For many foreign business owners, the hard part isn't setting up a company in Singapore. Registration is straightforward and typically wraps up within days. The real challenge comes after incorporation: keeping up with ongoing annual filing and compliance obligations under Singapore's Accounting and Corporate Regulatory Authority (ACRA) and Inland Revenue Authority of Singapore (IRAS).

These recurring requirements are where costly mistakes happen. Business cessations in Singapore reached 60,445 in 2025, the highest recorded level since 2017. Many of those closures trace back to missed deadlines, accumulating penalties, and director disqualifications.

Singapore's regulatory environment is actively enforced. Penalties escalate quickly, and directors can face personal liability for persistent non-compliance.

This article covers the key annual filing and compliance requirements foreign companies must meet in Singapore. You'll learn what ACRA and IRAS expect, how obligations differ between foreign company branches and locally incorporated subsidiaries, and which deadlines matter most to avoid enforcement action.

Annual filing and compliance in Singapore refers to recurring statutory obligations imposed by ACRA and IRAS that all registered companies must fulfill each financial year—regardless of foreign ownership or parent entity location.

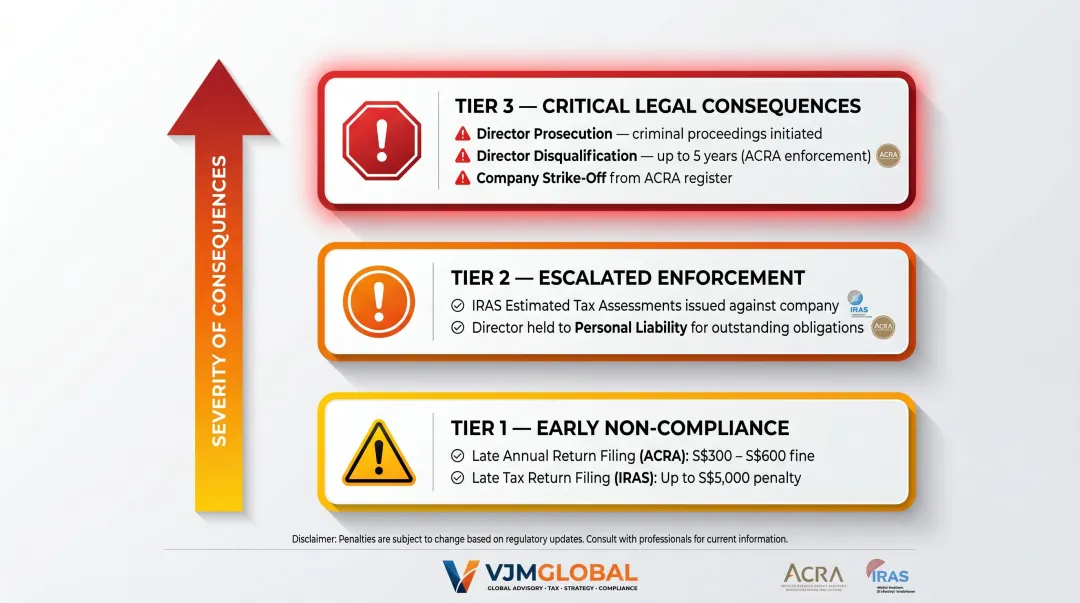

Singapore's regulatory environment is highly structured and actively enforced. Non-compliance carries real costs. According to ACRA's published guidelines, penalties include:

IRAS adds a separate layer of risk. When returns aren't filed on time, IRAS issues estimated tax assessments—typically set higher than actual tax owed. Directors face personal liability for missed deadlines, and enforcement actions follow individuals across future directorships.

