La mayoría de las empresas de Singapur que entran en el mercado indio descubren, una vez que ya están allí, que sus conocimientos de las SFRS(I) son insuficientes. India opera bajo un sistema de doble estándar que abarca las normas contables locales (Indian GAAP), las Ind AS, el cumplimiento del GST y la supervisión del Instituto de Contadores Públicos de la India (ICAI), el Ministerio de Asuntos Corporativos (MCA) y la Autoridad Nacional de Información Financiera (NFRA). Subestimar esta complejidad conlleva brechas de cumplimiento, reexpresiones de estados financieros y sanciones que podrían haberse evitado.

Esta guía detalla los principios contables fundamentales de la India, los compara con el marco SFRS de Singapur y define qué normas se aplican a su entidad según su patrimonio neto y su estatus de cotización, desde los requisitos de auditoría legal hasta la documentación de precios de transferencia y las obligaciones de doble reporte.

Resumen:

India opera bajo un sistema contable de dos niveles diseñado para equilibrar la convergencia global con las necesidades regulatorias locales. Las empresas pequeñas y no cotizadas siguen las Indian GAAP (Normas Contables AS 1–32), mientras que las empresas grandes y todas las entidades cotizadas adoptan las Ind AS (Normas Contables Indias), que son convergentes con las NIIF, aunque no idénticas.

Para las empresas de Singapur que establecen filiales en la India, esta distinción es fundamental. El patrimonio neto y la estructura de propiedad de su entidad determinan qué marco se aplica, y la decisión es irreversible una vez tomada.

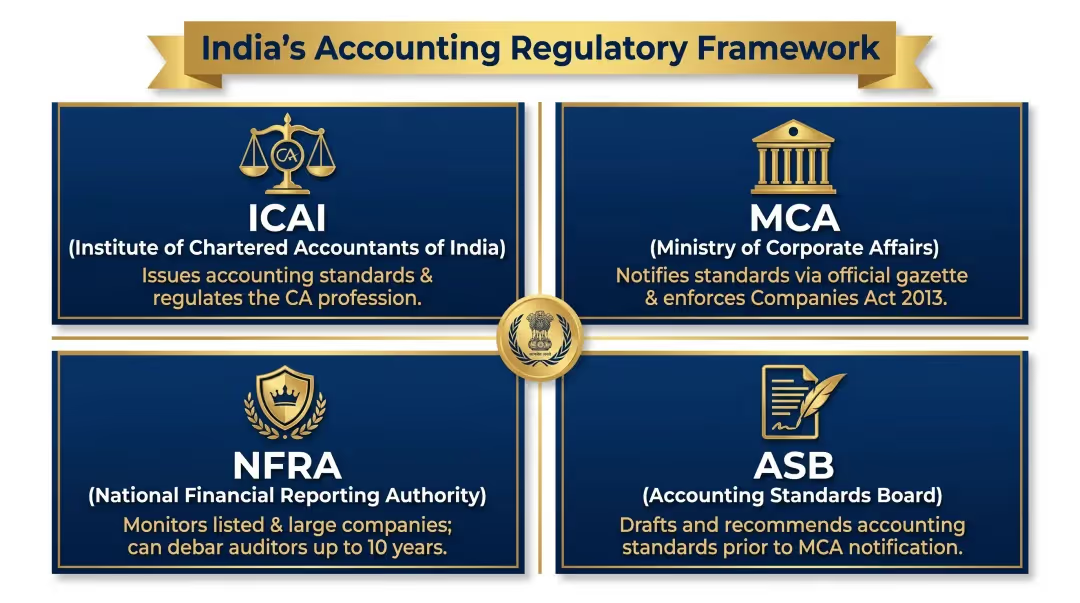

Cuatro instituciones principales definen el panorama contable de la India:

Si está estableciendo una filial india que cotiza en bolsa o una gran entidad no cotizada, espere supervisión de los cuatro organismos, no solo del ICAI.

Los PCGA de la India se refieren a las 27 Normas Contables vigentes (AS 1–32) emitidas por el ICAI y notificadas por el MCA bajo las Reglas de Sociedades (Normas Contables) de 2021. Estas se aplican a las empresas por debajo de los umbrales de las Ind AS.

Cinco normas no están vigentes:

Los PCGA de la India se basan en reglas, están arraigados en las prácticas comerciales nacionales y enfatizan la contabilidad a costo histórico. Son más sencillos que las Ind AS, pero carecen de las mediciones a valor razonable y la granularidad en la información que exigen los marcos convergentes con las NIIF.

