Foreign business owners setting up operations in Singapore often encounter an unfamiliar accounting landscape — different financial reporting standards, strict compliance deadlines, and regulatory bodies that operate far differently from systems in the US, UK, or Australia. A UK manufacturer expanding into Asia might struggle to reconcile IFRS-based parent company reports with Singapore's local framework, while a US tech startup faces dual reporting between US GAAP and Singapore standards.

Singapore's reputation as the 4th-ranked global financial centre (Global Financial Centres Index 37, March 2025) is built on a rigorous, internationally aligned accounting framework. The city-state follows Singapore Financial Reporting Standards (SFRS), closely modelled on IFRS, creating a familiar yet distinct system for the approximately 4,200 multinational regional headquarters operating here.

This guide covers the types of accounting standards applicable in Singapore, the core principles governing financial reporting, compliance obligations under ACRA (Accounting and Corporate Regulatory Authority), and critical differences between SFRS and IFRS that foreign companies must navigate.

TLDR:

Singapore Financial Reporting Standards (SFRS) are formulated by the Accounting Standards Council (ASC), an independent standard-setting body established under the Accounting Standards Act and operating under ACRA's purview. The ASC sets financial reporting standards for companies, charities, cooperative societies, and societies across Singapore.

Singapore's accounting framework has evolved through three distinct phases:

SFRS compliance is mandatory for:

Foreign businesses establishing a Singapore subsidiary cannot opt out. The subsidiary must prepare statutory financial statements under SFRS or SFRS(I), even if the parent company reports under US GAAP or another framework — making early compliance planning essential for any overseas entity entering Singapore.

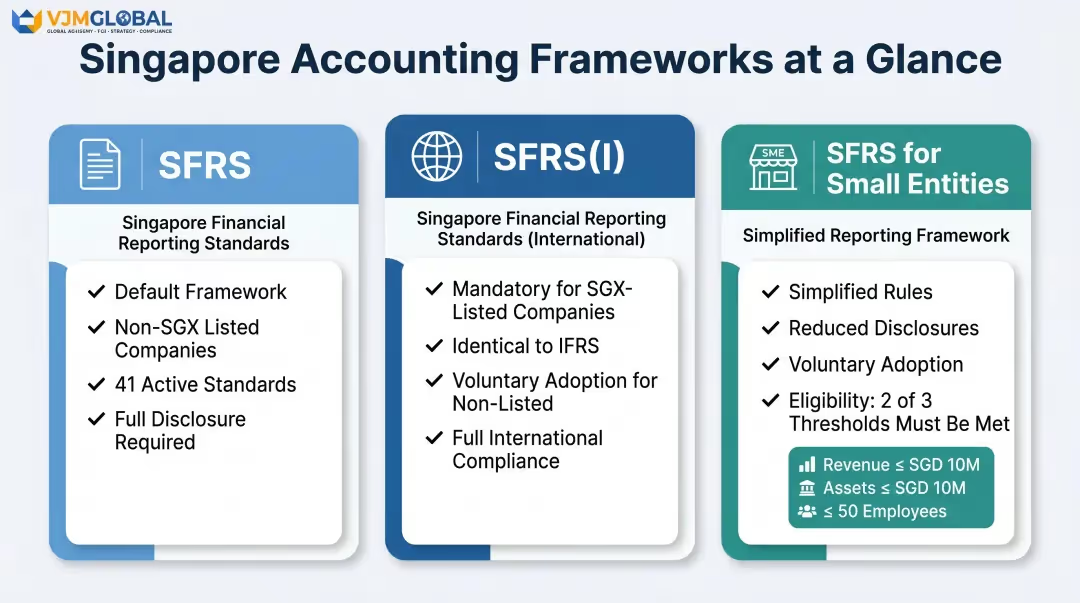

The ASC issues three primary frameworks, each designed for different entity types and business profiles. Selecting the right framework depends on company size, listing status, and whether the entity is publicly accountable.

SFRS is the default framework for most Singapore-incorporated companies that are not listed on SGX. The framework covers 41 distinct standards across topics from inventory valuation and lease accounting to revenue recognition and financial instruments.

StandardSubjectEffective DatePractical ImpactFRS 115Revenue from Contracts with Customers1 January 2018Governs when and how companies recognise revenue from customer contractsFRS 116Leases1 January 2019Requires lessees to recognise most leases on balance sheet, eliminating operating lease classificationFRS 109Financial Instruments1 January 2018Addresses classification, measurement, and impairment of financial assets and liabilities

These three standards carry the broadest business impact:

