Las empresas de Singapur que se expanden a la India se enfrentan a un obstáculo normativo inmediato: el año fiscal de la India va del 1 de abril al 31 de marzo, no sigue el año natural de enero a diciembre que utilizan la mayoría de las empresas singapurenses. Esa diferencia genera una fricción real en el cumplimiento normativo, y no se trata solo de un inconveniente de programación.

Cuando su empresa matriz en Singapur cierra sus libros el 31 de diciembre, pero su filial india opera con un ciclo de abril a marzo, se enfrenta a tres meses de retraso en la presentación de informes y a plazos fiscales desalineados. La conciliación entre empresas, la presentación de informes consolidados y las declaraciones legales requieren una coordinación cuidadosa en ambas jurisdicciones.

Esta guía detalla las normas del periodo contable de la India, cómo se comparan con el marco de Singapur y lo que su equipo financiero necesita para gestionar la realidad de la doble presentación de informes desde el primer día.

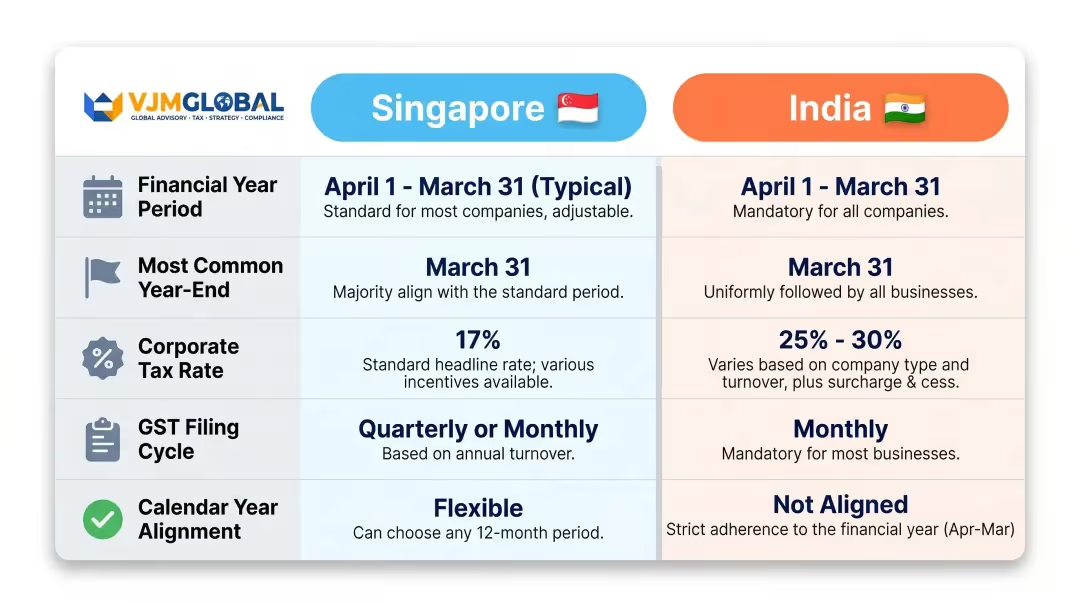

El año fiscal de la India (también llamado ejercicio fiscal o año contable) es un periodo de 12 meses que comienza el 1 de abril y termina el 31 de marzo del año natural siguiente. Por ejemplo, el año fiscal 2025-26 va del 1 de abril de 2025 al 31 de marzo de 2026.

Este ciclo es obligatorio por ley según la Sección 2(41) de la Ley de Sociedades de 2013, que define el "año financiero" como el periodo que termina el 31 de marzo de cada año. La Ley del Impuesto sobre la Renta de 1961 refuerza esto a través de sus definiciones de "Año Anterior" y "Año de Evaluación".

El sistema fiscal de la India utiliza dos conceptos distintos que suelen confundir a los equipos financieros de Singapur:

Por ejemplo, los ingresos obtenidos en el ejercicio fiscal 2025-26 (el año anterior) se evalúan y gravan en el año fiscal 2026-27 (el año de evaluación). Este desfase difiere notablemente del sistema de Singapur, donde los ingresos se evalúan en el mismo año en que se obtienen.

El ciclo de abril a marzo se remonta a 1867, cuando el gobierno colonial británico alineó el calendario fiscal de la India con el periodo contable de la Hacienda británica. Este calendario también coincidía con la temporada de cosecha agrícola de la India —las cosechas se producían de octubre a marzo—, lo que permitía al gobierno tener una visión más clara de los ingresos para abril. La India mantuvo este ciclo tras la independencia, ya que los sistemas administrativos y presupuestarios ya se habían construido en torno a él.

