%20(3).jpg)

Most finance leaders discover how complex Singapore amalgamations really are only after execution — when a misapplied accounting method or a missed tax election triggers liabilities that could have been avoided. Under the Companies Act (Cap. 50), amalgamation transfers all property, rights, liabilities, and obligations of the merging entities to a single surviving company. The accounting and tax consequences of that transfer are where the real decisions lie.

This guide is written for CFOs, tax managers, and finance directors at Singapore-incorporated companies — and for multinational groups restructuring regional entities. The legal procedure is well-documented; what rarely gets explained together is the SFRS(I) 3 accounting treatment, the irrevocable Section 34C tax election, and the strategic trade-offs between them.

The IRAS guidance confirms that 90-day election deadlines are frequently missed, permanently costing companies deferred tax benefits and loss carryforwards. This guide covers both choices — and what's at stake with each.

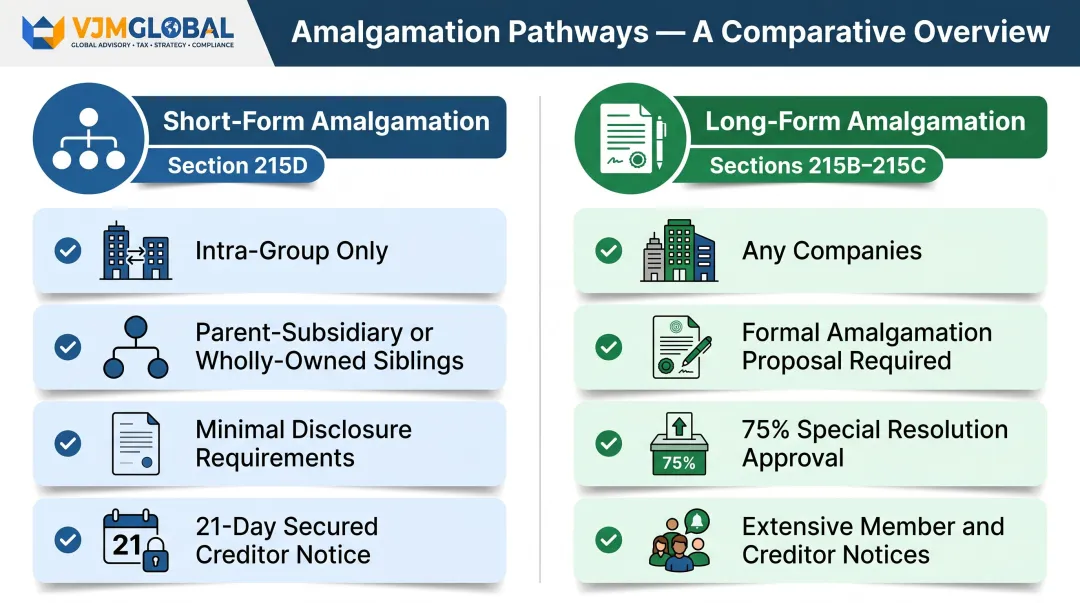

Amalgamation under Sections 215A–215K of the Companies Act 1967 is the process whereby two or more Singapore-incorporated companies combine into one entity, with all assets, liabilities, and obligations transferring automatically to the surviving (amalgamated) company by operation of law. Unlike a standard merger via asset or share transfer, amalgamation creates statutory vesting — property rights transfer without separate legal transfers for each asset.

Short-form amalgamation (Section 215D) is available for intra-group companies:

Long-form amalgamation (Sections 215B–215C) applies to any companies:

Unlike straightforward business transfers, amalgamation triggers specific questions that determine financial outcomes:

Accounting questions:

Tax questions:

The intersection of SFRS requirements and Income Tax Act provisions creates layers of complexity that go well beyond the legal mechanics of amalgamation. Getting the accounting treatment and tax elections right from the outset avoids costly corrections after the amalgamated company is already operational.

The applicable accounting standard depends on the economic substance of the amalgamation, not just its legal form.

When it applies: Long-form amalgamations between unrelated parties that meet the definition of a "business combination."