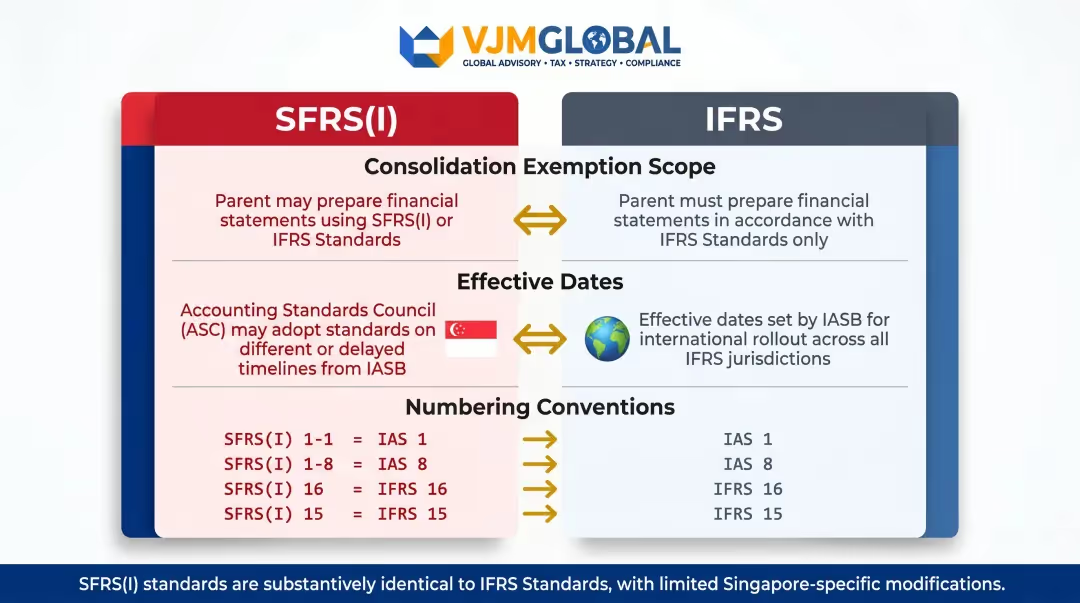

SFRS(I) is fully aligned with IFRS Standards, making it immediately familiar to multinational companies already operating under IFRS in other jurisdictions. The framework became mandatory for SGX-listed companies for annual periods beginning on or after 1 January 2018.

Non-listed companies may voluntarily adopt SFRS(I), which can be advantageous for:

This alignment with IASB pronouncements means SFRS(I) updates track closely with global IFRS changes — reducing restatement risk for multinationals moving between frameworks.

SFRS for Small Entities is a simplified framework for eligible small private companies, based on the IFRS for SMEs Accounting Standard — with reduced disclosure requirements and streamlined recognition rules.

Eligibility Criteria:

Companies must meet at least 2 of 3 thresholds for the immediate past two consecutive financial years:

Additional requirement: the entity must not be publicly accountable (no securities traded on public markets).

Adoption is voluntary. Eligible companies may choose full SFRS instead if they need more comprehensive reporting or face stakeholder expectations that require it.

SFRS is built on foundational principles drawn from the Conceptual Framework for Financial Reporting. These principles govern how transactions are recorded, disclosed, and interpreted — and they apply to every business preparing financial statements in Singapore.

Transactions must be recorded when they occur, not when cash changes hands. A company delivering services in December 2024 records revenue in 2024, even if the customer pays in January 2025.

This differs fundamentally from cash-basis accounting and provides a more accurate picture of financial position. For foreign business owners, the shift to accrual reporting is one of the first compliance adjustments to get right.

Financial statements assume the business will continue operating for the foreseeable future. Management must actively assess this assumption — especially during periods of financial stress, major restructuring, or market disruption.

If management has significant doubt about the company's ability to continue, two actions are required:

Companies must apply the same accounting policies from one period to the next, enabling meaningful comparison over time and across entities. Policy changes are permitted only when they produce more reliable and relevant information — and must be disclosed with a full explanation of the reason and financial impact.

Prudence requires exercising caution in judgement:

Completeness requires all material transactions to be properly recorded, classified, and disclosed.

The 2018 revised Conceptual Framework reinstated prudence as a component supporting neutrality — balancing conservatism with faithful representation.

Section 201(2) of the Singapore Companies Act 1967 requires financial statements to give a "true and fair view" of the company's financial position and performance. This overriding principle overrides strict technical compliance if literal adherence to a standard would produce misleading results.

Financial statements must be presented clearly and understandably to users with reasonable financial knowledge. Technical jargon without adequate explanation violates this principle.

Two agencies govern corporate compliance in Singapore: ACRA handles financial statement filing and corporate reporting, while IRAS (Inland Revenue Authority of Singapore) manages tax obligations. Both enforce mandatory deadlines — and penalties for missing them apply regardless of company size.

All Singapore-incorporated companies must prepare and file annual financial statements with ACRA comprising:

Accounting records must be retained for at least 5 years following the end of the financial year to which they relate, as required under Section 199(2) of the Companies Act.

AGM requirements vary by company type:

Company TypeAGM DeadlineListed companiesWithin 4 months after financial year-endNon-listed companiesWithin 6 months after financial year-end

Private companies may skip holding an AGM if they send financial statements to all entitled persons within 5 months after financial year-end, unless a member or auditor requests an AGM.

