, all Qualifying Free Zone Persons must maintain audited financial statements under Ministerial Decision No. 84 of 2025 for corporate tax purposes, regardless of revenue. The "free zone = no audit" assumption is simply wrong — and it leads directly to license suspension.

FALSE. This confusion is understandable — both involve auditors and compliance — but the statutory audit and the FTA tax audit are independent obligations serving completely different purposes.

Here's how they differ:

Both obligations exist independently. Completing one does not satisfy the other — you can face FTA penalties even with a current statutory audit, and vice versa. Federal Decree-Law No. 32 of 2021 and free zone regulations treat them as separate requirements.

Audit fees range from AED 3,500–6,500 for small free zone startups to AED 15,000–50,000+ for larger enterprises with complex structures. Free zone and mainland companies may be priced differently. Poor recordkeeping, high transaction volumes, and late engagement significantly increase costs.

The annual audit is a legally required, IFRS-compliant independent examination of a company's financial statements by a UAE-registered auditor following ISA standards. It applies to most mainland and free zone companies under UAE Commercial Companies Law (Federal Decree-Law No. 32 of 2021) and individual free zone regulations.

It depends on legal structure and jurisdiction. Mainland LLCs and PJSCs are mandated under federal law, and most major free zones (DMCC, JAFZA, DAFZA, DIFC) require it for license renewal. The UAE Corporate Tax Law also mandates audits for businesses above AED 50 million in revenue, plus all tax groups and Qualifying Free Zone Persons regardless of revenue.

No. Singapore-audited accounts under SFRS or SFRS(I) do not satisfy UAE requirements — UAE authorities require IFRS-compliant statements audited by a UAE-licensed or free zone-approved auditor. Although SFRS(I) is substantively identical to IFRS, it is legally distinct and not recognized as meeting UAE compliance obligations.

Core documents typically requested include:

Most audits take 2–6 weeks depending on company size, transaction volume, and how well-organized the financial records are. Businesses that maintain year-round bookkeeping with cloud-based systems complete audits faster and at lower cost than those compiling records post-year-end.