Las empresas de Singapur que se expanden a la India se encuentran con un entorno contable fundamentalmente distinto que puede tomar desprevenidos incluso a los equipos financieros más experimentados. A diferencia del marco de información más flexible de Singapur, el sistema de la India se basa en varios pilares diferenciados:

Los desafíos van más allá de la alineación de normas. La Ley de Sociedades de 2013 de la India prescribe el formato exacto que deben seguir los estados financieros (Anexo III) y establece vidas útiles específicas para la depreciación (Anexo II). Todas las empresas, independientemente de su tamaño, deben presentar cuentas auditadas ante el Registro de Sociedades dentro de plazos estrictos.

La estructura de cinco niveles del GST, las obligaciones de TDS en prácticamente todos los pagos entre empresas y los requisitos de documentación de precios de transferencia sin un umbral mínimo hacen que la carga de cumplimiento sea mayor que en la mayoría de los mercados de la ASEAN.

Esta guía cubre lo que las empresas de Singapur necesitan saber antes y después de su entrada:

Las Normas de Contabilidad de la India (Ind AS) son formuladas por el Consejo de Normas de Contabilidad (ASB) del Instituto de Contadores Públicos de la India (ICAI) y notificadas por el Ministerio de Asuntos Corporativos (MCA) de la India bajo las Reglas de Sociedades (Normas de Contabilidad de la India) de 2015. Estas normas están basadas en las NIIF y en gran medida convergen con ellas, aunque incluyen exclusiones y modificaciones específicas que reflejan las condiciones legales y económicas de la India.

La India seguía anteriormente los PCGA indios (IGAAP) antes de realizar la transición hacia la convergencia con las NIIF a través de las Ind AS. La adopción obligatoria comenzó el 1 de abril de 2016 para las grandes empresas, lo que mejoró significativamente la comparabilidad de los estados financieros indios para los inversores internacionales y las empresas matrices en Singapur que gestionan consolidaciones transfronterizas.

Tres organismos rigen la jerarquía normativa contable de la India:

Las empresas de Singapur deben seguir las actualizaciones de estos tres organismos para mantenerse al día.

La adopción de las Ind AS sigue un enfoque gradual basado en umbrales:

Las empresas que se encuentran por debajo de estos umbrales continúan bajo las Normas Contables (AS) anteriores. Este sistema de dos niveles es relevante cuando las empresas de Singapur estructuran su entidad en la India.

Una regla tiene un peso importante a largo plazo: una vez que una empresa adopta las Ind AS, ya sea de forma voluntaria u obligatoria, no puede volver a las normas anteriores, incluso si su patrimonio neto cae posteriormente por debajo del umbral. Esto hace que la decisión inicial sobre la estructura y el tamaño de la entidad sea significativa desde el principio. Si una empresa matriz de Singapur sigue las Ind AS, todas sus filiales indias también deben seguirlas, independientemente de su patrimonio neto individual.

El año financiero legal de la India va del 1 de abril al 31 de marzo según la Sección 2(41) de la Ley de Sociedades de 2013, a diferencia del año financiero flexible de Singapur o el enfoque común del año natural. Las empresas de Singapur gestionan eficazmente dos ciclos de información financiera distintos, lo que afecta a los plazos de presentación de informes consolidados, las conciliaciones entre empresas y la programación de auditorías. Las filiales de empresas matrices extranjeras pueden solicitar al Gobierno Central permiso para utilizar un año financiero alternativo para la consolidación, aunque la aprobación se concede caso por caso.

Tanto las Ind AS como las Normas de Información Financiera de Singapur (SFRS) convergen con las NIIF, lo que significa que sus fundamentos conceptuales son similares. Sin embargo, las Ind AS de la India contienen exclusiones específicas y la Ley de Sociedades de 2013 impone requisitos de presentación adicionales (formato del Anexo III) que no tienen un equivalente directo en el marco más flexible de Singapur.

Las divergencias clave incluyen:

.avif)

Más allá de la tabla anterior, cuatro áreas operativas merecen una atención más detallada:

Toda empresa constituida en la India, incluidas las filiales de empresas de Singapur, debe designar un auditor legal que sea un contador público colegiado (Chartered Accountant) en ejercicio o una firma de contadores registrada ante el ICAI conforme a la Sección 139 de la Ley de Sociedades de 2013. El Consejo de Administración debe nombrar al primer auditor dentro de los 30 días siguientes a la constitución.

Los estados financieros auditados deben ser aprobados en la Junta General Anual (AGM), que debe celebrarse dentro de los 6 meses siguientes al cierre del ejercicio fiscal (antes del 30 de septiembre para los ejercicios que cierran el 31 de marzo). Posteriormente, los estados deben presentarse ante el Registro de Sociedades; el incumplimiento de los plazos conlleva sanciones y puede afectar al estatus de "activa" de la empresa.