Annual return filing deadlines are measured from financial year-end, not from AGM date:

Most companies must undergo statutory annual audit conducted by a registered auditor. Small companies meeting at least 2 of 3 criteria may be exempt from audit:

These are the same thresholds as SFRS for Small Entities eligibility. Dormant companies are also exempt from audit requirements.

Corporate income tax returns must be filed annually with IRAS. Key tax obligations include:

The Year of Assessment (YA) is based on income earned during the prior calendar year. Income earned in financial year 2024 is assessed in YA 2025.

Navigating both ACRA and IRAS obligations simultaneously — each with its own deadlines and filing formats — is where many foreign companies run into trouble. VJM Global's cross-border accounting team works with multinational companies and foreign investors across 15+ industries, supporting compliance reporting, annual return preparation, and financial statement services aligned with IFRS and international accounting standards.

Singapore companies must produce a complete set of financial statements for each reporting period. The five required components provide a comprehensive view of financial health:

Most companies must submit financial statements in XBRL (eXtensible Business Reporting Language) format via ACRA's BizFinx system:

Company TypeXBRL RequirementSolvent Exempt Private Companies (EPCs)Exempt from filing financial statements (declaration of solvency only)Insolvent EPCsMust file in XBRL (Full or Simplified)Non-exempt private companiesMust file in XBRL (Full or Simplified)Public companiesMust file in Full XBRLForeign company branchesFile in PDF format

An EPC is defined as a private company with no more than 20 shareholders and no corporate shareholders.

Beyond these filing mechanics, one principle governs all financial reporting in Singapore regardless of company type. Financial statements must provide a "true and fair view" of the company's financial health — an overriding principle that supersedes strict technical compliance if literal adherence to a standard would produce misleading results.

SFRS is substantially based on IFRS, meaning companies familiar with IFRS will find Singapore's standards largely recognisable. The Institute of Singapore Chartered Accountants confirms that "SFRS are substantially word for word IFRS."

Key Alignment Points:

Listing TypeAccepted StandardsReconciliation Required?Domestic primary listing (SG-incorporated)SFRS(I) mandatoryNoForeign primary listingSFRS, IFRS, or US GAAPNo (if using one of these three)Foreign secondary listingHome country standardsYes — reconcile to SFRS, IFRS, or US GAAP

For US and UK businesses with secondary Singapore listings, this reconciliation obligation is the most common compliance gap — the table above maps exactly where each scenario falls.

Singapore does not follow US GAAP domestically. US-based parent companies with Singapore subsidiaries face dual reporting requirements:

Most multinational groups manage this through conversion adjustments or maintain dual-basis accounting from the start. For groups with India operations in the mix, this multi-framework juggle — SFRS, US GAAP, and Ind AS — is where specialist cross-border accounting support pays for itself.

While SFRS(I) mirrors IFRS closely, specific differences exist:

Before 2018, SFRS carried more significant departures from IFRS — including deferred standard adoption and Singapore-specific modifications. The SFRS(I) convergence project eliminated most of these for listed companies, which is why the two frameworks are now so closely aligned in practice.

Singapore's SFRS framework operates on core principles including accrual basis accounting, going concern assumption, consistency and comparability, prudence, completeness, fair presentation, and understandability. These principles are embedded in the Conceptual Framework for Financial Reporting and govern how all Singapore companies prepare financial statements.

SFRS is closely aligned with but not identical to IFRS. Standard SFRS is "substantially word for word IFRS" with minor local adaptations. SFRS(I), mandatory for SGX-listed companies since 2018, is identical to IFRS Accounting Standards, making it fully equivalent for practical purposes.

The Accounting Standards Council (ASC) formulates and issues standards under the Accounting Standards Act. ACRA enforces compliance through the Financial Reporting Surveillance Programme and oversees company registration, financial statement filing, and public accountant regulation.

SFRS for Small Entities is a simplified, optional framework with reduced disclosure requirements for private companies meeting 2 of 3 thresholds: revenue ≤ S$10 million, assets ≤ S$10 million, or ≤ 50 employees — and not being publicly accountable. Larger or publicly accountable entities must apply full SFRS.

Yes. Singapore branches of foreign firms must comply with SFRS when preparing their statutory financial statements. Foreign companies with equity securities listed on SGX may use SFRS, IFRS Standards, or US GAAP depending on their listing type (primary vs secondary).

Companies must retain accounting records for at least 5 years after the end of the financial year to which they relate, as required under Section 199(2) of the Companies Act. IRAS imposes the same 5-year retention requirement for tax-related documents.

Singapore's three-tier compliance architecture — full SFRS with audit and XBRL filing, SFRS for Small Entities with audit exemption, or minimal filing for solvent EPCs — gives foreign companies meaningful flexibility. Choosing the right framework early reduces administrative burden and avoids compliance gaps as your Singapore operations grow.