Imagine a UK manufacturing company acquires a trading subsidiary in India to expand its supply chain. Overnight, the finance director faces a critical question: do we now need to prepare consolidated group accounts? This scenario is increasingly common as UK businesses expand through acquisitions and subsidiary structures, yet many directors remain uncertain about their obligations under the Companies Act 2006.

Consolidated (or group) accounts present a parent company and all its subsidiaries as a single economic entity. Internal transactions between group members are eliminated, giving a clear picture of the group's overall financial position.

Under CA 2006 Section 399, UK parent companies have a statutory duty to prepare these accounts alongside their individual company accounts, unless they qualify for an exemption.

This guide covers who must prepare consolidated accounts, the size thresholds that trigger the requirement, available exemptions, what the accounts must contain, and the step-by-step preparation process.

Consolidated accounts combine the financial results of a parent company and all its subsidiaries, eliminating intra-group transactions to present the group as a single reporting entity. CA 2006 s399 defines them as comprising:

Under CA 2006 s1162, a parent-subsidiary relationship exists when the parent:

Important: Ownership need not be 100%. Control at any level—even 51%—can create a parent-subsidiary relationship requiring consolidation.

If your company is registered in the UK and has subsidiaries incorporated overseas, those entities must be included in your consolidated accounts. CA 2006 s1173(1) defines "body corporate" to include entities incorporated anywhere with separate legal personality. The subsidiary's country of incorporation does not affect this obligation. What counts is that the parent is UK-registered and exercises control.

UK parent companies choose between two frameworks based on their size and market status:

FrameworkWho Uses ItKey CharacteristicsComplexityFRS 102 (Companies Act)Most private groupsFollows UK GAAP; Section 9 covers consolidated statementsLower — practical for SMEsUK-adopted IASRequired for listed companies; optional for othersInternationally recognised; once adopted, must continue unless circumstances changeHigher — suited to cross-border groups

Whichever framework applies, the obligation to file on time remains the same.

Consolidated accounts must be filed at Companies House within:

Under CA 2006 s451, failure to file on time is a criminal offence for every director who held office at the deadline. Personal penalties include:

Companies House civil penalties also apply to the company itself, ranging from £150 (up to 1 month late) to £1,500 (over 6 months late).

The obligation to prepare consolidated accounts is tied directly to group size. Under CA 2006 s399, parent companies need not prepare group accounts if the group qualifies as "small."

Following SI 2024/1303, groups qualify as small if they meet at least 2 of these 3 criteria:

CriterionNet FigureGross FigureAggregate turnover≤ £15m≤ £18mAggregate balance sheet total≤ £7.5m≤ £9mAverage employees≤ 50≤ 50

Net vs Gross:

The previous limits were:

This represents a 47% increase in the turnover threshold — groups that sat just above the old limits may now qualify for exemption for the first time.

Regulation 3 of SI 2024/1303 provides an important shortcut: groups can treat the new thresholds as having applied in the prior year.

This bypasses the usual two-year qualification rule. Newly eligible groups can claim exemption in their first qualifying year beginning on or after 6 April 2025, without waiting an additional year to establish the two-year track record.

Generally, groups must meet the size criteria for two consecutive financial years to qualify as small. The one exception: a group's first financial year — if it meets the thresholds in year one, it qualifies immediately.

Once qualified, a single year above the limits does not immediately remove exemption. Two consecutive years above the thresholds will trigger the consolidation requirement.

Certain entity types cannot use the small group exemption regardless of size. If your group includes any of the following, you must prepare consolidated accounts:

Note: Companies listed on AIM are not considered to be on a "regulated market" and may use the small group exemption if they meet size criteria.

Even if your group exceeds the small group thresholds, three statutory exemption routes may apply.

The most common route. If your group qualifies on size and contains no ineligible entities, the parent need not prepare consolidated accounts.

Conditions:

A UK subsidiary that is itself a parent can avoid preparing its own consolidated accounts if a higher UK parent already consolidates it.

Conditions:

This exemption does not apply to traded companies.

Where the ultimate parent is incorporated outside the UK, a similar exemption is available — but with additional filing obligations for the foreign group accounts.

Conditions:

This exemption does not apply to companies with securities on a UK regulated market.

The exemptions above apply at the parent level. Separately, FRS 102 paragraph 9.9 allows individual subsidiaries to be excluded from consolidation on specific grounds — though this does not remove the parent's overall obligation to consolidate:

Excluded subsidiaries must still be accounted for as financial instruments under FRS 102 Sections 11 and 12.