La Sección 128 de la Ley de Sociedades de 2013 exige que todos los registros contables se mantengan:

Las empresas de Singapur que dependen de plataformas financieras globales centralizadas deben asegurarse de que sus datos en la India cumplan con los requisitos locales de almacenamiento y denominación de moneda. El incumplimiento conlleva sanciones de entre 50 000 ₹ y 500 000 ₹ para el responsable.

Además de las cuentas auditadas, las empresas indias deben presentar:

El incumplimiento de estos plazos conlleva sanciones acumulativas: 10 000 ₹ iniciales más 100 ₹ por cada día de retraso, con un límite de 200 000 ₹ para la empresa y 50 000 ₹ por director. Los directores asumen responsabilidad personal y deben pagar las multas con fondos propios, no con los de la empresa.

.avif)

Las transacciones entre una empresa matriz en Singapur y su filial india se clasifican como transacciones internacionales y deben valorarse a precios de mercado. Bajo Sección 92E de la Ley del Impuesto sobre la Renta, las empresas deben:

Importante: No existe un umbral mínimo. Incluso una sola transacción internacional que califique activa la obligación de presentar el Formulario 3CEB, cuyo plazo vence el 31 de octubre del año fiscal correspondiente. Este es un requisito de cumplimiento que las empresas de Singapur con comisiones por servicios intragrupo, regalías o préstamos suelen pasar por alto.

El equipo de precios de transferencia de VJM Global ayuda a las empresas de Singapur a preparar la documentación del Formulario 3CEB y a determinar los precios de plena competencia en las transacciones intragrupo, antes de la fecha límite del 31 de octubre y no después de recibir una notificación.

El informe de los directores y los estados financieros auditados deben estar firmados por al menos dos directores, incluyendo a un director a tiempo completo cuando corresponda. Los directores con sede en Singapur de entidades indias asumen obligaciones de cumplimiento personal bajo la ley india, no solo las de la empresa. Los requisitos clave incluyen:

La India utiliza una estructura de impuestos corporativos diferenciada:

Una filial constituida en la India califica como empresa nacional elegible para la tasa del 25,17 % según la Sección 115BAA (introducida en 2019). Una empresa de Singapur que opera a través de una sucursal se enfrenta a una tasa de hasta el 43,68 %, aproximadamente 18 puntos porcentuales más. Para la mayoría de las empresas de Singapur, esta diferencia fiscal por sí sola hace que constituir una filial local sea la opción estructural más inteligente frente a una sucursal.

.avif)

Desde el 1 de julio de 2017, el GST sustituyó a los antiguos impuestos indirectos con una estructura de cinco niveles:

Los contribuyentes mensuales deben presentar el GSTR-1 (suministros salientes) antes del día 11 del mes siguiente y el GSTR-3B (declaración resumen) antes del 20.º. Los pequeños contribuyentes con una facturación de hasta 50 millones de rupias pueden optar por la presentación trimestral bajo el régimen QRMP.

El TDS es un mecanismo de retención que exige al pagador deducir el impuesto antes de realizar pagos por servicios, alquileres, honorarios profesionales y otros pagos especificados. Sección 195 se aplica a cualquier pago a un no residente sujeto a impuestos en la India, sin exención por umbral. Se aplican obligaciones mensuales de declaración de TDS.

India y Singapur tienen un Convenio para Evitar la Doble Imposición (CDI) que cubre dividendos, intereses, regalías, ganancias de capital y beneficios empresariales. Reducciones clave de la retención de impuestos bajo el tratado:

Para solicitar los beneficios del CDI, una entidad de Singapur debe proporcionar:

Sin un TRC válido, el pagador indio debe aplicar las tasas nacionales más altas. Las empresas extranjeras también necesitan un PAN indio antes de poder presentar el Formulario 10F electrónicamente.

Implicación contable: Los registros de la entidad india deben separar claramente los tipos de ingresos para que los ingresos elegibles según el tratado puedan identificarse con precisión durante la evaluación. Una contabilidad mal estructurada es una razón común por la que las empresas no logran aprovechar los beneficios del CDI, y el costo de ese descuido puede ser significativo.

VJM Global asesora a empresas de Singapur en reclamaciones de DTAA, desde los requisitos de TRC y el cumplimiento del Formulario 10F hasta la estructuración de registros contables para garantizar que los beneficios del tratado se aprovechen plenamente desde el primer día.

