%20(3).jpg)

Many small private companies operating in Singapore mistakenly believe that being small equals having no financial reporting requirements at all. This misconception leads to costly non-compliance with the Accounting and Corporate Regulatory Authority (ACRA), which can result in penalties ranging from S$300 to S$3,000 for late or non-filing.

Since 2015, Singapore's Companies Act has provided a clear pathway to audit exemption under Section 205C through the "small company" concept, which replaced the older "exempt private company" framework. The updated framework opens audit relief to a broader range of private companies—including those with corporate shareholders—while maintaining essential compliance obligations.

Under Section 205C of the Companies Act 1967, qualifying "small companies" are exempt from mandatory audits of their financial statements by an external auditor. This provision was introduced through the Companies (Amendment) Act 2014 and took effect for financial years beginning on or after 1 July 2015.

Key distinction: Audit exemption means you don't need an auditor—not that you have no financial obligations. Exempt companies must still:

These obligations remain in place regardless of audit status. Where the new framework does change things is in eligibility — the "small company" regime is considerably broader than its predecessor, the "exempt private company" (EPC) regime:

Old EPC Framework (pre-2015)New Small Company Framework (2015+)Revenue ≤ $5MRevenue ≤ $10MMaximum 20 membersNo member limitNo corporate shareholders allowedCorporate shareholders permittedNarrow eligibilityBroader eligibility across company types

Understanding which framework applies to your company is the first step — the next is confirming whether you meet the specific qualifying criteria.

Audit exemption eligibility depends on meeting two overarching conditions:

The Thirteenth Schedule of the Companies Act defines these thresholds:

CriterionMeasureThresholdA — RevenueTotal annual revenue≤ SGD 10 millionB — Total AssetsBalance sheet assets≤ SGD 10 millionC — EmployeesFull-time headcount at year-end≤ 50 employees

Contractors and part-time workers do not count toward the employee limit.

A company qualifies if it meets any two of the three criteria above for two consecutive preceding financial years.

Example:

Financial YearRevenueTotal AssetsEmployeesQualifies?FY2022$8M ✓$12M ✗35 ✓2 of 3 met ✓FY2023$9M ✓$11M ✗40 ✓2 of 3 met ✓Status for FY2024———Audit exempt ✓

In this scenario, the company exceeds the asset threshold in both years but stays under revenue and employee limits, so it qualifies for audit exemption starting FY2024.

New companies (less than two years old) have no two-year history to look back on. Instead, they qualify based on meeting 2 of the 3 criteria within the current financial year itself.

Example:

A company incorporated in March 2023 with its first financial year ending December 2023 can qualify for audit exemption for FY2023 if it meets the thresholds during that first year alone. Once the company completes its second financial year, the standard two-year lookback rule applies.

If your company is part of a corporate group—either as a parent or subsidiary—individual qualification is not enough. The entire group must also qualify as a "small group" on a consolidated basis.

A small group must meet 2 of the same 3 criteria (revenue, assets, employees) calculated on a consolidated basis for the immediate past two consecutive financial years, using:

"Group" follows Singapore accounting standards — regardless of whether consolidated financial statements are actually filed. A Singapore subsidiary must assess group membership under these definitions even if it never prepares consolidated accounts.

This rule directly affects foreign businesses. If a Singapore company is a subsidiary of a large overseas parent, the global group's size determines eligibility—not the local entity's financials alone.

Example:

A small Singapore subsidiary with revenue of S$3M and 10 employees is wholly owned by a UK parent company with revenue of £50M and 200 employees. Even though the Singapore entity easily meets all three criteria individually, it cannot claim audit exemption because the consolidated group fails the thresholds.

Foreign-owned entities should assess group size at the outset — waiting until audit time to discover ineligibility is a costly mistake.

