Poor bookkeeping costs UK small businesses far more than just accountant fees. Beyond the legal obligation to maintain accurate records, inadequate bookkeeping leads directly to cash flow crises, overpaid taxes, and HMRC penalties that can cripple a growing business. HMRC collected £786 billion in tax revenue in 2024-25, and with the tax gap—the difference between tax owed and tax collected—standing at 5.3%, compliance scrutiny has intensified significantly.

UK-specific factors compound the challenge. Making Tax Digital (MTD) requirements mean VAT-registered businesses must now use digital record-keeping and submit returns through compatible software. The VAT registration threshold stands at £90,000 as of April 2024, and MTD for Income Tax will mandate quarterly digital updates from April 2026 for self-employed individuals and landlords earning above £20,000. The stakes have risen: accurate bookkeeping is no longer just good practice—it's a legal necessity that directly impacts your bottom line.

This guide covers everything small UK businesses need to know: legal record-keeping requirements, bookkeeping methods that suit different business stages, MTD obligations and compliance steps, and practical strategies you can implement immediately.

Key Takeaways:

Bookkeeping is the day-to-day recording of every financial transaction your business makes: income received, expenses paid, purchases made, and payroll processed. Accounting, by contrast, interprets that data to produce financial reports, file tax returns, forecast cash flow, and guide strategic decisions.

In practice, bookkeeping feeds accounting: clean, accurate records make tax filings, cash flow forecasts, and investor reports possible.

Every UK small business must maintain three core financial records as a legal minimum:

These cover the legal minimum — VAT-registered businesses face further obligations on top, including detailed VAT invoices showing tax charged and reclaimed, and quarterly return records submitted through MTD-compliant software.

Accurate bookkeeping directly feeds your compliance obligations and business decisions:

HMRC mandates that UK businesses retain financial records for a minimum of six years from the end of the relevant company accounting period. This isn't a suggestion — HMRC can request records during investigations, and inadequate documentation results in penalties even if your tax calculations were correct.

Mandatory documentation includes:

Records must be complete, up to date, clearly show all business income and expenditure, and be stored securely in either digital or paper format. "Up to date" means within the tax filing deadlines, but best practice is weekly or monthly updates to catch errors early and keep your cash flow picture current.

During an HMRC investigation, incomplete records can result in estimated tax assessments that often exceed your actual liability. Penalties range from hundreds to thousands of pounds, depending on the severity and whether HMRC suspects deliberate error.

Businesses with taxable turnover above the £90,000 VAT registration threshold must maintain:

If you employ staff, you must maintain:

Three main bookkeeping approaches exist for UK small businesses: single-entry (including basic spreadsheets or cashbooks), double-entry, and the choice between cash-basis and accrual accounting. The right method depends on your business size, complexity, and whether you're VAT-registered or a limited company.

Single-entry records each transaction once, like a simple cashbook showing money in and money out. It's straightforward but limited:

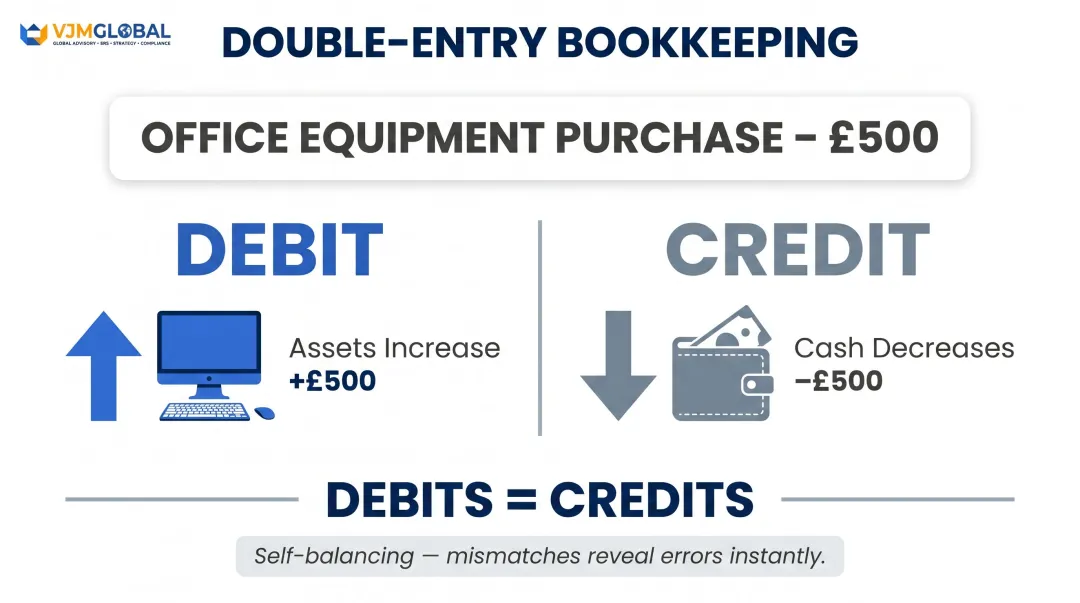

Every transaction is recorded twice—as both a debit and a credit—providing a complete picture of assets, liabilities, revenues, and expenses. This method is self-balancing: if debits don't equal credits, you know an error exists.

