%20(3).jpg)

Foreign business owners establishing operations in Singapore often assume that annual statutory audits are mandatory for all incorporated entities—only to discover during their first financial year that exemptions exist. The real work lies in determining whether your specific company structure, revenue profile, and group affiliations qualify under Singapore's precisely defined criteria.

Singapore's Companies Act 1967 governs all audit obligations, with the Accounting and Corporate Regulatory Authority (ACRA) as the enforcer. According to ACRA's registry data, approximately 628,000 business entities were registered as of early 2026, and a substantial share are foreign-owned private limited companies.

Many of these entities qualify for audit relief under the "small company" framework introduced in 2015. But qualifying requires careful attention to two-year performance windows, group-level consolidation rules, and dormancy criteria.

Whether you're a newly incorporated private company, part of a multinational group structure, or a foreign investor with a Singapore subsidiary, this guide clarifies your audit position, exemption eligibility, and ongoing compliance obligations even when audits aren't required.

TLDR:

A statutory audit under the Companies Act is an annual independent examination of a company's financial statements by a public accountant registered with ACRA. The auditor's mandate is to confirm that the statements comply with Singapore Financial Reporting Standards (SFRS) and present a "true and fair view" of the company's financial position and performance, as required by Section 207.

All private limited companies in Singapore are subject to statutory audit requirements by default. Section 205(1) requires directors to appoint at least one auditor within 3 months of incorporation. Failure to do so carries fines of up to S$5,000.

Companies can avoid the audit requirement only if they qualify under one of three specific categories:

For foreign-owned entities, an audit provides independent assurance to stakeholders — investors, lenders, and regulators — particularly when the parent company is overseas and direct oversight of Singapore operations is limited. Banks often require audited statements for credit facilities, and certain government grants or contracts mandate audited financials regardless of exemption status.

Statutory timeline: Directors must appoint at least one auditor within 3 months of incorporation. Only public accountants or accounting firms registered with ACRA under the Accountants Act may serve as company auditors. Auditors who practise without ACRA registration face fines up to S$10,000 and/or imprisonment.

Tenure structure: Auditors hold office from appointment until the conclusion of the company's next Annual General Meeting (AGM), at which point they must be reappointed or replaced. If directors fail to appoint, any shareholder may apply to ACRA to make the appointment on the company's behalf.

Removal vs. resignation:

Auditors assess whether a company's core financial statements comply with SFRS and give a true and fair view. Their scope and access rights are defined by statute:

Singapore law does not prescribe specific audit fees — these are negotiated between the company and the auditing firm. Shareholders retain disclosure rights, however. Under Section 206(1), shareholders can compel fee disclosure if they meet either threshold:

This applies to both auditor remuneration and any non-audit service fees paid to the same firm.

Singapore operates a "small company concept" under Section 205C, which allows qualifying private companies to be fully exempt from statutory audit requirements. This exemption applies to financial years beginning on or after 1 July 2015.

There are three distinct exemption pathways — small company, small group, and dormant company — each with its own qualifying criteria. A company may fall under one or more of these tracks depending on its structure.

To qualify, a company must satisfy both of the following conditions:

CriterionThresholdTotal annual revenue≤ S$10 millionTotal assets (at FY-end)≤ S$10 millionFull-time employees (at FY-end)≤ 50

Companies incorporated for less than two years qualify by meeting the criteria in the current year only. From the second year onward, both prior years are assessed.

Source: ACRA Audit Exemptions

Singapore-resident companies that belong to a corporate group face an additional layer of assessment. Both of the following conditions must be met:

A few details that frequently catch companies off guard:

Common pitfall: A US parent with S$50 million in global revenue will fail the group test, forcing the Singapore subsidiary into a mandatory audit — even if that subsidiary has only S$500,000 in local revenue.

A third pathway applies to companies that have simply stopped trading. Under Section 205B(2), a company is dormant during any period in which no accounting transactions occur — regardless of size or group membership.

The following activities do not break dormant status (Section 205B(3)):

Two override provisions limit this exemption. First, Section 205D allows the Registrar to require audited statements if the company has breached Section 199 (accounting records) or Section 201 (financial statements), or if the public interest demands it. Second, members holding at least 5% of issued shares may require an audit for any given year by written notice.