All subsidiary undertakings where the parent has control must be consolidated. Control is determined by:

This applies equally to UK and overseas subsidiaries. A UK parent with an Indian trading subsidiary and a German manufacturing subsidiary must consolidate both.

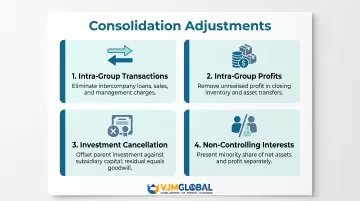

Four categories of adjustments are required to produce a true and fair group picture:

Intra-group transactions — eliminate all loans, intercompany sales and purchases, and management charges between group entities so only external activity is reported.

Intra-group profits — remove unrealised profit sitting in closing inventory from parent-to-subsidiary sales and adjust for unrealised gains on asset transfers.

Investment cancellation — cancel the parent's investment in subsidiary shares against the subsidiary's share capital and reserves, with any remaining difference treated as goodwill.

Non-controlling interests — present minority shareholders' share of net assets and profit or loss separately from the parent shareholders' interests within equity.

Goodwill arises when the purchase price exceeds the fair value of the subsidiary's net assets at acquisition. Under FRS 102:

Where the purchase price falls below fair value of net assets — known as negative goodwill or a bargain purchase — a different treatment applies:

All group entities must apply consistent accounting policies when preparing consolidated accounts. If a subsidiary uses different policies, adjustments must be made on consolidation to align with group policies. Where adjustment is impracticable, full disclosure of the inconsistency is required.

Group companies should prepare accounts to the same period-end. FRS 102 paragraph 9.16 allows subsidiaries to report up to three months before the parent's year-end if preparing to the same date is impracticable. When using different period-ends, adjust for significant transactions or events occurring between the subsidiary's reporting date and the parent's reporting date.

For groups managing complex multi-entity structures, applying these requirements consistently across jurisdictions can be challenging. VJM Global's accounting and compliance team supports UK businesses and international groups with consolidation, working across UK accounting standards and Companies House filing requirements.

With 30+ years of experience and 250+ UK businesses served, the firm draws on its global network as a member of EAI International to deliver technically compliant group accounts.

Start by collecting complete financial information from every entity in the group.

Collect individual financial statements and acquisition details:

Confirm alignment across the group:

With aligned financials in hand, work through four core adjustments in sequence.

Step 1 — Calculate and eliminate investment:

Step 2 — Eliminate intra-group balances:

Step 3 — Eliminate intra-group transactions:

Step 4 — Calculate non-controlling interests:

Once adjustments are complete, compile the consolidated statements and prepare for filing.

Consolidated statements to prepare:

Required disclosures include:

To sign off and file:

The process involves gathering individual financial statements from all group entities, performing consolidation adjustments (eliminating intra-group transactions, calculating goodwill, recognising non-controlling interests), and producing combined accounts that present the group as a single entity. These are then filed at Companies House within the statutory deadline.

Any UK-registered parent company with one or more subsidiaries must prepare consolidated accounts if the group exceeds the small group thresholds under CA 2006 s399. This applies regardless of where subsidiaries are incorporated—overseas subsidiaries must be included in UK parent consolidations.

For accounting periods beginning on or after 6 April 2025, groups qualify as small by meeting at least 2 of 3 criteria: aggregate turnover ≤£15m net (£18m gross), balance sheet ≤£7.5m net (£9m gross), and average employees ≤50.

Yes. If the parent company is registered in the UK, all subsidiaries—regardless of where they are incorporated—must be included in consolidated financial statements. The only exclusions are limited grounds under FRS 102 paragraph 9.9 (immateriality, severe restrictions, or held for resale).

Yes. Under CA 2006 s400 (UK parent) or s401 (non-UK parent), an intermediate parent may be exempt if already included in a higher group's consolidated accounts that meet required standards and are filed at Companies House. Specific shareholder approval conditions apply depending on ownership percentage.

Companies claiming the small group exemption must state this in their accounts under s399. Those using the intermediate parent exemption must disclose the parent's name, registered office, country of incorporation (if outside the UK), and where its accounts can be obtained. Copies of the parent's group accounts must also be filed at Companies House.

Need expert support with UK consolidated accounts? VJM Global's accounting team provides comprehensive consolidation services, from technical compliance under FRS 102 to Companies House filing. Get in touch at info@vjmglobal.com to discuss your group reporting requirements.