Las Ind AS se introdujeron para alinear la contabilidad de la India con las normas internacionales, facilitando la consolidación de los estados financieros de las filiales indias en la empresa matriz de Singapur. Aunque están alineadas en gran medida con las NIIF, las Ind AS incluyen más de 10 excepciones específicas para la India que generan diferencias prácticas para las empresas matrices en Singapur al consolidar los resultados de sus filiales indias.

Principales excepciones de las Ind AS respecto a las NIIF:

Umbrales de aplicabilidad obligatoria:

Estos umbrales no cuentan toda la historia. Si su filial india es una sociedad holding, filial, empresa conjunta o asociada de una entidad ya sujeta a las Ind AS, también debe adoptar las Ind AS, independientemente de su propio patrimonio neto. Una vez adoptadas, está prohibido volver a las normas contables indias (Indian GAAP) según la Regla 4 de las Normas de Sociedades (Normas Contables Indias) de 2015.

Equivocarse en esta clasificación durante la constitución puede obligar a realizar costosas reexpresiones más adelante. VJM Global ayuda a las empresas de Singapur a identificar el marco correcto para su estructura empresarial específica antes de registrarse, no después.

Las normas contables de la India, tanto los PCGA indios como las Ind AS, se basan en principios que afectan directamente a la forma en que su filial india registra las transacciones y cumple con sus obligaciones normativas. Varios de estos principios interactúan con el sistema fiscal indio de formas que suelen tomar desprevenidas a las empresas de Singapur.

Los ingresos y gastos se registran cuando se devengan o incurren, no cuando se produce el movimiento de efectivo. La sección 128(1) de la Ley de Sociedades de 2013 exige que todas las empresas indias lleven sus libros bajo el principio de devengo mediante contabilidad por partida doble.

Por qué es importante en la India:

Los estados financieros asumen que el negocio continuará operando indefinidamente, lo cual afecta la valoración de activos y pasivos. La norma AS 1 codifica esto como una suposición fundamental bajo los PCGA indios; cualquier desviación requiere una divulgación explícita.

Para las empresas de Singapur que evalúan estrategias de salida o la reestructuración de sus operaciones en la India, esto es importante en la práctica: cualquier indicador de discontinuidad debe ser revelado y puede activar bases de medición de activos completamente diferentes.

Los gastos deben reconocerse en el mismo periodo que los ingresos que ayudaron a generar. Una asociación precisa también influye directamente en el calendario de pagos anticipados de impuestosde la India, donde los errores de estimación conllevan sanciones por intereses:

El reconocimiento inadecuado de los gastos puede provocar errores en la estimación de impuestos anticipados y sanciones por intereses.

Los contables reconocen las pérdidas probables de inmediato , pero solo registran las ganancias cuando se materializan. Esto evita sobreestimar la situación financiera.

Diferencia clave entre marcos normativos:

Toda información relevante que afecte la comprensión de las partes interesadas debe ser revelada. Esto es especialmente crítico para:

La norma SFRS(I) de Singapur es idéntica a las NIIF al 1 de enero de 2018. La norma Ind AS de India es convergido con las NIIF pero incluye exclusiones y requisitos locales que generan diferencias prácticas en la presentación de informes.

Ambos marcos siguen la misma base conceptual: contabilidad de devengo, imagen fiel, empresa en funcionamiento y materialidad. El reconocimiento de ingresos (SFRS(I) 15 / Ind AS 115), la contabilidad de arrendamientos (SFRS(I) 16 / Ind AS 116) y los instrumentos financieros (SFRS(I) 9 / Ind AS 109) están alineados a nivel de norma.

Pero: las exclusiones de la India implican que transacciones idénticas pueden arrojar cifras diferentes.

Ambos prohíben el método UEPS (últimas entradas, primeras salidas) y exigen el uso de PEPS o el coste promedio ponderado. Ambos valoran el inventario al menor valor entre el coste y el valor neto realizable (VNR), con la reversión obligatoria de las rebajas de valor cuando el VNR aumenta posteriormente.

Matiz específico de la India: La norma Ind AS 2 exige una revelación detallada de las reversiones de rebajas de valor de inventarios, y el ICAI ha emitido directrices específicas por sector (por ejemplo, construcción y farmacéutico) que los contables de Singapur podrían no encontrar bajo las SFRS(I).