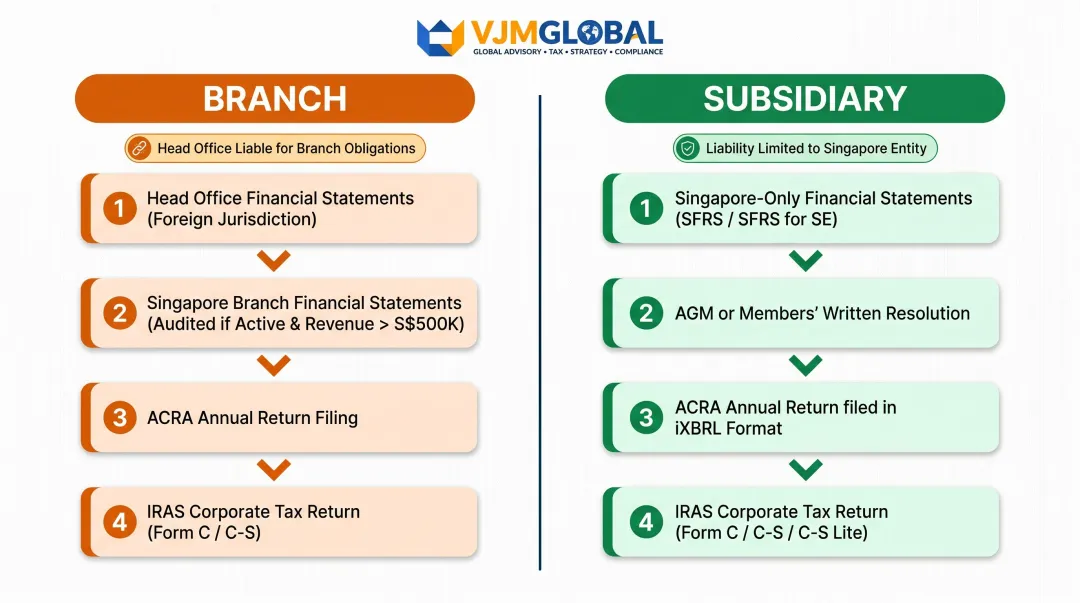

Foreign companies in Singapore fall into two categories, and the distinction directly shapes compliance requirements:

StructureLegal StatusLiabilityReporting ScopeSubsidiarySeparate Singapore-incorporated entityLimited to the subsidiarySingapore operations onlyBranchExtension of overseas parentParent bears full liabilityHead office + Singapore branch (dual filing)

Subsidiaries follow standard Singapore company rules. Branches carry a heavier reporting load—under Section 373 of the Companies Act 1967, they must file financial statements for both the Singapore branch and the overseas head office, which often requires document translation and additional audit work.

All Singapore-incorporated companies, including foreign-owned subsidiaries, must hold an AGM within 6 months of the financial year-end (FYE), unless all shareholders agree in writing to dispense with the AGM. Listed companies face a shorter deadline of 4 months after FYE.

During the AGM, directors present financial statements complying with Singapore Financial Reporting Standards (SFRS). Required components include:

Private companies may pass resolutions by written circulation instead of holding a physical meeting, under Sections 184A to 184F of the Companies Act. The resolution must reach all members entitled to vote, with the required majority confirming agreement in writing within 28 days.

Even when AGMs are dispensed with, financial statements must still be prepared and sent to all members within 5 months after FYE.

Failing to hold an AGM within the required period triggers fines under the Companies Act and potential director disqualification.

After the AGM (or once financial statements are finalized if AGM is exempt), the Annual Return must be filed with ACRA within 7 months of the FYE via the BizFile+ portal. Listed companies have 5 months; companies with overseas branch registers have extended deadlines (8 months for non-listed, 6 months for listed).

The Annual Return must include:

Late lodgement penalties start at $300, escalating to a maximum of $600. Non-compliance can further result in enforcement action, composition sums (out-of-court settlements), and court prosecution. All companies listed as "live" must file an annual return, even if dormant or having received a tax waiver from IRAS.

The Annual Return filing ties directly into format requirements. Most companies must submit financial statements in iXBRL (Inline eXtensible Business Reporting Language) format, which allows ACRA to electronically process structured financial data.

Exemptions from XBRL filing:

Foreign companies operating through subsidiaries should confirm with their local corporate secretary which filing format applies, as exemption eligibility depends on company size and structure at the time of each annual filing.

Singapore taxes companies on a preceding year basis at a flat rate of 17% of chargeable income. This applies to both local and foreign companies.