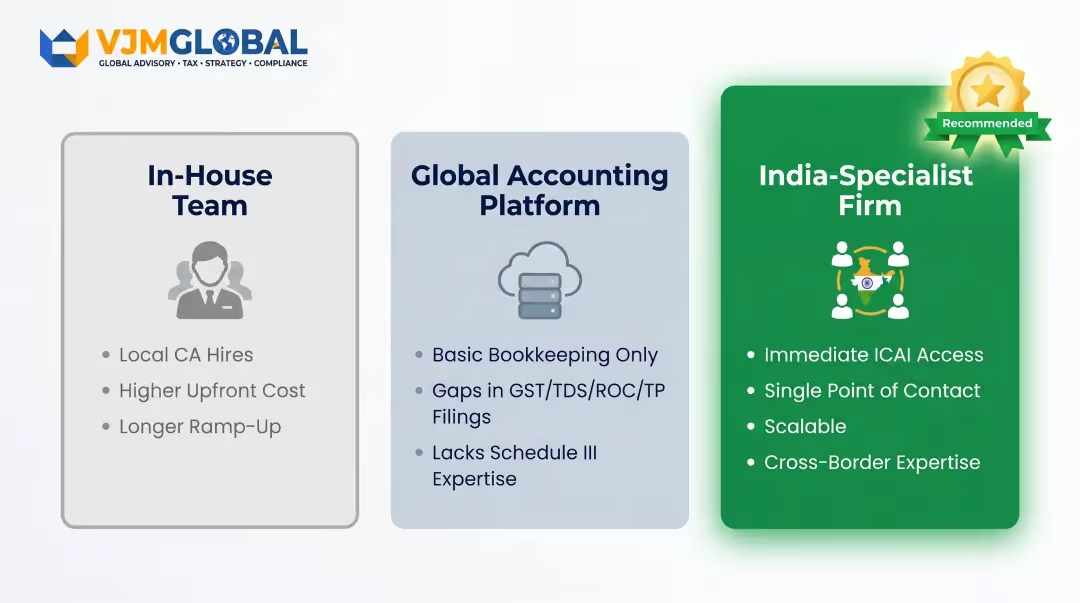

Las empresas de Singapur tienen tres opciones estructurales principales:

Ventajas prácticas de externalizar a una firma especializada en la India:

Para las empresas de Singapur que buscan este tipo de apoyo especializado, VJM Global —con más de 30 años de experiencia ayudando a empresas extranjeras a operar en la India— cubre todo el conjunto de cumplimiento: coordinación de auditorías legales, documentación de precios de transferencia (Formulario 3CEB), presentaciones ante el ROC (AOC-4 y MGT-7), registro de GST, declaraciones de TDS y asesoramiento sobre DTAA.

El equipo también ayuda a configurar los sistemas contables para cumplir con los requisitos del Anexo III y gestiona el ajustado calendario de declaraciones que va desde el cierre del ejercicio el 31 de marzo hasta la temporada de declaraciones de octubre y noviembre.

Antes de que su entidad india comience a operar, siga estos pasos:

Antes de comenzar las operaciones:

La India utiliza las Normas de Contabilidad Indias (Ind AS), que son normas convergentes con las NIIF, formuladas por el ICAI y notificadas por el Ministerio de Asuntos Corporativos. Las empresas utilizan un sistema de contabilidad de partida doble basado en el devengo, y los estados financieros deben prepararse en el formato del Anexo III prescrito por la Ley de Sociedades de 2013.

Las Ind AS están en gran medida convergentes con las NIIF, pero no son idénticas. La India ha introducido exclusiones específicas: contabilidad de coberturas (solo se permite la NIIF 9), propiedades de inversión (solo modelo de costo) y ganancias por compras ventajosas (registradas a través de ORI). Las empresas de Singapur familiarizadas con las NIIF no deben asumir una equivalencia total.

El año fiscal legal de la India va del 1 de abril al 31 de marzo según lo establecido por la Sección 2(41) de la Ley de Sociedades de 2013. Esto se aplica a todas las empresas registradas en la India, incluidas las filiales de empresas de Singapur, lo que genera ciclos de presentación de informes duales para las empresas matrices.

Sí, la India y Singapur tienen un CDI que reduce significativamente las tasas de retención de impuestos: dividendos al 10%, intereses al 15% (10% para pagos bancarios) y regalías/honorarios por servicios técnicos al 10%. Para reclamar los beneficios, las entidades de Singapur deben proporcionar un Certificado de Residencia Fiscal del IRAS y presentar el Formulario 10F electrónicamente en el portal fiscal de la India.

Sí. La Ley de Sociedades de 2013 exige que las auditorías legales sean realizadas por un contador público en ejercicio o una firma de contadores públicos registrada ante el ICAI; un auditor con licencia de Singapur no puede cumplir esta función. Ciertas presentaciones de cumplimiento, incluido el Informe del Contador sobre Precios de Transferencia (Formulario 3CEB), también requieren la certificación de un contador público.

No presentar el Formulario AOC-4 (estados financieros) o el Formulario MGT-7 (declaración anual) a tiempo conlleva una multa inicial de 10 000 ₹ más 100 ₹ por cada día de incumplimiento continuado, con un límite de 200 000 ₹ (2 lakh) para la empresa y 50 000 ₹ por director. Los directores deben pagar las multas con sus fondos personales, y el incumplimiento de la presentación debe subsanarse independientemente del pago.