Ambos siguen el modelo de cinco pasos bajo la NIIF 15. Sin embargo:

Más allá de las áreas de convergencia, existen tres requisitos de cumplimiento que se aplican exclusivamente en India, ninguno de los cuales tiene un equivalente directo en el marco de información financiera de Singapur.

Según las secciones 194 y 195 de la Ley del Impuesto sobre la Renta de 1961, los pagadores deben retener impuestos en la fuente sobre pagos específicos, incluidos todos los pagos a no residentes si están sujetos a impuestos en India. Esto genera:

Cada factura debe realizar un seguimiento del estado de retención del TDS, un requisito que no tiene paralelo en el sistema de GST de Singapur. Para las empresas de Singapur con filiales en India, el seguimiento del cumplimiento del TDS debe integrarse en los procesos de cuentas por pagar y por cobrar desde el primer día.

El GSTR-2B es un estado de cuenta mensual generado automáticamente (disponible el día 14 de cada mes) que muestra el ITC disponible según las declaraciones de los proveedores. No está permitido reclamar el ITC por facturas que no aparezcan en el GSTR-2B—lo que crea una obligación de información financiera exclusiva de la India.

En la práctica, esto significa que sus libros deben conciliarse mensualmente con las declaraciones GSTR-3B, identificando las transacciones no elegibles y calculando los intereses sobre cualquier reclamación en exceso. El servicio de conciliación de GST de VJM Global gestiona este proceso para sus clientes, reduciendo el riesgo de incumplimiento normativo.

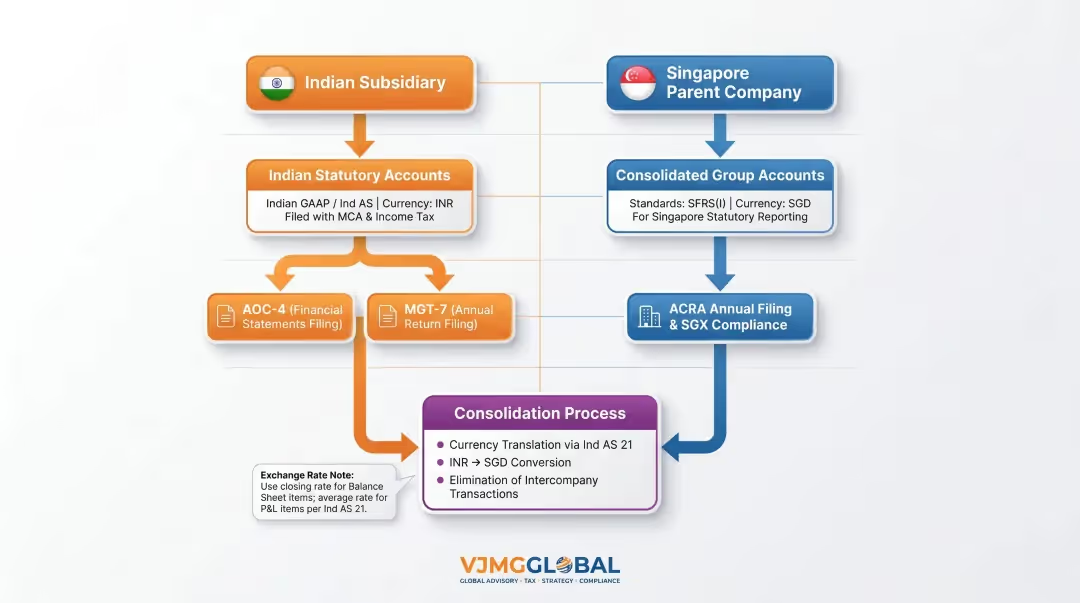

La sección 128(1) de la Ley de Sociedades de 2013 exige que toda empresa mantenga libros de contabilidad en la India, bajo el principio de devengo y utilizando el sistema de partida doble. Los libros deben llevarse en rupias indias, sin excepciones.

Las empresas matrices de Singapur acostumbradas a mantener registros consolidados en SGD deben asegurarse de que su filial india mantenga libros separados y conformes denominados en INR.

La aplicabilidad depende del tipo de entidad, el patrimonio neto y la estructura de propiedad — y equivocarse en esto durante la constitución crea brechas de cumplimiento que son costosas de corregir más adelante. Las empresas de Singapur suelen establecer uno de estos tres tipos de entidades en la India, cada una con una obligación contable diferente:

Si está estableciendo una filial de propiedad absoluta constituidas en la India, se aplican los siguientes umbrales:

Crítico: Una vez adoptadas las Ind AS (ya sea de forma obligatoria o voluntaria), no es posible volver a los PCGA de la India—incluso si el patrimonio neto cae posteriormente por debajo del umbral.