New companies benefit from the Start-Up Tax Exemption (SUTE) for the first three consecutive Years of Assessment (YA):

Companies not claiming SUTE receive the Partial Tax Exemption (PTE):

1. Estimated Chargeable Income (ECI)

Filed within 3 months after FYE, unless the company qualifies for exemption. Exemption applies when both conditions are met:

2. Corporate Tax Return

Form C, Form C-S, or Form C-S (Lite) must be filed by 30 November of the Year of Assessment via myTax Portal. Paper filing is no longer accepted. This applies to all companies, including those that did not carry on business or incurred a loss.

Late filing consequences:

Beyond direct tax filings, foreign companies with related-party transactions — with parent companies, subsidiaries, or sister entities abroad — face transfer pricing obligations when:

All transactions must follow the arm's length principle: pricing must reflect what unrelated parties would charge in similar circumstances.

Non-compliance risks:

Companies with cross-border related-party transactions — particularly those with parent or sister entities in India, the USA, UK, or Australia — should ensure documentation is in place before IRAS requests it, not after.

GST registration becomes mandatory once annual taxable turnover exceeds $1 million, either:

Voluntary registration is also available.

Once registered, companies must:

Late filing or non-payment brings financial penalties and potential suspension of GST registration.

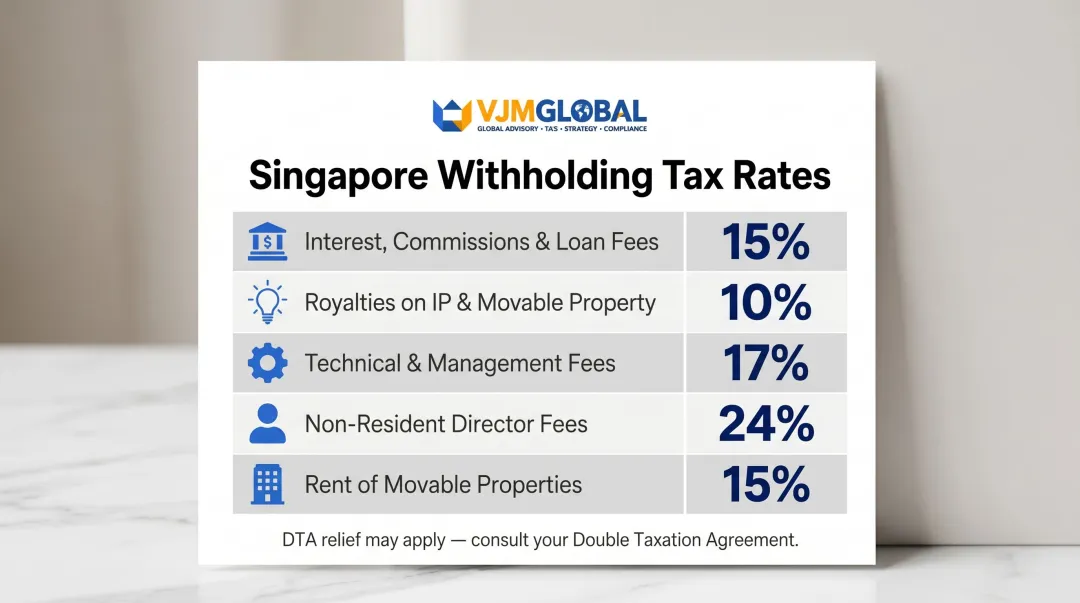

Separate from GST, payments to non-resident companies or individuals may trigger Singapore withholding tax. Common categories include:

Payment TypeWHT RateInterest, commissions, loan fees15%Royalties (IP/movable property)10%Technical/management fees17%Non-resident director fees24%Rent of movable properties15%

Applicable Double Taxation Agreements (DTAs) may reduce these rates. Verify treaty relief availability before processing each payment type.

Large multinational enterprises with consolidated group revenue above EUR 750 million may be subject to Singapore's Multinational Enterprise Top-up Tax (MTT) and Domestic Top-up Tax (DTT) under the GloBE rules.