Audit exemption removes the statutory audit requirement — it does not remove compliance obligations. Exempt companies must still prepare unaudited financial statements (UFS) that include:

UFS serve several practical and regulatory purposes:

On the annual filing side:

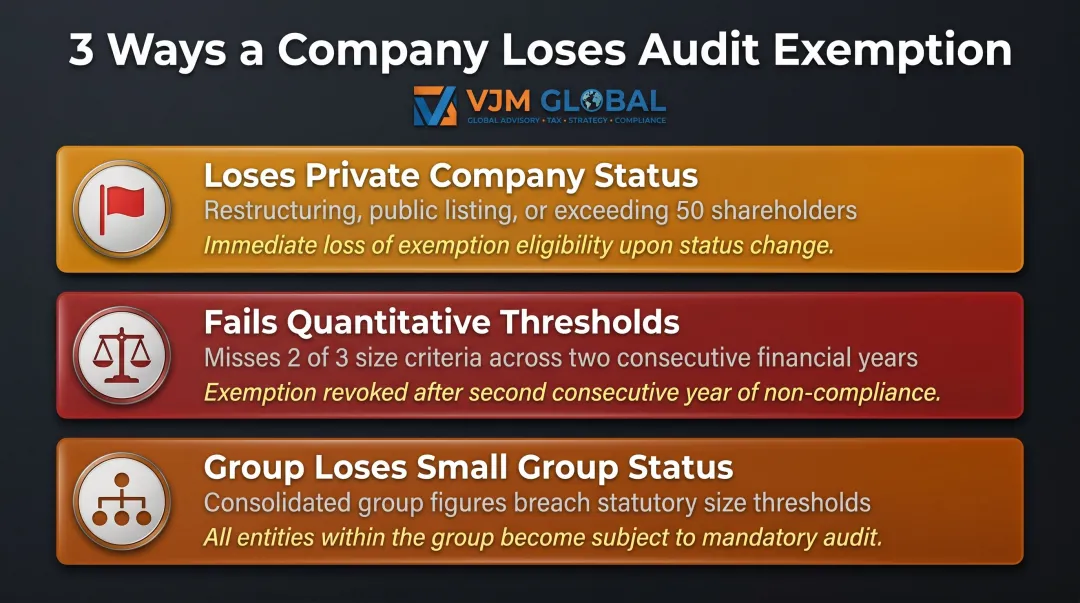

Three scenarios can strip a company of its audit exemption:

Companies approaching the S$10 million revenue or asset thresholds should monitor both metrics closely across consecutive years. Because the exemption is assessed on a two-year rolling basis, strong growth in year 2 can quietly trigger mandatory audit requirements for year 3 — leaving little time to appoint a qualified auditor.

OffencePenaltyLate annual return filing (up to 3 months)S$300 late feeLate annual return filing (beyond 3 months)S$600 late feeCourt conviction for filing offencesUp to S$5,000 per chargeFailure to appoint auditorUp to S$5,000 for company and every director in defaultFailure to maintain accounting recordsUp to S$10,000 or 12 months imprisonment, plus default penaltyFalse or misleading statementsUp to S$50,000 or 2 years imprisonment, or both

Source: ACRA Penalties & Enforcement

If composition sums are not paid or defaults are repeated, ACRA may prosecute the company and its directors. Court summons are sent via registered mail — if a director fails to attend, a warrant for their arrest will be issued. Directors convicted of 3 or more filing offences within 5 years are disqualified from acting as directors for 5 years.

OffencePenaltyLate filing of corporate income tax returnUp to S$5,000 per offenceNon-filing for 2+ consecutive yearsPenalty of twice the tax assessed PLUS fine up to S$5,000 per offenceDirector failure to comply with Section 65B(3) noticeUp to S$10,000 or 12 months imprisonment, or both

Source: IRAS Late Filing or Non-Filing

Beyond company-level fines, directors face personal exposure. Wilful or serious non-compliance can result in personal fines, imprisonment, and permanent disqualification from holding directorial positions.

The "2-year rule" requires a company to meet at least 2 of 3 quantitative criteria (revenue ≤S$10M, assets ≤S$10M, employees ≤50) for the immediate past two consecutive financial years to qualify as a small company. Newly incorporated companies need only meet the criteria for their first year.

Section 157 covers directors' duties — specifically the obligation to act honestly and exercise reasonable diligence. Breaches can result in fines up to S$20,000 or 12 months imprisonment, and apply regardless of whether a company holds audit-exempt status.

No. Private companies that qualify as small companies, small groups, or dormant companies are exempt from statutory audit. They must still prepare unaudited financial statements and file annual returns with ACRA.

Yes. Unlike the older Exempt Private Company framework, the current small company exemption does not require all shareholders to be individuals. Corporate shareholders—including foreign parent companies—do not disqualify a company from the exemption, provided the quantitative criteria are met.

Once a company no longer qualifies as a small company or small group, it must comply with full statutory audit requirements—including appointing an ACRA-registered auditor and having financial statements audited—from the financial year in which disqualification occurs.

Yes. Audit-exempt companies must still prepare unaudited financial statements and file annual returns with ACRA within 7 months of financial year-end. Most companies are also required to submit financial statements in a structured digital format, unless they qualify for simplified filing as a small dormant company.