VJM Global trabaja con empresas extranjeras que entran en la India para identificar el marco contable correcto en el momento de la constitución y gestionar las transiciones cuando las filiales superan los umbrales de las Ind AS, antes de que aparezca una brecha de cumplimiento en el informe de un auditor.

La sección 128(1) exige que las empresas indias mantengan registros específicos:

Las empresas de Singapur, acostumbradas a prácticas contables flexibles para PYMES, a menudo subestiman la rigidez de los requisitos de los libros legales en la India. El incumplimiento puede derivar en sanciones y responsabilidad directa para los directores de la empresa.

Las obligaciones que se pasan por alto con mayor frecuencia incluyen:

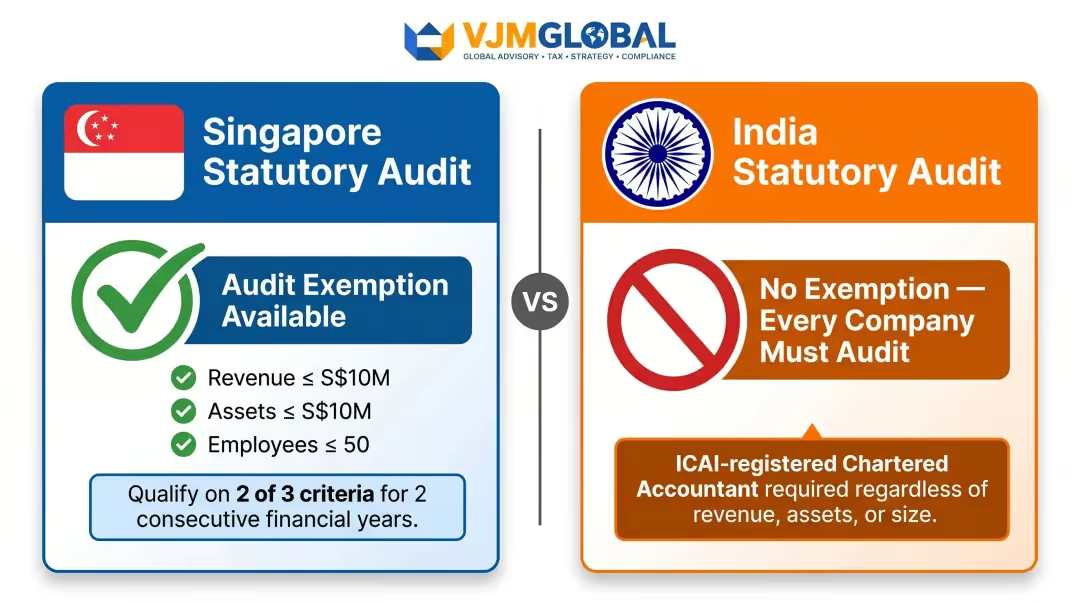

Según la Sección 139(1) de la Ley de Sociedades de 2013, toda empresa debe nombrar un auditor, independientemente de sus ingresos, activos o número de empleados. A las empresas de Singapur esto suele sorprenderles, ya que en la India no existe una exención equivalente para pequeñas empresas.

Exención de auditoría en Singapur (a modo de comparación):

Según la Sección 205C, una empresa privada de Singapur puede optar a la exención de auditoría si cumple 2 de los 3 criterios durante dos años consecutivos:

India no cuenta con una exención equivalente. Todas las empresas indias, incluidas las pequeñas filiales con ingresos mínimos, deben someterse a una auditoría legal realizada por un contador público colegiado registrado en el ICAI.

VJM Global coordina auditorías legales para empresas indias de propiedad extranjera, asegurando que se cumplan los requisitos de registro de los contadores públicos y que los cronogramas de auditoría se ajusten tanto a los plazos legales de la India como a los plazos de presentación de informes de la empresa matriz en Singapur.

Las transacciones entre una empresa matriz en Singapur y su filial india son transacciones internacionales entre partes vinculadas reguladas por las secciones 92 a 92F de la Ley del Impuesto sobre la Renta de 1961.

Requisitos de documentación (Regla 10D):

Sanciones según la sección 271AA:

La norma Ind AS 24 también exige la divulgación de todas las transacciones entre partes vinculadas en los estados financieros, incluyendo importes, saldos pendientes y condiciones.