Required for:

Benefits:

Once you've chosen how to structure your records, you also need to decide when to record transactions. That's where cash-basis and accrual accounting differ.

Cash-basis accounting records income and expenses when money actually changes hands. Accrual accounting records income when earned and expenses when incurred, regardless of payment timing.

Cash-basis:

Accrual (traditional):

A chart of accounts is a categorised list of every account used to record transactions. It typically covers:

Keeping these categories consistent lets you:

Making Tax Digital (MTD) is HMRC's initiative requiring businesses to maintain digital financial records and submit returns through MTD-compatible software. MTD for VAT became mandatory in April 2019 for all VAT-registered businesses. VAT is the phase already in effect — income tax requirements are being introduced in stages from 2026 onwards.

Key MTD for VAT obligations:

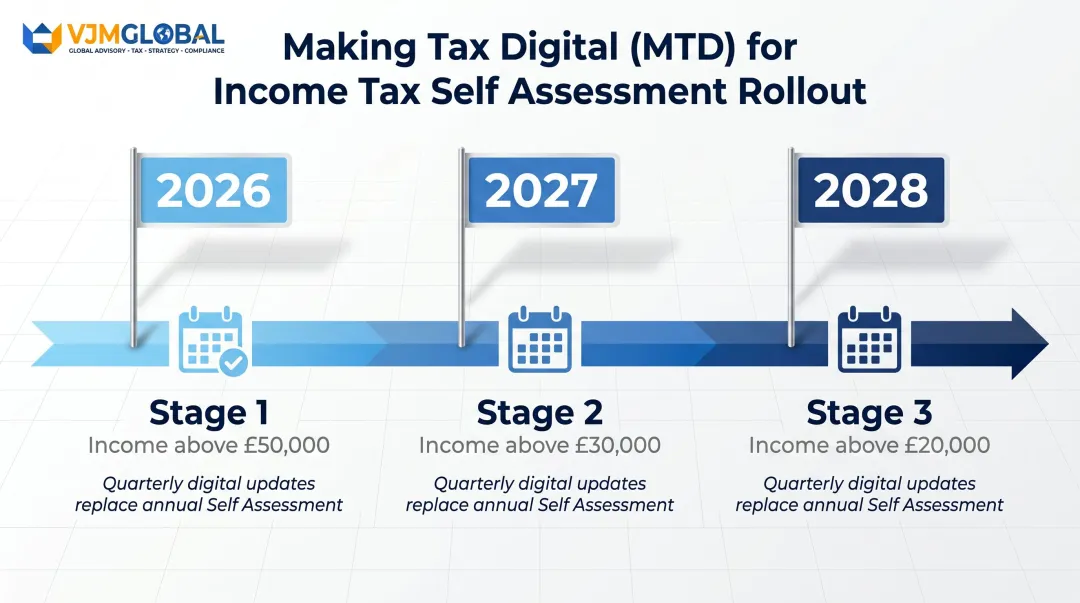

MTD for Income Tax rolls out in stages for self-employed individuals and landlords:

Instead of one annual Self Assessment return, affected businesses will submit quarterly updates to HMRC digitally — giving HMRC an up-to-date view of income and expenses throughout the year.

To prepare for MTD:

HMRC can issue penalties for:

Penalties vary based on severity and whether errors appear deliberate, but non-compliance can result in fines ranging from £200 for initial late submissions to percentage-based penalties for extended delays or inaccuracies. Checking your obligations now — rather than scrambling at the deadline — is the simplest way to avoid them.

Open a dedicated business bank account and run all business income and expenses through it exclusively. Mixing personal and business finances is one of the most common—and costly—mistakes small business owners make.

Why this matters:

Reconcile your bookkeeping records against bank statements every month — ideally on a fixed date. This catches errors, duplicate entries, and missing transactions early, before they compound into bigger problems.

How often you update records between reconciliations depends on volume:

Update FrequencyBest ForWeeklyMost small businesses with regular transactionsBi-weeklyBusinesses with moderate activityMonthlyVery small businesses with minimal transactions

Consistency prevents the dreaded year-end scramble and ensures you always have an accurate view of cash position and profitability.

Store digital copies of all receipts, invoices, and bank statements as they're received. Waiting until year-end to organise documents guarantees lost receipts and missed deductions.