The rules apply to financial years commencing on or after 1 January 2025 and target a minimum effective tax rate of 15% on under-taxed profits. Affected groups should assess exposure early — penalties for non-compliance apply even in the first year. Consult IRAS guidance on Pillar 2 top-up taxes for filing specifics.

Entity TypeLegal StatusLiabilityFiling ScopeBranchExtension of overseas parentParent bears full liabilityDual financial statements requiredSubsidiarySeparate Singapore-incorporated entityLimited liability (independent)Standard Singapore entity filings

Which structure you operate under directly shapes your financial reporting obligations under Section 373 of the Companies Act 1967.

Unlike subsidiaries, branches must file two sets of financial statements with ACRA:

The format of head office financial statements depends on whether the parent is listed and which accounting standards it uses. Listed companies must meet format requirements aligned with listing rules. Non-listed companies using IFRS or equivalent standards may file in the format used for their home jurisdiction.

Active branches must file audited branch financial statements.

Dormant branches may file unaudited statements. Under Section 205B of the Companies Act, a branch is dormant during any period when no accounting transaction occurs. Routine administrative actions don't count — specifically excluded are:

If your branch qualifies as dormant, audit exemptions can reduce your compliance burden significantly — which brings us to the formal waiver options available under Section 373.

ACRA may grant waivers from certain filing requirements:

Section 373(12): Complete waiver from filing Singapore branch financial statements (head office statements still required)

Section 373(13A): Relief from audit requirements and/or form-and-content requirements for branch statements

Submit applications via BizFile+ General Lodgement with a non-refundable fee of SGD 200.

Foreign companies may also apply for a 60-day extension for filing financial statements via BizFile+.

Many foreign directors assume compliance is primarily about tax filing. In reality, ACRA filings (AGM, Annual Return, financial statements) operate on separate deadlines and carry independent penalties.

Missing ACRA deadlines—even when tax filings are current—can result in the company being struck off the register. Compliance is multi-threaded and deadline-specific, not a single annual event.

Many parent corporations maintain centralized accounting functions outside Singapore and fail to provide local directors and company secretaries with timely access to Singapore-specific accounting records.

This creates bottlenecks at filing time and exposes local directors to personal liability for missed deadlines. Two specific obligations catch companies off guard:

Foreign companies with low or zero revenue often believe they have no compliance obligations. This is false.

Even if a Singapore company is dormant or has no income:

All companies listed as "live" must file an annual return, even if inactive, dormant, or having received a tax waiver from IRAS. Beyond tax and ACRA filings, companies holding operational licenses in regulated sectors — finance, education, food services — must separately track and renew those licenses. Dormant status does not pause these sector-specific obligations.

Any foreign business wishing to carry out commercial operations in Singapore must register with ACRA. Options include registering as a branch, incorporating a subsidiary, or setting up a representative office (which cannot earn income). A corporate service provider must be engaged to complete the registration process.

"Small companies" are exempt from statutory audit if they meet at least 2 of 3 criteria: annual revenue not exceeding S$10 million, total assets not exceeding S$10 million, and no more than 50 employees. They must still prepare SFRS-compliant financial statements. Dormant foreign company branches may file unaudited branch statements.

Singapore uses SFRS and SFRS(I) — both substantially aligned with IFRS, with SFRS(I) being identical to IFRS Accounting Standards. Foreign company branches may file head office financial statements prepared under IFRS or equivalent standards, depending on their home jurisdiction and listing status.

Late filings attract escalating monetary penalties from ACRA and IRAS. Persistent non-compliance can lead to prosecution of company directors, director disqualification for up to five years, and the company being struck off the register. IRAS may also issue estimated tax assessments that are typically higher than actual tax owed.

A branch is a direct extension of the overseas parent (with the parent bearing full liability), while a subsidiary is a separate Singapore-incorporated legal entity. Branches must file financial statements for both their head office and Singapore operations; subsidiaries follow standard local company compliance rules.

Yes. All Singapore companies must file annual corporate tax returns with IRAS — a nil return is required when there is no taxable income. ACRA filing obligations (Annual Return, financial statements) remain mandatory regardless of revenue.