VJM Global ayuda a las empresas matrices en Singapur con documentación de precios de transferencia contemporánea, estudios de evaluación comparativa y revelaciones bajo la norma Ind AS 24, permitiendo a los clientes demostrar que los precios entre empresas reflejan lo que acordarían partes independientes y evitar así la penalización del 2% sobre las transacciones.

Las empresas matrices en Singapur generalmente necesitan dos conjuntos de estados financieros:

La norma Ind AS 21 establece cómo convertir las transacciones y operaciones en moneda extranjera. Para las filiales en India:

Contexto del tipo de cambio: A fecha de mayo de 2026, el tipo de cambio medio de mercado SGD/INR es de aproximadamente ₹74.27 por SGD, con un promedio de 6 meses de alrededor de ₹71.25. La tasa osciló entre ₹67.75 (noviembre de 2025) y ₹74.60 (mayo de 2026). Esa diferencia representa una volatilidad significativa; planifique los ajustes de consolidación en consecuencia.

Utilice un software contable que admita:

Establezca cronogramas claros para el cierre de mes:

Plazos legales en la India:

Los plazos de consolidación de la empresa matriz en Singapur varían según la compañía, pero generalmente se alinean con los ciclos de informes trimestrales.

Gestionar ambos libros contables en dos jurisdicciones es donde muchos equipos financieros en Singapur enfrentan retrasos. VJM Global se encarga de los libros de la filial india (Ind AS/PCGA indios en INR) mientras su equipo en Singapur se enfoca en la consolidación del grupo bajo SFRS(I), manteniendo ambas contabilidades listas para auditoría y cumpliendo con los plazos.

La India utiliza dos conjuntos de normas: PCGA indios (27 Normas de Contabilidad operativas AS 1–32) para empresas más pequeñas y no cotizadas, y Ind AS (Normas de Contabilidad de la India convergentes con las NIIF) para empresas que cotizan en bolsa y entidades no cotizadas con un patrimonio neto ≥ 250 millones de rupias. Ambas están reguladas por el ICAI y el MCA, y la NFRA proporciona supervisión independiente para las entidades que cotizan en bolsa.

Los US GAAP se basan en reglas y fueron desarrollados por el FASB para el mercado estadounidense; los PCGA de la India se basan en principios y están moldeados por el entorno regulatorio de la India. Las divergencias clave incluyen los métodos de inventario (LIFO permitido bajo los US GAAP, prohibido en la India), los modelos de contabilidad de arrendamientos y los enfoques de deterioro de instrumentos financieros. La Ind AS 109 utiliza un modelo de pérdidas crediticias esperadas (ECL) de tres etapas, mientras que los US GAAP aplican las pérdidas esperadas durante toda la vida del activo de forma inmediata.

Los cinco principios más citados son devengo (registro cuando se gana o se incurre), empresa en funcionamiento (el negocio continúa indefinidamente), asociación (los gastos se reconocen con los ingresos relacionados), prudencia (reconocer las pérdidas inmediatamente y las ganancias cuando se realizan), y revelación suficiente (toda la información importante debe ser revelada). Las normas emitidas por el ICAI de la India incorporan los cinco como conceptos fundamentales.

Los siete principios básicos son entidad económica, unidad monetaria, periodo contable, costo histórico, revelación suficiente, empresa en marcha, y asociación. Las normas indias reconocen los siete; las Ind AS introducen excepciones de valor razonable al costo histórico para clases de activos específicas, como instrumentos financieros y propiedades de inversión.

Los 12 principios de los PCGA son regularidad, consistencia, sinceridad, permanencia de métodos, no compensación, prudencia, continuidad, periodicidad, importancia relativa, buena fe, reconocimiento, y revelación. Las Ind AS de la India incorporan todos estos principios y, además, los alinean con las NIIF, lo cual es fundamental para las empresas de Singapur que gestionan obligaciones de doble informe para sus filiales indias.

¿Está listo para llevar la contabilidad de su filial india correctamente desde el principio? Los contadores públicos registrados ante el ICAI y los especialistas transfronterizos de VJM Global apoyan a las empresas de Singapur en cada etapa, desde las evaluaciones de aplicabilidad de las Ind AS hasta la coordinación de auditorías legales y la elaboración de informes de gestión. Con más de 30 años de experiencia ayudando a empresas extranjeras a navegar el panorama contable de la India, aportamos experiencia práctica a cada proyecto. Contáctenos en info@vjmglobal.com o +91-9213397070 para hablar sobre sus necesidades de expansión en la India.