Simple habits make a real difference:

MTD requirements make digital storage not just best practice but a legal necessity for VAT-registered businesses and, soon, for all self-employed individuals above the income threshold. HMRC also requires businesses to retain records for six years (five years for the self-employed), so a well-organised digital archive protects you well beyond the current tax year.

Generate at minimum a monthly profit-and-loss statement and balance sheet. These reports should drive business decisions, not just satisfy compliance obligations.

Use bookkeeping data to:

Most small business owners who review monthly reports regularly say the same thing: they spotted a problem — a supplier overcharge, a slow-paying customer, a margin that had quietly eroded — weeks earlier than they would have otherwise. That early warning is where the real value of good bookkeeping sits.

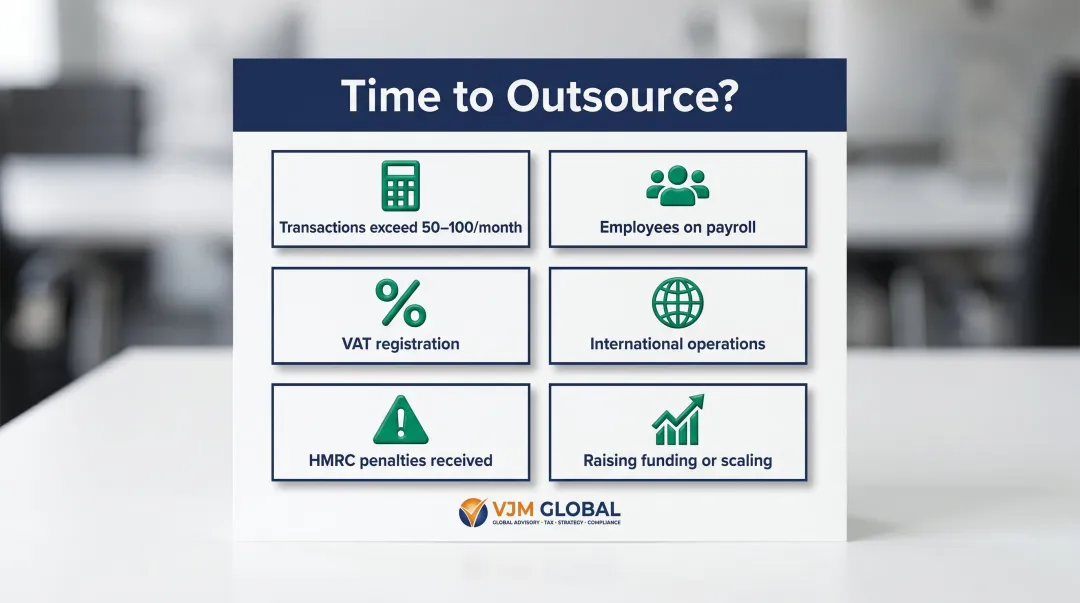

DIY bookkeeping works in limited circumstances: early-stage businesses with fewer than 50 transactions per month, simple structures, and owners who have both the financial knowledge and the time to do it properly.

The real question is whether it's the best use of your time. If bookkeeping takes 10 hours per month and your billable rate is £50 per hour, that's £500 in lost revenue — often more than professional bookkeeping costs.

Outsourcing becomes worthwhile when:

Specialist bookkeeping firms don't just maintain accurate records. They provide:

VJM Global has supported over 250 UK businesses through outsourced accounting, providing cost-effective access to qualified professionals without the overhead of an in-house hire. Core services include monthly reconciliation, VAT return preparation, payroll management, and strategic management reporting — all delivered with bank-level data security and a 95% client retention rate.

The five core principles are:

Bookkeeping is the day-to-day recording and organisation of financial transactions. Accounting uses that data to analyse financial performance, produce statutory reports, file tax returns, and develop tax and growth strategies.

HMRC requires UK businesses to keep financial records for at least six years from the end of the relevant company accounting period. Missing records can trigger penalties during an audit, and HMRC may estimate your tax liability higher than your actual figures.

MTD is HMRC's initiative to digitise tax administration. MTD for VAT already applies to all VAT-registered businesses, requiring digital records and quarterly submissions via compatible software. MTD for Income Tax applies from April 2026 to self-employed individuals and landlords earning above £50,000, with the threshold reducing to £30,000 in April 2027 and £20,000 in April 2028.

Very small businesses may start with spreadsheets, but MTD rules require VAT-registered businesses and soon income tax filers to use HMRC-recognised software with digital links between systems. Purpose-built bookkeeping software is the practical and compliant choice for most businesses, particularly those approaching or exceeding VAT registration thresholds.

Outsourcing makes sense when monthly transactions exceed 50-100, employees are on the payroll, VAT or MTD obligations kick in, or the time spent on DIY bookkeeping costs more than professional support. For growing businesses, that point often arrives within the first 12-18 months of trading.