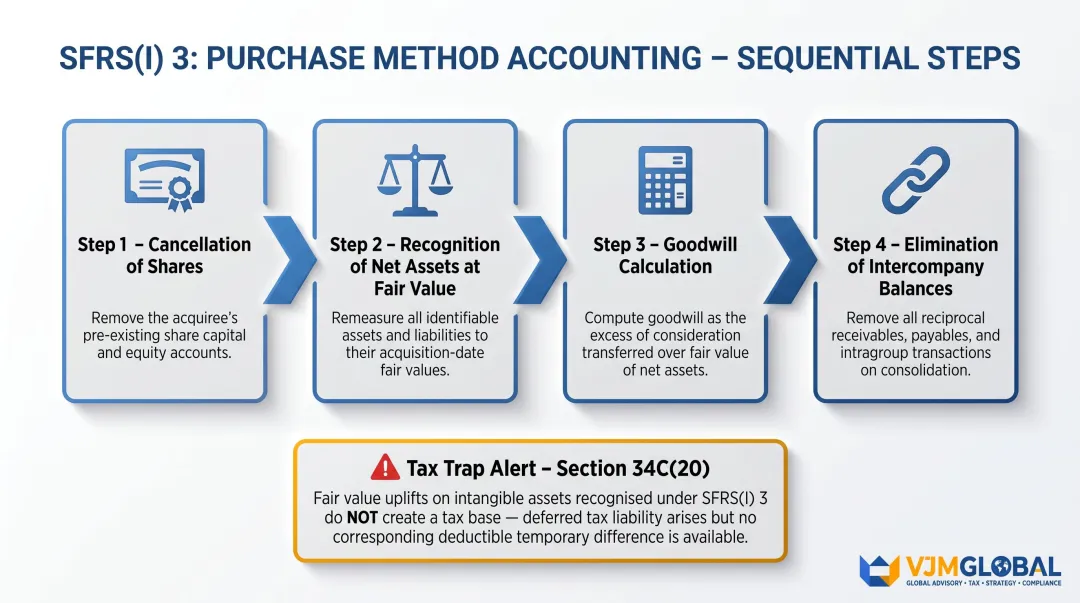

SFRS(I) 3, the Singapore equivalent of IFRS 3, requires the purchase (acquisition) method:

Key requirements:

Critical accounting entries:

Tax trap under Section 34C(20): No writing-down allowance (WDA) is granted for intellectual property rights recognized solely due to SFRS(I) 3 purchase accounting that did not exist as assets pre-amalgamation. Fair value uplifts that create new intangible assets generate no corresponding tax benefit.

When it applies: Short-form intra-group amalgamations where combining entities are under common control.

SFRS(I) 3 explicitly excludes common control combinations from its scope. Entities must develop accounting policies under SFRS(I) 1-8; ISCA RAP 12 recommends merger/pooling accounting as the preferred approach.

Key features:

The choice of accounting method directly shapes your post-amalgamation tax compliance workload. Purchase method creates the more complex outcome:

Merger accounting keeps the tax picture much cleaner:

The accounting method must be determined before amalgamation execution — not retrospectively. Getting this wrong means correcting misstated goodwill, unwinding non-deductible intangibles, and rebuilding deferred tax schedules from scratch.

Section 34C applies only to amalgamations where ACRA issues a Notice of Amalgamation under Section 215F on or after 22 January 2009, or where the Minister approves the amalgamation.