Aunque la mayoría de las empresas indias siguen el año de abril a marzo, históricamente han existido excepciones limitadas. La Ley de Sociedades de 2013 redujo significativamente estas excepciones al exigir un año financiero uniforme para todas las empresas registradas.

Puntos clave sobre las excepciones:

Comprender este marco hace que un elemento sea fundamental: el Presupuesto de la Unión. El gobierno de la India lo presenta en febrero —antes de que comience el año financiero—, lo que significa que los cambios fiscales entran en vigor antes de que finalice su ciclo de planificación.

Los ajustes de tasas, las normas de depreciación y los requisitos de cumplimiento anunciados en el presupuesto suelen aplicarse a partir del 1 de abril. Para las empresas de Singapur, esto significa que un anuncio presupuestario en febrero puede alterar su exposición fiscal en la India, sus supuestos de precios de transferencia o sus plazos de presentación con aproximadamente seis semanas de antelación. Vale la pena incluir un paso de seguimiento presupuestario en su calendario del primer trimestre.

Para las empresas matrices en Singapur con filiales en la India, esa diferencia en las fechas de cierre del ejercicio crea verdaderos desafíos de consolidación y presentación de informes, y no solo de carácter administrativo.

Una sociedad holding en Singapur que cierra sus libros el 31 de diciembre debe consolidar una filial india que solo cierra el 31 de marzo, lo que genera una brecha de tres meses en la presentación de informes.

Según las normas NIIF 10 y SFRS(I) 10 (Normas de Información Financiera de Singapur - Internacional), esta brecha de tres meses es el máximo permitido a efectos de consolidación. Las empresas suelen gestionar esto mediante:

Independientemente del enfoque utilizado, las políticas contables deben ser coherentes en ambas entidades, y cualquier transacción importante que ocurra entre los dos cierres de ejercicio debe identificarse y ajustarse en las cuentas consolidadas.

Singapur no tiene un concepto separado de "Año de Evaluación". Los ingresos se evalúan en el año en que se obtienen. En la India, la Año anterior/Año de evaluación distinción significa que una empresa que obtiene ingresos en el ejercicio fiscal 2025-26 solo ve su evaluación fiscal en el año de evaluación 2026-27.

Los equipos financieros de Singapur que revisan las provisiones fiscales indias en las cuentas intercompañía deben tener en cuenta este desfase; no hacerlo puede provocar que las obligaciones fiscales se atribuyan erróneamente al periodo incorrecto, distorsionando tanto las provisiones como las conciliaciones intercompañía.

Las declaraciones de GST en Singapur suelen presentarse trimestralmente. El GST de la India requiere:

El calendario del GST indio no sigue estrictamente el año fiscal; las declaraciones abarcan meses naturales, lo que genera obligaciones de cumplimiento durante todo el año que las empresas de Singapur deben gestionar de forma continua.

La frecuencia de las declaraciones del GST indio también tiene un efecto dominó en la documentación de precios de transferencia, ya que las facturas intercompañía que alimentan esas declaraciones deben tener precios consistentes durante todo el año.

Cuando las entidades de Singapur realizan transacciones con filiales indias, la documentación de precios de transferencia en la India debe cubrir el año fiscal de abril a marzo. La documentación de precios de transferencia de Singapur sigue el año fiscal de Singapur.

Las empresas de Singapur deben asegurarse de que sus políticas de precios intercompañía y documentación cubran ambos períodos y estén conciliadas, especialmente cuando los precios o los márgenes cambian durante el año. El Formulario 3CEB (informe de auditoría de TP de la India) vence el 31 de octubre del año de evaluación y cubre el año fiscal indio.