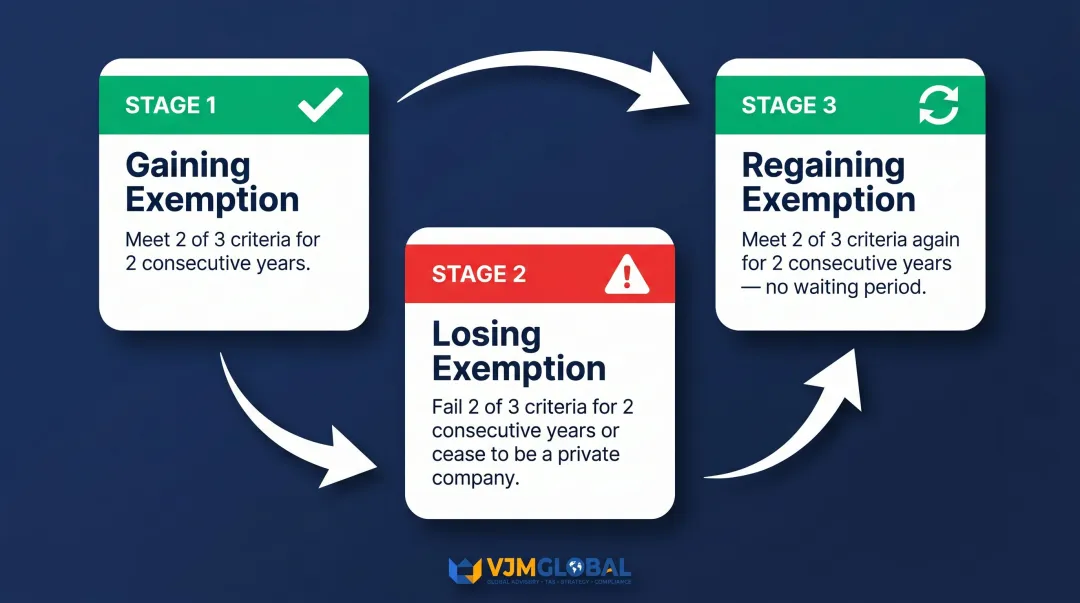

Audit exemption status is not permanent—it must be reassessed annually based on current performance.

A company retains small company status unless:

Example of losing status:

Financial YearMeets 2 of 3?StatusFY2021Yes ✓ExemptFY2022No ✗Still exempt (first fail)FY2023No ✗Loses exemption from FY2024

Failing the criteria in just one year does not trigger loss of status. The company must fail for two consecutive years before audit exemption ends.

Companies that lose small company status can automatically requalify. To do so, they must satisfy the same conditions that originally qualified them:

Re-Qualification ConditionRequirementCompany typeMust remain a private companyFinancial criteriaMust meet 2 of 3 thresholds for two consecutive financial yearsWaiting periodNone — status is restored immediately once conditions are met

There is no penalty for having previously lost exemption. Once the criteria are met again for two consecutive years, the company regains exempt status from the following financial year.

Audit exemption reduces costs but does not eliminate core financial responsibilities.

Maintain proper accounting records (Section 199)

Records must accurately reflect the company's financial position and enable preparation of compliant financial statements.

Prepare financial statements per SFRS

All exempt companies must prepare annual financial statements that comply with Singapore Financial Reporting Standards, even without an auditor's signature.

File annual returns with ACRA

Annual returns must be filed on time. Depending on company size and structure, financial statements may need to be submitted in XBRL format:

Under Section 205D, the Registrar can require an otherwise exempt company to lodge audited financial statements if deemed necessary. This means:

For foreign businesses managing entities across multiple jurisdictions—such as a UK parent with subsidiaries in both Singapore and India—maintaining consistent, compliant books becomes especially complex. VJM Global supports businesses navigating exactly this complexity. With 30+ years of cross-border accounting and compliance experience, the firm helps international companies manage bookkeeping, meet filing deadlines, and align subsidiary reporting with group-wide standards—particularly for clients with India operations alongside other jurisdictions.

Even when a company qualifies for audit exemption, certain situations may still require one — either voluntarily or by contractual obligation:

Important: In these cases, the audit exemption technically still applies — the company is choosing to audit for commercial or contractual reasons, not because statute requires it. Directors should keep a written record of why the voluntary audit was commissioned, particularly if shareholders or lenders request it.

Not automatically — but newly incorporated companies (under two years old) can qualify by meeting 2 of the 3 size criteria in a single financial year, without needing two consecutive years of history.

Yes. Unlike the old exempt private company framework, the small company concept places no restrictions on shareholder types. Corporate shareholders do not disqualify a company from audit exemption.

The company must arrange for a statutory audit starting from the financial year it no longer qualifies. However, it may requalify in a later year if it meets the criteria again for two consecutive years.

No. Audit exemption removes the auditor requirement only. Companies must still prepare financial statements in accordance with SFRS and file annual returns with ACRA on time.

Yes. Under Section 205D, the Registrar can direct an otherwise exempt company to lodge audited accounts when it sees fit — so maintaining clean, complete records is advisable regardless of your exemption status.

No. The exemption under Section 205C is exclusively for private companies. Public companies must have their accounts audited regardless of size.