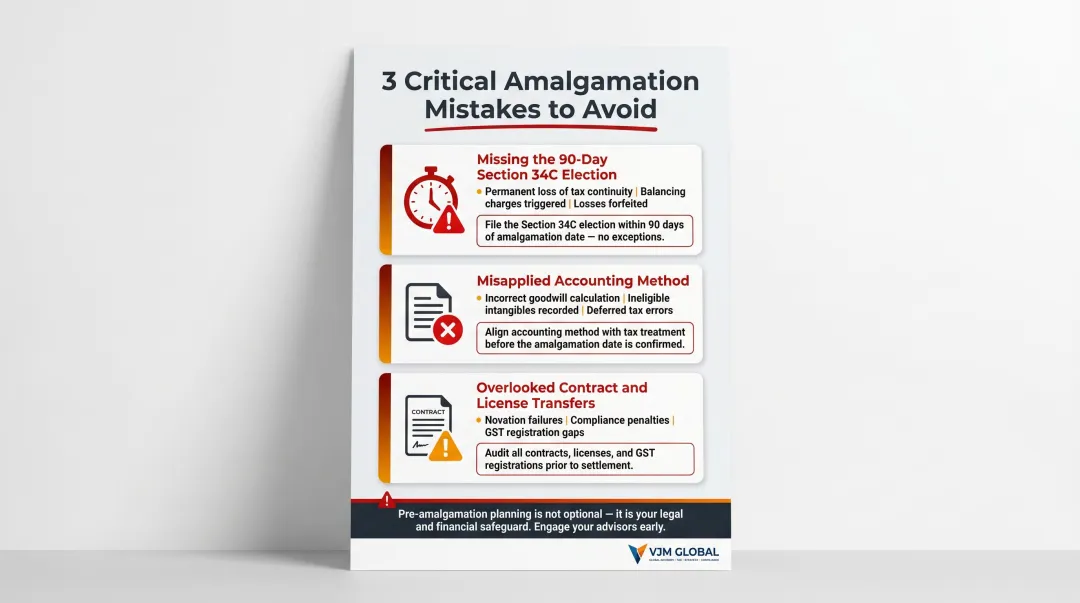

Critical requirement: The amalgamated company must make a formal, irrevocable election within 90 days of the amalgamation date.

Without this election:

When the Section 34C election is made, the amalgamation is treated as a seamless continuation of business — not a cessation and restart. Three key continuity rules flow from this:

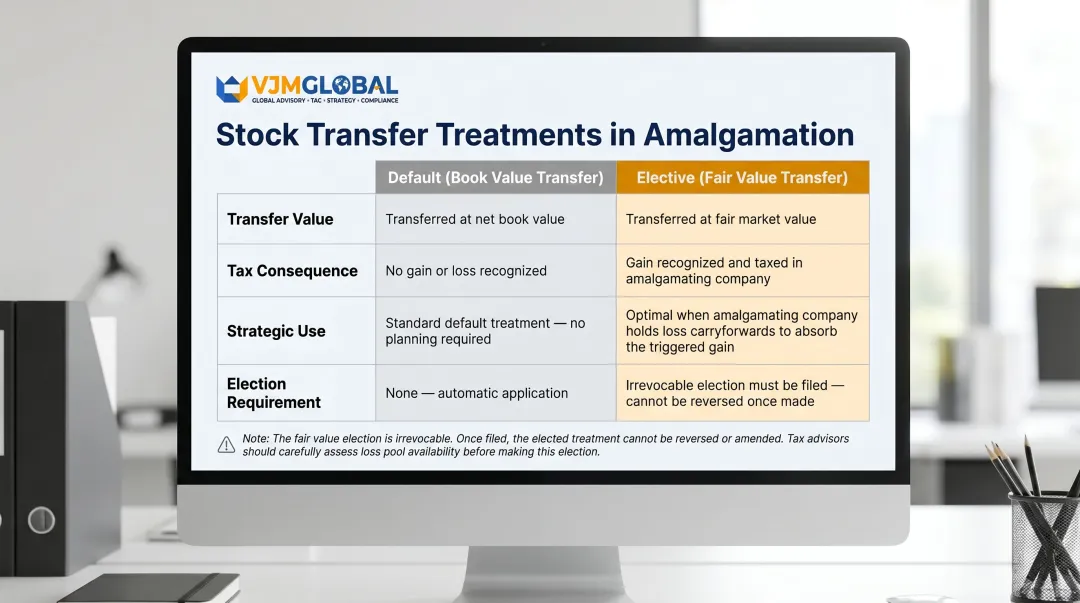

TreatmentDefault (NBV)Elective (Fair Value)Transfer valueNet book value as reflected in amalgamating company's booksFair value as reflected in financial accountsTax consequenceNo profit/loss recognized in amalgamating companyGain (FV minus NBV) taxed in amalgamating company in year of assessment covering amalgamation dateStrategic useStandard treatmentCan be used where amalgamating company has losses to absorb the gainElectionAutomaticIrrevocable, must cover all stocks from that amalgamating company

The table above assumes trading stock remains on the revenue account after transfer. Where an asset switches accounts entirely — from revenue to capital or vice versa — different rules apply.

Section 34C(14): Revenue to capital

Where property moves from revenue account in the amalgamating company to capital account in the amalgamated company:

Example: Amalgamating Company A holds inventory (revenue account) valued at $500,000 (NBV). Amalgamated Company B intends to hold these items as fixed assets, so transfer occurs at open market value of $600,000 — the $100,000 gain is taxable in Company A's hands.

Section 34C(16): Capital to revenue

Where property moves from capital account to revenue account, the treatment differs: consideration is the lower of open market value or actual payment, deductible as an expense in the amalgamated company when the stock is eventually sold.