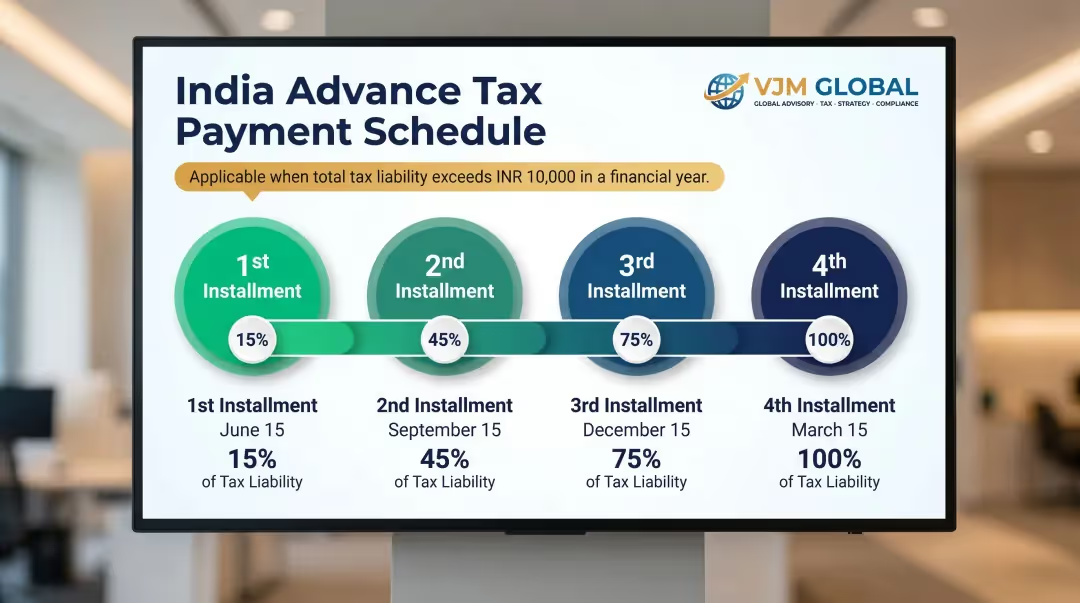

Si el impuesto total a pagar por el año supera las 10.000 INR, las empresas deben pagar impuestos anticipados en cuatro cuotas trimestrales:

El incumplimiento de estos pagos conlleva un interés del 1% mensual según las secciones 234B y 234C de la Ley del Impuesto sobre la Renta. Esto difiere del modelo de impuesto tras la evaluación de Singapur y toma por sorpresa a muchas empresas de Singapur cuando entran por primera vez en la India.

Plazos de presentación de las declaraciones trimestrales de TDS:

Los formularios aplicables incluyen el Formulario 24Q (TDS sobre salarios), el Formulario 26Q (pagos distintos a salarios) y el Formulario 27Q (pagos a no residentes).

Las filiales indias deben presentar declaraciones anuales, estados financieros y resoluciones de la junta ante el Ministerio de Asuntos Corporativos:

La presentación tardía de los formularios AOC-4 y MGT-7 conlleva una multa de 100 INR por día sin límite máximo, además de sanciones adicionales bajo la Sección 450 por infracciones continuas.

Para empresas de Singapur que operan a través de una sucursal u oficina de representación (no una filial constituida):

Un aspecto de cumplimiento adicional que cabe destacar: la India realiza ahora las evaluaciones fiscales de forma digital, sin audiencias presenciales. Las empresas de Singapur deben:

Los estados financieros individuales de la filial india abarcan de abril a marzo, mientras que las cuentas consolidadas del grupo matriz en Singapur suelen seguir el calendario de enero a diciembre. Este desfase no es exclusivo de la India —el Reino Unido y Australia también utilizan años fiscales que no comienzan en enero—, pero requiere procesos internos estructurados.

Los auditores del grupo en Singapur exigirán que se revele la diferencia en el ejercicio financiero en las cuentas consolidadas, y este mismo desfase se traslada a su ciclo de planificación.

Cuando una empresa de Singapur presupuesta de enero a diciembre, el plan de la filial india abarca dos ejercicios fiscales indios: de enero a marzo cierra un ejercicio y de abril a diciembre abre el siguiente. Los equipos directivos indios planifican y son incentivados según el ciclo de abril a marzo, lo que puede provocar que las prioridades locales se desincronicen con los objetivos del grupo.

Gestione esta brecha de forma deliberada mediante:

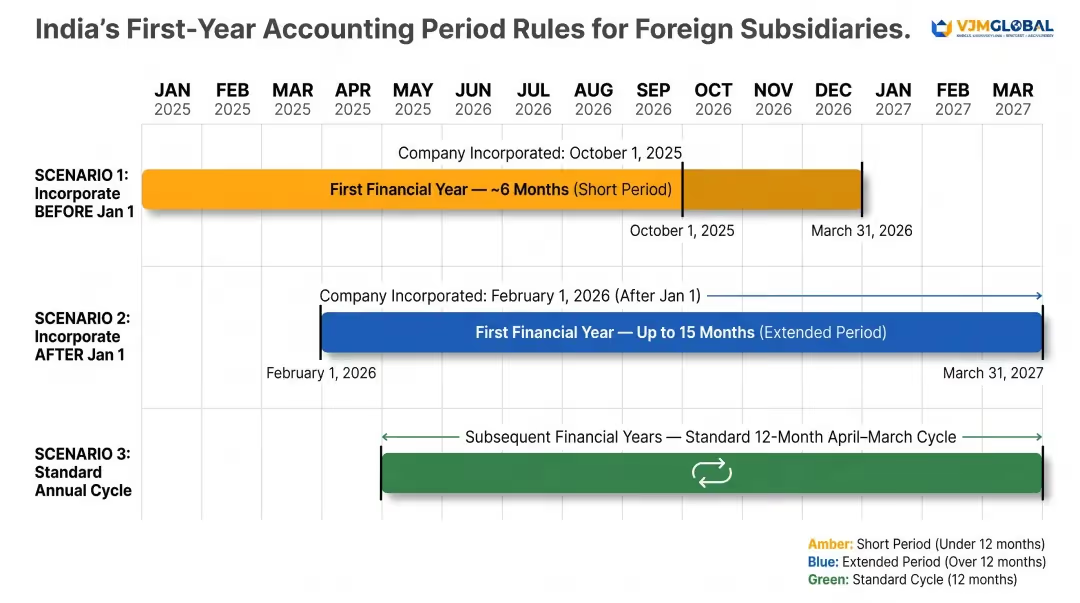

Cuando una empresa extranjera constituye una filial en la India, el primer ejercicio financiero puede ser más corto o más largo de 12 meses, pero debe finalizar el 31 de marzo.

Según la Sección 2(41) de la Ley de Sociedades de 2013:

Esto significa que el primer conjunto de cuentas auditadas en la India puede cubrir menos de 12 meses, lo cual debe comunicarse claramente a las partes interesadas de la empresa matriz en Singapur.

Las empresas extranjeras que operan a través de oficinas de enlace o de proyectos (entidades no constituidas) tienen requisitos de contabilidad y presentación de informes independientes bajo las regulaciones de FEMA y el RBI:

La Sección 2(41) establece una excepción limitada: las empresas que sean holdings, subsidiarias o asociadas de entidades constituidas en el extranjero pueden solicitar al Director Regional seguir un ejercicio fiscal diferente a efectos de consolidación.

Dos escenarios específicos en los que esto se aplica:

En la práctica, la mayoría de las filiales indias propiedad de empresas de Singapur operan bajo el ciclo estándar de abril a marzo.

Históricamente, el Banco de la Reserva de la India (RBI) utilizaba un año contable de julio a junio. A partir del 1 de abril de 2021, el RBI cambió al periodo de abril a marzo para alinearse con el año fiscal del gobierno. Para las empresas de Singapur, esta alineación significa que el año financiero de su filial india, el calendario fiscal del gobierno y los ciclos bancarios del RBI ahora operan bajo el mismo cronograma de abril a marzo, lo que reduce una capa de complejidad en la conciliación.

Un periodo contable de 12 meses se denomina comúnmente "año financiero" o "año fiscal". En la India, específicamente, este periodo va del 1 de abril al 31 de marzo y también se le llama "año anterior" en la terminología del impuesto sobre la renta.

El año fiscal (FY) 2025-26 abarca del 1 de abril de 2025 al 31 de marzo de 2026. El año de evaluación (AY) correspondiente es el 2026-27, que es cuando se evalúan y gravan los ingresos obtenidos durante el año fiscal 2025-26.

El año fiscal 2024-25 (a menudo denominado FY 25) comenzó el 1 de abril de 2024 y finalizó el 31 de marzo de 2025. El término "FY 25" puede causar confusión dependiendo de si se utiliza la convención del año de inicio o del año de finalización.

No. Singapur no exige un año financiero específico; las empresas constituidas en Singapur pueden elegir cualquier periodo de 12 meses como su año financiero. Muchas utilizan del 1 de enero al 31 de diciembre, lo que difiere del ciclo obligatorio de la India de abril a marzo, creando un desajuste en la presentación de informes para las empresas de Singapur con filiales en la India.

Según la Ley de Sociedades de 2013, las empresas registradas en la India —incluidas las filiales de empresas extranjeras— están obligadas a seguir el año financiero de abril a marzo. Existen excepciones limitadas para tipos de entidades específicos, como las empresas del IFSC, pero la flexibilidad es muy restringida.

Plazos clave a tener en cuenta:

El incumplimiento de estos plazos conlleva intereses del 1% mensual, además de sanciones acumulativas.

¿Necesita asesoramiento experto para gestionar los periodos contables y los requisitos de cumplimiento en la India? VJM Global se especializa en ayudar a empresas de Singapur a establecerse y operar en la India. Con más de 30 años de experiencia, ofrecemos servicios integrales de constitución de empresas, cumplimiento fiscal, gestión de informes con doble calendario y contabilidad continua adaptada a operaciones transfronterizas. Contáctenos en info@vjmglobal.com o al +91 98915 76441 para hablar sobre cómo podemos ayudar a que su empresa de Singapur tenga éxito en la India.