Example: Amalgamating Company C holds equipment (capital account) with a TWDV of $200,000 and OMV of $250,000. Amalgamated Company D will hold it as trading stock — transfer consideration is set at $250,000, which Company D deducts upon eventual sale.

Section 34C(7) addresses a frequently overlooked trap:

When an amalgamating company holds shares in another amalgamating company and those shares are cancelled:

This directly affects leveraged intra-group restructurings where acquisition debt remains outstanding after amalgamation — a planning point that is often missed until the deduction is denied.

Under Sections 34C(23) and (24), unabsorbed capital allowances, trade losses, and donations of an amalgamating company can transfer to the amalgamated company, but only if two conditions are met:

Condition 1: Business continuity (amalgamating company)

Condition 2: Business continuity (amalgamated company)

Ring-fencing restriction (Section 34C(25)):

Transferred deductions may only be set off against income from that same trade or business, not against other income streams of the amalgamated company.

Transferred losses cannot shelter unrelated income — which makes the choice of amalgamated entity strategically important. The amalgamated company must maintain separate income tracking to stay compliant with ring-fencing requirements.

These ring-fencing rules connect directly to how capital allowances are handled. Under Section 34C(8), the amalgamation preserves continuity for plant, machinery, and industrial buildings.

Section 34C(8) treatment:

For plant, machinery, and industrial buildings on which allowances were previously granted:

Section 34C(8A) provides additional continuity for Section 18C building allowances.

Instruments relating to asset transfers during a qualifying amalgamation may qualify for ad valorem stamp duty relief under Section 15 of the Stamp Duties Act, provided:

Conditions:

Submission deadlines:

Retention period: 2-year asset/share retention period applies, with clawback provisions including 6% annual interest if breached.

Where an amalgamation constitutes a Transfer of a Business as a Going Concern (TOGC) under Regulation 10 of the GST (General) Regulations, the transfer may be treated as neither a supply of goods nor services and thus outside the scope of GST.\

Five conditions must be satisfied:

Important limitations:

Many companies assume that because amalgamation is a legal unification — not a third-party sale — there are no immediate tax consequences. Without the Section 34C election, that assumption is costly:

Missing the 90-day irrevocable election window makes these tax consequences permanent — there is no mechanism to reverse them.

Applying purchase method accounting (fair value) to a common control amalgamation — or merger accounting where it doesn't belong — creates a cascade of downstream errors:

The accounting method must be determined before the amalgamation is executed, not retrospectively. The choice depends on the relationship between companies (common control vs. business combination) and determines both accounting presentation and tax consequences.

This accounting misstep often compounds the tax errors above — making the method decision one of the earliest and most consequential choices in the process.

Statutory vesting does not automatically carry over every business relationship. Companies frequently overlook the need to actively transfer employment contracts, licenses, and third-party agreements — with real compliance consequences:

When these transfers are missed, income may continue to be reported under a company that no longer legally exists — triggering compliance failures and potential penalties.

Best practice: Seek counterparty consent for material contracts prior to amalgamation, particularly those governed by foreign law where Singapore statutory vesting may not be recognized.

Amalgamation follows either the short form (Section 215D, for wholly-owned intra-group companies) or long form (Sections 215B–215C, for any companies) procedure. Both require director solvency statements, shareholder resolutions, and lodgement with ACRA, culminating in a Notice of Amalgamation that triggers automatic vesting of assets and liabilities.

SFRS(I) 3 (Business Combinations) applies to amalgamations between unrelated parties and requires the purchase method. Common control amalgamations may instead use merger (pooling of interests) accounting, which is a permitted policy choice under SFRS(I) 1-8.

The purchase method records net assets at fair value and may recognize goodwill. Merger accounting (pooling of interests) combines assets and liabilities at historical book values with no goodwill recognized.

Under Section 34C(23), unabsorbed losses and capital allowances transfer to the amalgamated company if business continuity conditions are met. The amalgamated company must continue the same trade or business, and transferred deductions can only be applied against income from that specific trade.

The Section 34C election is a written, irrevocable notice submitted to IRAS within 90 days of the amalgamation date. It must cover all amalgamating companies and, once made, activates tax continuity provisions that prevent adverse tax consequences on asset and trading stock transfers.

If the amalgamation qualifies as a transfer of a going concern (TOGC) under Regulation 10 of the GST (General) Regulations, the transfer falls outside the scope of GST. Key conditions include both parties being GST-registered and the transferee using the assets for taxable supplies — consult IRAS before proceeding.